The Cost Accounting Whale Curve to Understand Accounting Fraud in Asia

September 10, 2014 Leave a comment

“Bamboo Innovators bend, not break, even in the most terrifying storm that would snap the mighty resisting oak tree. It survives, therefore it conquers.” |

| BAMBOO LETTER UPDATE | September 8, 2014 |

Bamboo Innovator Insight (Issue 49)

|

|

The Cost Accounting Whale Curve to Understand Accounting Fraud in Asia

“It struck me as a business I didn’t know anything about initially. You know, you’re talking about petroleum additives… Are there competitive moats, is there ease of entry, all that sort of thing. I did not have any understanding of that at all initially. And I talked to Charlie a few days later…and Charlie says, ‘I don’t understand it either.’ I decided there’s probably a good size moat on this. They’ve got lots and lots of patents, but more than thatthey have a connection with customers… Lubrizol is exactly the sort of company with which we love to partner—the global leader in several market applications run by a talented CEO, James Hambrick.” – Warren Buffett on Lubrizol, the $9.7 billion oil additives, lubricants and specialty chemicals company that Berkshire Hathaway bought into in March 2011

“It’s hard to imagine that three years after the fall of Sino-Forest, a fraud twice its size could navigate through a sea of regulators, investment bankers, and auditors to list on a global stock exchange.” – Anonymous Analytics on Tianhe Chemicals, the “Lubrizol of China” in their 67-page report

Information may be used to inform or deceive. Accounting is at the heart of the information system in economies and companies, providing information to lubricate the market and internal working parts of an organization, thus contributing to their smooth functioning.

When accounting frauds and financial failures pop up as what appear to be rather sudden surprise while the most recent financial statements indicate a sound condition, accounting loses their legitimacy and effectiveness. Where were the accountants and auditors?

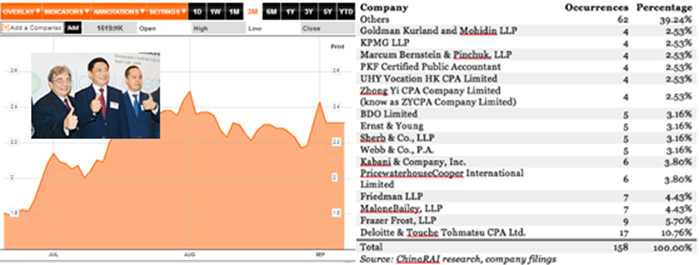

We were left asking this question last week when HK-listed Tianhe Chemicals (1619 HK, MV $7.6bn) was suspended on Tuesday after Anonymous Analytics (AA) issued a report detailing how the chemicals company, who raised $650 million in its June IPO deal brought to the market by sponsors Morgan Stanley, Bank of America Merrill Lynch and UBS, massively inflate its revenue and profits and “is one of the largest stock market frauds ever conceived.”

The role of two independent experts have come into the spotlight: the auditor verifying the accounting numbers, and the market research firm Frost & Sullivan producing industry and market share data which was heavily relied upon by analysts and investors. Tianhe is audited by Hong Kong’s Deloitte. According to data compiled by ChinaRAI in May 2013, Deloitte has more “occurrences” of fraud and other accounting issues in China than the other Big 4 firms combined (table above). AA said that original filings made by Tianhe’s main Chinese operating subsidiaries to the SAIC (State Administration for Industry and Commerce) showed revenue and profit that were 85 to nearly 100% less than what the company declared in its filings to investors in its HK IPO.

In another alleged accounting fraud, Emerson Analytics detailed how the sausage-casing maker Shenguan (829 HK, MV $1.1bn) inflated revenue (selling price to its largest customer was over 40% higher than what it charged others on average in the same standardized product) and concealed high cost of raw materials (cattle skin). Ernst & Young’s audit coverage excluded the BVI and PRC subsidiaries were audited by local firm Shenzhen Pengcheng, which had its securities business permit revoked by the CSRC in May 2013 for its failure to perform due diligence in the IPO of Yunnan Green-Land Biological Technology (002200 CH).

