QE and the Tokyo stock market (part two, banks and others)

June 12, 2014 Leave a comment

QE and the Tokyo stock market (part two, banks and others)

Andrew Smithers | Jun 03 08:30 | 1 comment | Share

In my last blog I emphasised the importance of foreign investors for the Tokyo stock market, but suggested that their future behaviour was either unpredictable or momentum based. If the latter assumption is correct, foreigners are likely to amplify rather than lead changes in the market’s direction and to assess its prospects we therefore need to look at the other participants.

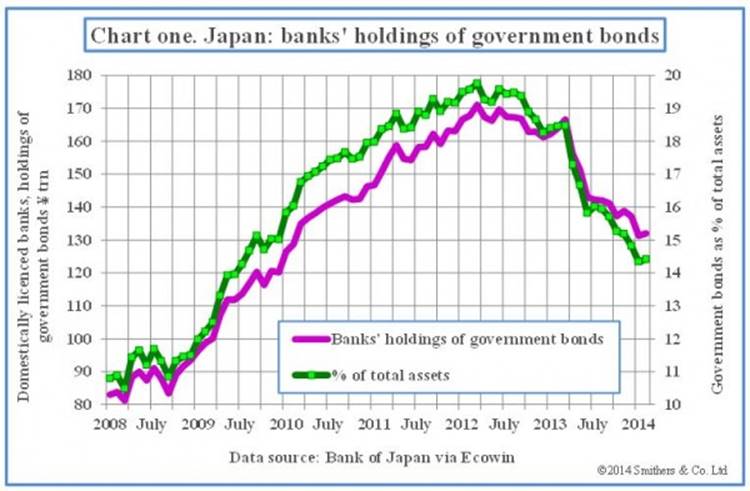

Chart one (below) shows that Japanese banks have been rapidly reducing their holdings of government bonds. These have fallen from 20 per cent of total assets to 14 per cent. This has had a beneficial impact in that the risk that banks will suffer large losses when interest rates rise has been much reduced.

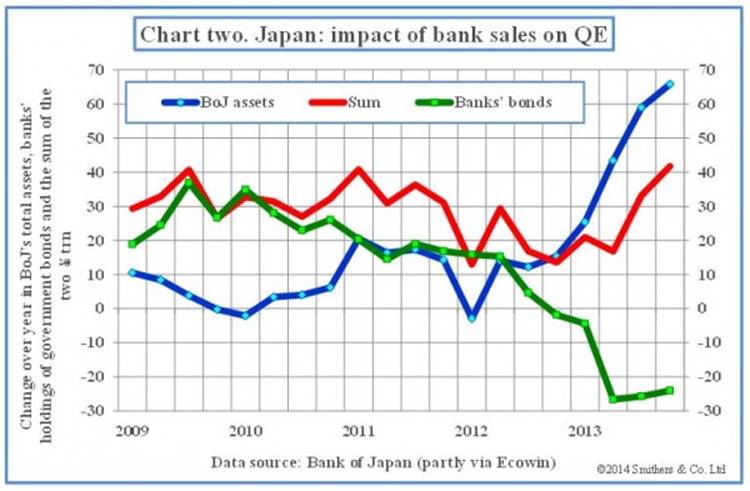

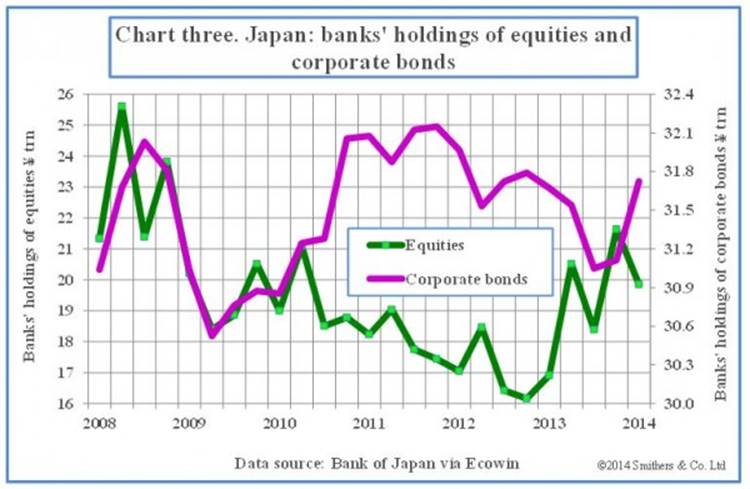

Bank selling of bonds has, however, probably had a negative impact on share prices, because it has had the effect of reducing the impact of quantitative easing on the liquidity of other investors. Chart two (below) shows the extent to which sales of government bonds by banks have effectively stultified the impact of QE. As banks have not been increasing their holdings of either equities or corporate bonds (see chart three), which are also much smaller than their holdings of government bonds, there has been a sharp rise in their liquidity preference.

US banks, however, have tended to increase rather than reduce their holdings of government debt (chart four) and thus reinforced rather than moderated, as in the case of Japan, the impact of QE on the liquidity of other investors.

Individuals and institutions appear to have had a lagged response to the stock market, as I show in chart five. (It is quite hard to differentiate between the two sectors as institutions include purchases made by individuals through investment trusts and certain types of life insurance contracts.)

The Japanese government seems anxious to boost the stock market. It has sought to encourage individuals with tax incentives to buy shares via institutions through new individual savings accounts. Though this appears to have had little impact so far, a rising market could well stimulate a better response. Additional support for shares is also likely to come from a switch by the state pension fund from bonds to equities.

Even at current levels of bank purchases of bonds, QE is having a marked impact on the liquidity of other domestic investors as chart two shows. As companies appear to have no wish to raise funds either by bond or equity issues, the choices for domestic investors are either to allow their liquidity to rise or to try to buy domestic equities or foreign assets. It seems likely that either choice will benefit Japanese share prices, either directly or indirectly, as increased spending on foreign assets is likely to put downward pressure on the yen.

Chart six shows that, in the recent past, the stock market and the yen have moved closely together.

As a weak yen tends to push up the profits of manufacturing companies, which are heavily represented in the stock market, it is not only the past relationship but also an improved outlook for profits which provide a rationalisation for a weak exchange rate being reflected in a stronger stock market.

Foreigners may of course keep selling, though they appear to have halted in April, and the liquidity preference of individuals and institutions may rise. But it looks to me as if, at least in terms of liquidity, the outlook for the Tokyo market is improving.