| Dear Friends,Detecting Accounting Fraud in Asia (Part 4): Introducing Six New MeasuresEarlier articles in the Accounting Fraud in Asia series:

“What seemed to be wrong with this income statement?” I would ask and engage value investors in a conversation discussing the limitations of western-based screening tools and techniques in financial statement analysis to analyze Asian companies.

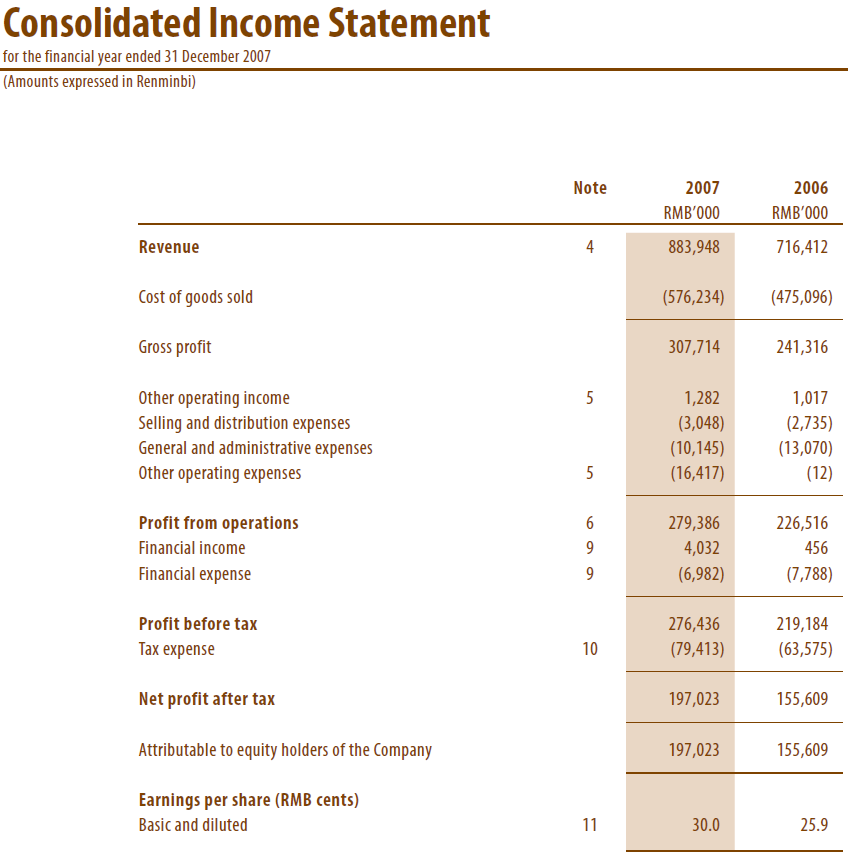

“It was generated by a listed Chinese zipper company who claimed to be the ‘YKK of China’ with a diversified customer base of over 900 customers. Its zipper products are used in fashion and sports apparels, camping equipment, shoes, and bags by renowned brands. It also received the ‘PRC Top Ten Famous Zipper Brands’ in China. To perhaps make your job easier, a simple table of financial ratios from profit margins, ROE, cash conversion cycle (CCC) is provided. Interestingly, you might note that it is a company generating a ROE of 20.2% on profit net margin of 22.3% and trading at a modest valuation of Price-Earnings ratio 6.2x and Price-to-Book Value 1.6x, with downside protected by a seemingly healthy ‘net cash’ balance sheet with net cash comprising 27% of the market value of the company.”

| RMB Mil |

2004 |

2005 |

2006 |

2007 |

| Revenue |

394.3 |

525.7 |

716.4 |

883.9 |

| Operating Income |

91.4 |

165.1 |

226.5 |

294.5 |

| Net Income |

57.4 |

109.3 |

155.6 |

197.0 |

| GP Margin |

26.7% |

34.0% |

33.7% |

34.8% |

| OP Margin |

23.2% |

31.4% |

31.6% |

33.3% |

| Net Margin |

14.6% |

20.8% |

21.7% |

22.3% |

| ROE |

|

|

|

20.2% |

| AR Days |

137 |

167 |

139 |

121 |

| Inventory Days |

23 |

15 |

19 |

20 |

| AP Days |

12 |

17 |

18 |

18 |

| CCC |

149 |

165 |

140 |

123 |

| Mkt Cap (US$m) |

|

|

|

181 |

| Price/ Book Value |

|

|

|

1.6 |

| PE ratio |

|

|

|

6.2 |

| Net “Cash” % Mkt Cap |

|

|

|

27% |

“And we would stay on this income statement for whatever time it takes before someone points out the dog that didn’t bark,” I added.

Sometimes, there would be one or two people, often those who are open-minded and intellectually curious in their learning approach, who would point out: “The selling and distribution expense of RMB3m seems awfully low for a company generating RMB882m in sales for truckloads of zippers to be transported to over 900 of their customers’ factories in the different provinces.”

