Hoping to bring banking services to millions of people in small towns and villages, India is turning to industrial companies to set up banks, a strategy that has had bad consequences in other countries

July 5, 2013 Leave a comment

July 4, 2013, 7:22 p.m. ET

India’s Risky Step to Boost Banks

NUPUR ACHARYA And SHEFALI ANAND

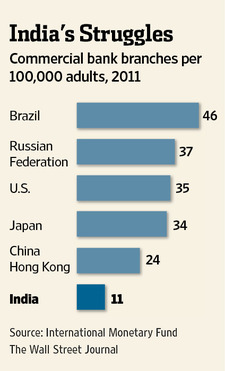

MUMBAI—Hoping to bring banking services to millions of people in small towns and villages, India is turning to industrial companies to set up banks, a strategy that has had bad consequences in other countries. Regulators are taking this risk because only one in two Indians have bank accounts in India, and one in seven have access to bank credit, according to CrisilLtd., 500092.BY +0.14% a research unit of Standard & Poor’s. State-run banks, which dominate India’s banking system, are struggling to expand due to shortage of capital. Meanwhile, foreign banks have been stymied, because all of them together are allowed to open only 12 branches a year.But India’s strategy is risky. Many countries don’t allow businesses such as manufacturers or real-estate developers to own banks because of the temptation to use cash from their customers’ accounts to lend to their own operations. That essentially allows the businesses to lend to themselves, judging their own creditworthiness, interest rates and repayment terms.

If the loans go bad, depositors could lose their savings, and the government, which provides deposit insurance, could be on the hook to make good some of these losses.

But India is taking this chance because it is running out of options to bring financial services to its vast unbanked population.

Against this backdrop, some say only industrial groups have the capital needed to expand banking in India.

Major Indian business houses such as the $100 billion Tata Group, $40 billion Aditya Birla Group and the $30 billion Reliance Anil Dhirubhai Ambani Group are among 26 companies that applied to the RBI for bank licenses on Monday, the last date for applications.

Allowing companies to run banks is “a strategy with a lot of risks,” said Russell Green, a former attaché for the U.S. Treasury in Delhi and now a fellow at Rice University in Houston. “It has proven problematic in plenty of countries in the past,” he said.

Mr. Green referred to the experience of Mexico, which had allowed companies to own banks in the 1990s, only to later find that founders were funneling the money to related companies.

South Korea also used to allow its chaebolindustrial groups to own banks, but reversed the policy after large related-party loans contributed to the country’s plunge during the 1997-98 Asian financial crisis.

In a bid to prevent self-dealing, the Reserve Bank of India has placed several restrictions on ownerships and the holding structures of the new banks.

Experts worry that the RBI may not have the ability and staff to supervise all units and related parties of these proposed banks. “It’s a challenge,” said Thomas Richardson, India representative for the International Monetary Fund, adding that the RBI will need “to have additional skills and resources to keep track of the risks.”

But some experts say India could achieve some of this growth from existing banks itself. India can “increase competition in the banking space by allowing more foreign banks,” said Ajay Shah, a former consultant to India’s finance ministry. “As the competition intensifies there will be a natural need to explore new markets,” he added.

Over the past two decades, the RBI has allowed only 12 new banks, bringing the total number of Indian banks to 48. Mumbai-based Kotak Mahindra Bank Ltd.500247.BY +0.39% and Yes Bank Ltd. 532648.BY +0.81% were the last two banks to get licenses earlier in this decade. They have expanded rapidly, setting up more than 400 branches each, but remain a small part of the banking system. India also has 31 foreign banks, of which only three have a sizable business in the country.

Companies that have applied for the new bank licenses now say central-bank guidelines have enough safeguards to ensure that the banking and other businesses of the founders remain separate.

“We are not building a bank to lend to our companies. We are doing it to build our customer franchise,” said Ajay Srinivasan, chief executive of Aditya Birla Financial Services, part of Indian conglomerate Aditya Birla Group, which has applied for a bank license.

Mr. Srinivasan said that industrial groups over the years have successfully brought mobile phones and automobiles to semiurban and rural India. “There is no reason why the banking sector should not benefit from this,” he added.

An email sent to the Tata Group spokesperson remained unanswered while Reliance declined to comment.

The RBI hasn’t said how many licenses it will issue or how long it will take to approve them, but experts say it will take at least a year.