Long-Term Contract Accounting Fraud in Asia From Construction to Software

May 19, 2015 Leave a comment

| “Bamboo Innovators bend, not break, even in the most terrifying storm that would snap the mighty resisting oak tree. It survives, therefore it conquers.” |

| BAMBOO LETTER UPDATE | May 18, 2015 |

Bamboo Innovator Insight (Issue 83)

|

| Dear Friends,Long-Term Contract Accounting Fraud in Asia From Construction to SoftwareA Dreamer and an Accountant is a lethal combination. McDonald’s Ray Kroc had financial wizard Harry Sonneborn to advise him that real estate was the key to a franchise’s financial success. Thomas Edison had his right-hand business partner Samuel Insull who took care of financing, operations, hirings, firings and mergers.Tanaka Hisashige and Ichisuke Fujioka, the “Thomas Edisons of Japan”, must have wished there is a competent accountant to exercise financial stewardship over their business creation Toshiba (6502 JP, MV $14.6bn). Toshiba was involved in an accounting scandal in inflating profits by over ¥50bn ($419m) for the three year cumulative period through FY13 after calling for an urgent press conference at its headquarters in Minato City, Tokyo, on 15 May 2015 to appoint an independent investigation committee to probe the accounting issues, four years after the Olympus accounting fraud revelation in 2011 that hid $1.7bn in losses in a 13-year cover-up.Starting from a small workshop rented from the second floor of a temple in Roppongi, Tokyo in 1873, six years after the Meiji Restoration and at the age of 74, Hisashige-san produced the first telegraph equipment in Japan. After meeting Thomas Edison in 1884 while on a tour in the United States, Fujiioka-san pledged to devote himself to establishing a Japanese electric power industry, succeeded in developing an economical, durable light bulb and in constructing an electric railway, taking Japan into the age of electricity. Hisashige’s firm, later renamed Shibaura Engineering Works, merged with Fujiioka’s Tokyo Electric Company to form Tokyo Shibaura Electric, which soon became known as Toshiba.

The in-house investigation into the accounting scandal relates to the underestimation of costs for 9 out of the 250 projects using the percentage-of-completion (POC) accounting method: 4 projects totalling ¥6bn at the power systems company, 4 projects totalling ¥30bn at the social infrastructure systems company and one project totalling ¥14bn at the community solutions company. Toshiba derived around 11% of operating income from its power and social infrastructure business. This is the second accounting investigation in less than two years for Toshiba, which has twice delayed reporting its earnings for the year ended in March because of irregularities. The new panel’s probe will extend to Toshiba’s 593 consolidated subsidiaries, including electrical engineering giant Westinghouse Electric, owned by Toshiba since 2007. Toshiba and one of its listed subsidiaries, Toshiba Plant Systems & Services (1983 JP, MV $1.2bn), are also members of the JPX-Nikkei Index 400, which was started last year to showcase Japan’s best shares to institutional investors and shame executives of companies that weren’t picked into improving capital efficiency to make the cut. It selects the 400 companies in Japan with the highest return on equity and profit over the past three years. Corporate governance is another factor in choosing the members. The gauge recalculates its constituents every year using data from the last business day of June, and publishes the results in August. Sony Corp was among 31 members that got replaced in 2014. Interestingly, Toshiba has four outside board directors, an apparent sign of good “corporate governance” to keep checks and balances on the managers. Toshiba is now in a race to report its restated earnings before the June 30 deadline. Toshiba risks losing the attention of about ¥650bn tracking the JPX-Nikkei 400 in exchange-traded and mutual funds should it get kicked out of the JPX-Nikkei Index. We wish to highlight the area of revenue recognition and the accounting for long-term contracts, in particular the percentage-of-completion (POC) accounting method, which has received relatively little inspection from academics and practitioners. There are important implications for value investors given that the POC accounting method is common across industries from construction/infrastructure/property and defence to software. In essence, long-term contracts present special problems for revenue recognition, which allows for both the POC method and the completed contract method (CCM). Under the CCM, no revenue is recognized until the project is 100% complete; and, the related project costs are held as inventory. The POC method recognizes revenue and costs as measurable important progress milestones on a project (output-based measure) or based on a ratio of costs incurred to date over expected total contract costs (input-based measure 1: cost-to-cost method) or based on comparing measures such as labor hours, labor dollars, machine hours or quantities of material consumed to date to the total quantity estimated forte entire project (input-based measure 2: efforts-expended method). Under the POC method, managers can opportunistically manipulate the percentage of completion to recognize revenue prematurely and conceal contract overruns. The following can be manipulated to affect revenue recognition:

Note: Should the above red flags be found, value investors should adjust downward the revenue by an amount that is the difference between unbilled receivables (or amount due from customers in contract work) and the work-in-progress (WIP). Past prominent cases involving POC accounting fraud include:

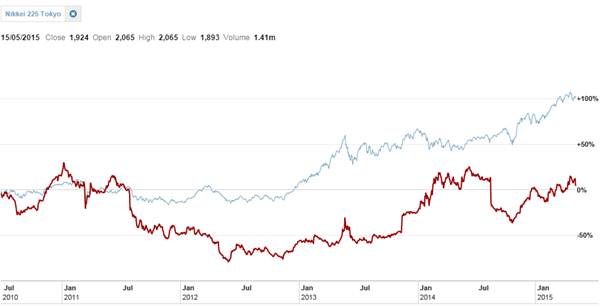

Recent accounting scandals in Asia who had potentially abused the POC accounting method include water treatment company Sound Global (967 HK, $1.36bn) whose auditors identified audit issues of missing RMB2bn cash shortfall and had reported matters to Singapore’s Ministry of Finance in an announcement on May 4, around three months after allegations of fraud by Emerson Analytics which the company denied with the media supporting the management and blasting the short-seller for the unfair attack. For instance, unbilled receivables (amount due from customer for contract work) at Sound Global soared over five-folds from RMB203m in FY09 to RMB1.1bn in FY13, representing around 15% and 35% of sales respectively, an indication of aggressive revenue recognition before projects are actually completed in the subjective use of the POC accounting method. Managers often opportunistically manipulate the estimates under the POC accounting method to inflate revenue and profits to achieve compliance with existing and future debt covenants and to raise more external financing in debt and equity. Note that the total debt at Sound Global had jumped from RMB227m in FY09 to RMB3.8bn in FY13. Another example is Japanese vacuum machinery company Ulvac (6728 JP, MV $796m). Around 2010, Ulvac reported that its full year ended Jun 2010 sales were down 1% and operating profit was up 38%. However, the result was due to the switch to POC accounting method and aggressive accounting in revenue recognition much earlier. Interestingly, Ulvac disclosed in the footnotes that had it used the same revenue recognition method as before, its sales would have been down 21% and there would be a loss. Since Jun 2010, Ulvac’s share price is flat, underperforming the 100% rise in the Nikkei index. Ulvac (TSE: 6728 JP) – Stock Price Performance 2010-2015

******** When Samuel Insull was not named the president of what is now known as General Electric, he left and went on to build a electricity utilities empire using financial engineering and complex holding companies structure carrying out M&As and became one of the richest man in the world with a personal worth of over $150m (over $1.7bn in today’s dollars). To pay for expansion, Insull had sold low-price bonds and stock. Over a million middle-class Americans bought in – but their investments were made worthless by the Great Depression. Overnight, Insull went from a hero on the cover of Time magazine to the villain who had stolen the people’s money. It was said that before Enron, there was Insull. Charged with fraud, Insull was tried in 1934 and acquitted of the charges. But his reputation was destroyed, and he left the country for good. Four years later, Insull died of a heart attack in the Paris subway in 1938 with 84 cents in his pocket. When financial and accounting wizards Harry Sonneborn and Samuel Insull left Ray Kroc and Thomas Edison respectively, they were in a “percentage of completion” mode in not being able to build an idea larger than themselves to complete the work. The awkward Dreamer and the suave professional Accountant is the “completed contract”. When separated from the Dreamer and her vision, the Accountant often flounders and loses his Way. Similarly, the technical interpretation and application of the POC accounting method cannot be separated from the wide-moat business model analysis of the company since the long-term nature of the contract with the customer determines the economic substance and viability of the business’ work in progress, of an idea larger than oneself. Warm regards, KB The Moat Report Asia http://accountancy.smu.edu.sg/faculty/profile/108141/KEE-Koon-Boon A new monthly issue of The Moat Report Asia is now available! Access the in-depth idea presentation: http://www.moatreport.com/members/ This month, we highlight a wide-moat innovator who is the #1 in Asia in a patented automotive electronics part that is part of the fast-growing Advanced Driver Assistance System (ADAS) market worth >$22bn by 2018, doubled from $11bn in 2014. The ADAS market is driven by more stringent safety requirements from governments forcing the automotive industry to develop automotive electronics solutions to increase vehicle safety. [Company’s name] is the third-largest in the world behind Valeo (FR EN) and Bosch. It has >50% market share in new cars sold in China, and the installation rate of this ADAS product on China’s auto is still low (35%+ on new cars vs 80%+ in developed markets). Established in 1979 by founder and Chairman Mr. C, [Company’s name] is one of the rare Tier-1 automotive suppliers in Asia to major OEM car makers that include Ford, GM, Daimler, Hyundai, Nissan, China’s top 10 auto companies such as Great Wall Motor, thereby directly shipped to them and involved in their R&D processes and early stage processes of concept car design and prototyping, creating a pre-emptive advantage in winning new orders. Over the past 36 years, [Company’s name] has forged formidable competitive advantages in scale, product quality, technological know-how and R&D capabilities and in May 2012, [Company’s name] outgunned illustrious industrial automotive giants Valeo (founded in 1923) and Bosch (founded in 1886) to sign a breakthrough global 10-year contract with GM, with the commencement of worldwide shipment to 18 countries and 25 factories at the end of 2016. Paid subscribers get:

|