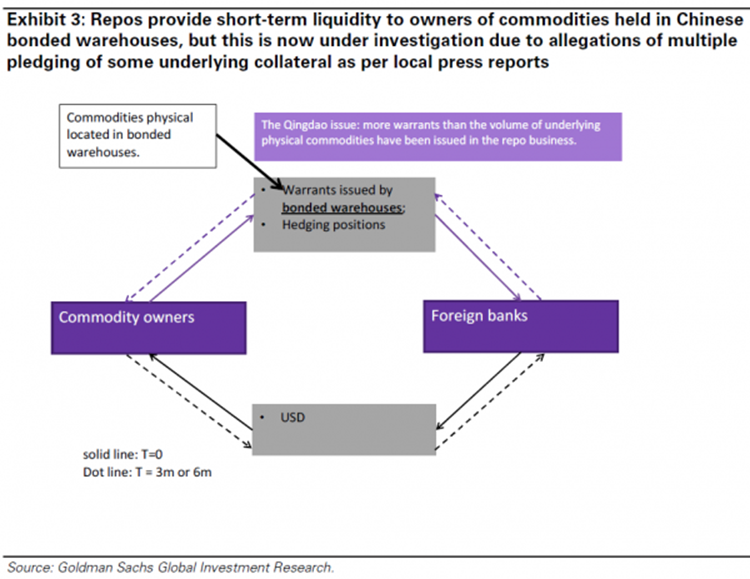

China’s Rehypothecation Scandal In One Chart

June 13, 2014 Leave a comment

China’s Rehypothecation Scandal In One Chart

Tyler Durden on 06/10/2014 13:51 -0400

Remember how small Greece was and how it wasn’t relevant to US stocks… until suddenly it got close to breaking up the EU and the world’s markets slumped. Remember how small subprime was? Remember how Lehman was not a ‘big’ bank? We hear the same “why would that impact us?” chatter now about the China rehypothecation scandal and we suspect the outcome will be just as dramatic a “whocouldanode” moment for many. The problem, as this chart so simply explains, is “more warrants than the volume of the underlying physical commodities have been issued in the repo business” and that is a problem for every foreign bank that was tempted into China’s carry trade (which is “every” bank).

Simply put – the collateral that I promised you on my loan… I also promised to between 10 and 30 other people… but we’re good right?

The “repo” business in commodities in China is similar to any other “repo” business in the financial markets. Generally speaking, the repo is a short-term FX funding vehicle, whereby a commodity owner first sells the commodity warrants issued by bonded warehouses (paired with an equal amount of short positions) to banks, then buys the package back from the banks in 3 to 6 months. It is a way for commodity traders/refiners to gain access to foreign banks’ balance sheets and improve liquidity efficiently.

The Qingdao situation alleges the issuance and pledging of more warrants than the underlying physical commodity. Were this to have occurred, foreign banks may be exposed to asset write-offs due to potential collateral shortages and/or losses. As a result, some foreign banks may have reduced or suspended their commodities repo business in China, and could be undertaking further investigation as to whether to make any suspension permanent.

…

The initial reaction is likely to be to significantly reduce the exposure to different repo businesses and investigate whether there are any other multi-pledge issues in other deals. This is already happening in the market.

A further potential reaction, in our view, is for the banks to investigate the broader spectrum of their Chinese commodity financing deals (i.e. not just the repos or CCFDs, but the whole book) in order to clarify:

whether these deals are exposed to substantial underpriced risks;

whether the banks as a whole still want to continue the business;

if they choose to continue, what rules could be established and enforced.

Our base case is that, even if banks do not find any further cases during the investigation periods, they are likely to raise the bar for Chinese commodity financing deals in general, in order to broadly lower the exposure to this sector. This would occur via higher funding costs for the arbitrageurs, thereby slowly disincentivising repurchase deals and CCFDs, and resulting FX inflows.

* * *

In a world where central banks have encouraged levered carry trades everywhere, a crack in the virtuous circle – such as we are seeing in China’s fractional-reserve commodity financing deal business – will rapidly lead to a sell first (unwind first), think later mentality.