Tianhe claims to be a top five player in the world in terms of lubricant additive sales, behind Lubrizol of the US, the number-one manufacturer, and also number two behind DuPont of the US in speciality fluorochemicals (SFC).Tianhe’s lubricant additive make up 40% of sales with margins at 27% while its SFC clocks in a breath-taking 85% margin. Tianhe, with a market value of $7.6bn, is relatively large as compared to Buffett’s Lubrizol at $9.7bn. So what is the difference in the business model between Lubrizol and Tianhe?

Both Buffett and Munger initially did not understand about the competitive dynamics of this seemingly-commoditized business and wonder whether it has an economic moat and pricing power. After all, around two-thirds of Lubrizol’s sales come from oil lubricants and additives, which are oil-based and the company must purchase some heavy hydrocarbons such as crude to make them. That means that Lubrizol is exposed to fluctuations in the volatile oil market. When the price of base oil is high and keeps rising, a key question is whether Lubrizol can effectively passed that higher price on to consumers in a cost-plus pricing model based on volume.

Buffett gave us the all-important clue to assessing the moat of true compounders and Bamboo Innovators such as Lubrizol or Huchems Fine Chemical (069260 KS, MV $943m), Korea’s sole supplier of polyurethane (PU) intermediate materials: “They have a connection with customers”. A close customer relationship minimizes earnings volatility inherent in the petrochemical business.

Huchems Fine Chemical (069260 KS) – Stock Price Performance, 2002-2014

For instance, one of the secrets for Huchems…

<Article snipped>

As the late management accounting pioneer Dr Charles Horngren puts it aptly, “You need to understand the business first, before you can understand the accounting of the business.”

An observation is that too often students today walk away from an accounting course in which they learned models, standards and techniques, were tested on computations, and now know a laundry list of standards, but have no clue about the accounting way of thinking and what accounting as a subject is all about.

Accounting is not just about reporting numbers but is also about structuring incentives, generating information that guides decisions, providing disciplinary feedback on decisions, and inspiring innovations. The accounting way of thinking gives us a language to analyze in a systematic manner and help us reach informed opinions. The accounting way of thinking requires logic and interpretation, an ability to grasp problems and offer solutions, and an ability to ponder deeper questions and offer tentative answers in an ongoing conversation and learning by inquiry.

When accounting frauds occur, accounting loses their legitimacy and effectiveness: Where were the accountants and auditors? As accounting educators, we cannot seek to answer this unless we have managed to think deeper about these two important questions:

It would not be very often that we encounter someone who says, “Oh, how exciting, it really impacted my life and the way I think about the world.” We need to teach and research accounting as an intellectually exciting and world-illuminating discipline. Accounting doyen Ray Ball had bemoaned: “The absence of a solidly grounded worldview – a deep understanding of the function of financial reporting in the economy – is a major threat to accounting.”

Some of the most exciting developments for the next generation lie at the periphery of accounting even though information is often said to lie at the heart of accounting. We need to find ways to make investors feel the importance of bias in accounting and financial information through the interdisciplinary lenses: the ways that conflicts of interest affect the financial reporting process, the institutional mechanisms that limit or exacerbate this behavior, the power held by the preparers and reporters of information in the context of the countries and companies that do not permit a transparent flow of information. This is particularly true in Asia which is not a monolithic homogenous bloc and can be a heterogeneous mess for users of accounting information without a resilient mental model.

By expanding the accounting way of thinking to the cost accounting of whale curve to understand more about customer profitability and the business model in serving customers, value investors can better understand tunneling and expropriation acts by companies via related party transactions to generate artificial sales.

Warm regards, KB Managing Editor The Moat Report Asia SMU: http://accountancy.smu.edu.sg/faculty/profile/108141/Kee%20Koon%20Boon

To read the exclusive article in full to find out more about the story of Korea’s bamboo innovator Huchems and the cost accounting whale curve to understand accounting fraud in Asia, please visit:

|

| The Moat Report Asia |

|

“In business, I look for economic castles protected by unbreachable ‘moats’.” – Warren Buffett

The Moat Report Asia is a research service focused exclusively on competitively advantaged, attractively priced public companies in Asia. Together with our European partners BeyondProxy and The Manual of Ideas, the idea-oriented acclaimed monthly research publication for institutional and private investors, we scour Asia to produce The Moat Report Asia, a monthly in-depth presentation report highlighting an undervalued wide-moat business in Asia with an innovative and resilient business model to compound value in uncertain times. Our Members from North America, the Nordic, Europe, the Oceania and Asia include professional value investors with over $20 billion in asset under management in equities, secretive global hedge fund giants, and savvy private individual investors who are lifelong learners in the art of value investing.