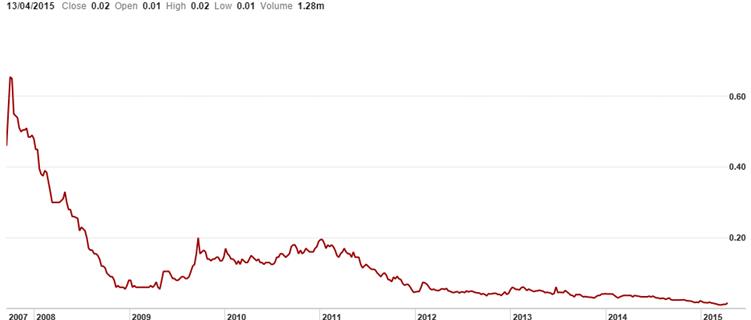

This zipper company is SGX-listed Fuxing Zipper (SES: DC9, Bloomberg: FUXC SP), down over 90% in market value. We will later illustrate how accounting tunneling fraud is carried out and the six new measures for value investors to employ to avoid such statistically-attractive fraudulent stocks. From the case of Fuxing, one of the apparent measures is based on the opportunistic shifting or deferring of operating expenses out of the income statement to boost profits artificially – often into the balance sheet items. But how do we can capture this? A possible measure is that of the “OP/OL ratio”, or “Other Payables/Operating Liabilities ratio” which we will elaborate upon later with the cases that we have observed to be a systematic phenomenon. In essence, we have observed that an OP/OL ratio over 40% leads to subsequent and future acts of accounting tunneling fraud in which corporate wealth and cash is tunneled out.

Fuxing Zipper (SES: DC9) – Stock Price Performance 2007-2015

As we have shared in earlier articles, transportation and logistical cost is a nightmare in China and emerging markets, estimated to account for 15 to 20% of the cost of doing business and of the GDP too by various sources that include World Bank and the Li & Fung group in an insightful presentation. The problem lies not only because of the geographical woes but also due to the regulatory licensing bottlenecks: “China’s logistics system is governed by nine separate ministries and commissions, which prevents the central government from regulating cross-provincial transport across China’s 31 provinces. Instead, local governments manage their transportation systems as provincial fiefdoms, often using local license rules and tolls to raise revenue. Thanks to high transaction costs, no trucking firm has yet established a nationwide network.”

The emerging Asian and Chinese companies engaging in accounting fraud often push operating expenses and overheads off the listed entities to related-party companies to boost artificially-high profit margins and ROE. For instance, an Asian consumer “brand” selling its “visible” products in supermarkets would usually shift the substantial expenses related to shelf-space placement to undisclosed related-party “distributors” and “agents” (called “tong lu” 通路 in the local language) to achieve the high profit margins and ROE that are attractive to investors. Most value investors focusing on financial ratio analysis do not realize that logistics, distribution and marketing costs in emerging Asian markets is around 15-20% of sales, instead of the 0.34% that this zipper company incurred. Like-minded value investors are often amazed that they have not seen what was now obvious to them. Thus, one simple new measure is to use the “Selling and Distribution expense as % of Sales” (Measure #1) as a sanity check on unrealistically low operating expenses that were deferred or shifted out of the income statement.

We wrote something in the article “BNSF + JB Hunt = Buffett + Munger = Lollapalooza! How About Asia?” about how logistical improvement throughout America has enabled the scaling up of retailers and businesses in a cost-effective way: “The open innovation also enabled American companies such as Petco Animal Supplies, Pepboys Auto, The Container Store, Best Buy, Lowe’s, arts & craft retail chain Michael’s, to scale up their expansion in a cost-effective way. Petco commented, ‘Despite a 27% growth in stores since 2008 – from 870 to 1,100 – our transportation spend on a cost-per-delivery basis has remained relatively flat. If you had told me we could add that many stores without raising the transportation costs, I wouldn’t have believed you.’”

The above excerpt talking about pet shop Petco highlights one of the important real-world cost concept in doing business: cost-per-delivery or in general, cost-per-activity. Many Asian entrepreneurs whom we have talked to over the past decade plus had lamented their problems in scaling up their business to get a decent valuation beyond the billion-dollar market capitalization barrier. They mentioned how sales might perhaps tripled in five or ten years, but core business profit growth (excluding deal-making trading profits) might remain flat or even decline, and a key reason (from a simple cost perspective) is that Selling, General and Administrative (SG&A) cost, thought by many to be a “fixed” or at least a “semi-fixed” cost, had increased even faster than sales. Rather than SG&A costs being fixed or even variable, these costs had become “super-variable” – increasing faster than sales.