Learn more about membership benefits here: http://www.moatreport.com/subscription/

https://www.moatreport.com/individual-subscription/?s2-ssl=yes

Our latest monthly issue for the month of August investigates an Asian-listed company who’s the leading ecommerce group in its home country with the complete platform coverage in the Amazon-type of B2C ecommerce of selling directly to end consumers (Sales/Net Profit: 90%/78%), Rakuten-type of B2B2C platform (Sales/Net Profit: 4%/12%) to support the online SME merchants who in turn sell to the end consumers, and the eBay-type of C2C auction site (Sales/Net Profit: 2%/21%) where individuals buy and sell to one another. This “Amazon-Alibaba” is highly profitable with recurring free cashflow (FCF yield 4.6-5% compounding at 25% in the next 3-5 years) bypioneering the world’s-first 24-hour delivery promise and guarantee when world-class logistics experts said it cannot be done. In emerging markets and Asia where logistics costs is 15-20% of GDP, most ecommerce companies fail to scale up due to lack of fulfillment capabilities and inventory risk became the killing blow as they pursue growth without the intangible know-how. The company designs and builds its own warehouses to provide fast and efficient delivery with 99.68% on-time rate and also complete backend services to suppliers, widening the gap between itself and peers. With its superior infrastructure, the company is able to provide consumers a one-stop shopping experience with all goods purchased from different vendors packaged into a single box and delivered to the client’s door. The company has consignment agreements with suppliers which allow it to have control over inventory management but carry no liability of inventory on its balance sheet, in other words, there is minimal inventory riskfor the company to scale up sustainably and without the usual accounting risks that plagued the ecommerce companies.

With (1) a superior ROE of 23.6% due to its wide-moat business model in 24-hour delivery system, (2) negative cash conversion cycle (-29 days) in its unique warehouse system with minimal inventory risk, (3) a sustained 25-30% recurring earnings and cashflow growth per annum in the next 5 years, especially a long run-way in disrupting traditional retailers, and (4) potential exponential growth in its option value in the third-party electronic payment business, the company can scale up multiple times. Short-term downside risk is protected by its healthy$128m net-cash balance sheet (15% of MV) and proven management execution in prudent capex expansion to support sustainable quality earnings growth. Its terminal value and long-term downside risk will be protected by giants Alibaba, Rakuten, eBay, Amazon who wish to swallow it up to possess its valuable trust and brand equity support it enjoys and its wide-moat business model in 24-hour delivery system. The company is one of the few Asian ecommerce companies with good governance and low accounting risks with its net-value revenue recognition method and it deserves a valuation premium. Upcoming deregulation in third-party electronic payment with the passing of the law in Sep 2014 will result in various government restrictions to be removed, paving the way for the company to introduce stored-value payments, O2O payment, P2P payment (money transfer without transactions), multiple currencies’ payments, big data analysis, payment services for customers outside the group to boost transaction volume and scale up its existing proprietary PayPal/AliPay business. Led by the inspiring and highly-determined founder and Chairman who established and listed the company in 1998 and 2003 respectively, the company has overcome the multiple obstacles to ecommerce transactions in its home market. The founder described the obstacles to ecommerce transactions as ‘friction’, and that he “resolve to take on the Life’s Task to reduce this ‘friction’”.