The impatient entrepreneurs seeking their payday resorted to opportunistically manipulating this SG&A cost to improve dramatically their profit margin in the eyes of investors by shifting or deferring this expense item into the balance sheet items that include “Accrued Expenses”, “Other Current Liabilities”, “Other Non-Current Liabilities”, “Deferred Tax Liabilities” and so on, giving the excuse that these expenditures provide long-term payoffs which are unlikely to materialize and hence they should be expensed off. We classify and sum these up as “Other Payables”. A closer examination into the footnote disclosure would reveal these include loans due to directors, amount due to related-parties.

A common IPO fraud ruse by the insiders and investment bankers is for the directors to first borrow some short-term financing from the banks, using part of the borrowed money to create set-up customers to engage in fictitious sales with the IPO company. Once the IPO proceeds are raised, the loans to directors and amount due to related parties are repaid with other people’s money (OPM) – often disguised as under the purpose of “IPO proceeds used for working capital purposes”.

Another is to use the IPO company to buy equipment, goods and services at inflated value from their related companies. Equipment worth $20m is invoiced to the IPO company at $100m from the related company, with the insiders pocketing the “free” $80m profit which they either pump back to the company to boost artificial sales or to convert as “personal” investment into “free” equity into the IPO company in a show of “ownership commitment” in the eyes of the unsuspecting investors. This is often disguised as under the purpose of “IPO proceeds used for PPE, factory expansion and capex investments”. In the case of the accounting tunneling fraud through PPE and capex (we coined it as “Grand Capex Fraud” in our earlier articles), we will elaborate upon this in another future article.

As for deferred tax liabilities, joint-controlled entities and associates…

<ARTICLE SNIPPED>

In addition, the OP/OL ratio = Other Payables (OP)/ Operating Liabilities (OL) (Measure #6), a ratio in which we have observed that crossing over the unusually high 40% (as opposed to under 20% for the typical companies) leads to subsequent and future acts of accounting tunneling fraud in which corporate wealth and cash is tunneled out. In the case of Fuxing Zipper, the OP/OL ratio in 2007 and 2008 is 44% and 52% respectively, as opposed to around 19% for YKK for instance.

<ARTICLE SNIPPED>

In the case of Fuxing, let’s apply the below measures to detect the accounting transgression ahead of the curve before FY09-12:

- Bloated Balance Sheet (Measure #2)

- Measure #3

- Measure #4

- Measure #5

- Measure #6

|

2004 |

2005 |

2006 |

2007 |

2008 |

| Part C: The Tunneling Measures |

|

|

|

|

|

| Measure #2: Bloated Balance Sheet |

80% |

75% |

74% |

53% |

64% |

| Measure #3 |

|

-3% |

20% |

108% |

|

| Measure #4 |

|

|

|

38% |

47% |

| Measure #5 |

|

|

|

79% |

130% |

| Measure #6: OP/OL |

|

72% |

27% |

44% |

52% |

<ARTICLE SNIPPED>

… the set of tunneling measures reveal that lurking beneath the deceptively attractive financial ratios and valuation metrics is the hideous Picture of Dorian Gray with all the sins hidden.

This is what we wrote in Aug 28, 2013 and we still feel very strongly, if not more so, about what we have written since:

“This prevalent situation in Asia is analogous to that of the Picture of Dorian Gray in the novel by Oscar Wilde (1890) – the face of Dorian Gray showed no signs of aging as time passed, whereas the sins of his worldly existence are vivid in the portrait of himself that he kept hidden in the attic. The Dorian Grays of Asia have been able to get away with their accounting frauds and misgovernance transgressions because they are branded as sexy growth companies who charm party-goers with their good looks (quantitative financials) and riding on “The Asian Growth Story”.

At Bamboo Innovator, our task is to support fellow value investors to understand and appreciate the early signs of potential problems and red flags in Asian companies ahead of the market, to see the real attic portrait of the companies’ financial health and economic worth.

We still hold on feverishly to the idealistic hope that a community of like-minded people can come together to spread their knowledge and kindness built around a resilient mental model, a home that everyone can breathe in it and make it their own. We hope that our candid and authentic views about value investing can be shared in our little community.

Thus, despite self-doubts all the time, this mission to create value for our readers with the Bamboo Innovator analytical framework has pulled us forward to devote nights after nights and squeeze every ounce of our bludgeoned body to do this. This is why we care so much about doing The Moat Report Asia for you.

Having the inner compass of the Bamboo Innovator in our hearts can help us not lose our way in difficult and uncertain times as we journey together in the dangerous Asian capital jungles.”

Warm regards,

KB

The Moat Report Asia

www.moatreport.com

http://accountancy.smu.edu.sg/faculty/profile/108141/KEE-Koon-Boon

A new monthly issue of The Moat Report Asia is now available!

Access the in-depth idea presentation:

http://www.moatreport.com/members/

Paid subscribers get:

- The Monthly Moat Report Asia (20 issues)

- Bonus Content: The Weekly Bamboo Innovator Insight Articles (>70 Issues)

- Bonus Content: Access to the Members’ Forum

- Bonus Content: Videos and Presentations by Thoughts Leaders, Entrepreneurs and Business Leaders in Asia

|