Our past monthly issues examine:

The Moat Report Asia Members’ Forum has been getting penetrating quality dialogues from our subscribers.Questions range from:

Do find out more in how you can benefit from authentic and candid on-the-ground insights that sell-side analysts and brokers, with their inherent conflict-of-interests, inevitable focus on conventional stock coverage and different clientele priorities, are unwilling or unable to share. Think of this as pressing the Bloomberg “Help Help” button to navigate the Asian capital jungle. Institutional subscribers also get access to the Bamboo Innovator Index of 200+ companies and Watchlist of 500+ companies in Asia and the Database has eliminated companies with a higher probability of accounting frauds and misgovernance as well as the alluring value traps.

|

| Professional Development Workshops for Executives and Lifelong Learners |

|

Our 8th run of the series of workshop From the Fund Management Jungles: Value Investing Exposed and Explored – (Part 1) Moat Analysis, (Part 2) Tipping Point Analysis and (Part 3) Detecting Accounting Fraud – on 14 June 2014 has been well-received with serious value investors, professionals, and serious lifelong learners attending, with some who flew in from Jakarta and KL!..

Our 9th workshop will be on Detecting Accounting Fraud Ahead of the Curve sometime later in the year.

Thank you for your support all this while!

|

|

Thank you so much for reading as always.

Warm regards, KB Kee Managing Editor The Moat Report Asia Singapore Mobile: +65 9695 1860

A Service of BeyondProxy LLC 1608 S. Ashland Avenue #27878 Chicago, Illinois 60608-2013 Other offices: London, Singapore, Zurich

|

|

P.S.1 Here is a little more about my background: KB Kee has been rooted in the principles of value investing for over a decade as an analyst in Asian capital markets. He was head of research and fund manager at a Singapore-based value investment firm. As a member of theinvestment committee, he helped the firm’s Asia-focused equity funds significantly outperform the benchmark index. He was previously the portfolio manager for Asia-Pacific equities at Korea’s largest mutual fund company.

He holds a Masters in Finance and degrees in Accountancy and Business Management, summa cum laude, from Singapore Management University (SMU) and had also published articles on governance and investing in the media, as well as published an empirical research paper Why ‘Democracy’ and ‘Drifter’ Firms Can Have Abnormal Returns: The Joint Importance of Corporate Governance and Abnormal Accruals in Separating Winners from Losers in the Special Issue of Istanbul Stock Exchange 25th Year Anniversary Best Paper Competition, Boğaziçi Journal, Review of Social, Economic and Administrative Studies, Vol. 25(1): 3-55. KB has also presented his thought leadership as a keynote speaker in global investing conferences. KB has trained CEOs, entrepreneurs, CFOs, management executives in business strategy, value investing, macroeconomic, industry trends, and detecting accounting frauds in Singapore, HK and China, and had taught accounting at the SMU where he is currently an adjunct lecturer.

P.S.2 Why do I care so much about doing The Moat Report Asia for you? My personal motivation in embarking on this lifelong journey has been driven by disappointment from observing up close and personal the hard-earned assets of many investors, including friends and their families, burnt badly by the popular mantra: “Ride the Asian Growth Story!” I witnessed firsthand the emotional upheavals that they go through when they invest their hard-earned money – and their family’s – in these “Ride The Asian Growth Story” stocks either by themselves or through money managers, and these stocks turned out to be the subject of some exciting “theme” but which are inherently sick and prey to economic vicissitudes. They may seem to grow faster initially but the sustainable harvest of their returns is far too uncertain to be the focus of a wise program in investment. Worse still, the companies turned out to be involved in accounting frauds. Their financial numbers were “propped up” artificially to lure in funds from investors and the studiously-assessed asset value has already been “tunnelled out” or expropriated. And western-based fraud detection tools and techniques have not been adapted to the Asian context to avoid these traps.

After a decade-plus journey in the Asian capital jungles, it has been somewhat disheartening as I observe many fraud perpetrators go away scot-free and live a life of super luxury on minority investors’ hard-earned money. And these perpetrators make tempting offers to various parties in the financial community to go along with their schemes. When investors have knowledge in their hands, we have a choice to stay away from these people and away from temptations and do the things that we think are right. With knowledge, we have a choice to invest in the hardworking Asian entrepreneurs and capital allocators who are serious in building a wide-moat business.

|

CONNECT WITH US      |

| MOAT REPORT ASIA OUR TEAM SUBSCRIBE MEMBERS CONTACT US

The Moat Report Asia Other offices: London, Singapore, Zurich |