Getting a Handle on Twitter’s Value; Investors Must Look Beyond the Basics to See Just How Expensive Twitter Really Is; diluted market value of $31.7 billion means Twitter trades at 33 times 2014 sales estimates

November 8, 2013 Leave a comment

Getting a Handle on Twitter’s Value

Investors Must Look Beyond the Basics to See Just How Expensive Twitter Really Is

MIRIAM GOTTFRIED

Updated Nov. 7, 2013 6:03 p.m. ET

The wait is over, and the market has spoken, or rather, tweeted. But when it comes toTwitter‘s TWTR +72.69% size, and valuation, the message is easily garbled. After pricing late Wednesday at $26, shares of newly public Twitter opened at $45.10 Thursday. According to most financial databases, that means the micromessaging service has a market value of $25 billion. That is open to debate.

Twitter’s initial public offering, like Facebook‘sFB -3.18% before it, provides a window into why it is crucial for investors to focus on diluted share counts and stock-based compensation when valuing highflying social media and tech companies. Failing to do so can lead investors to pay far more than they realize for a stock, a particularly big risk in Twitter’s case given its heady valuation.

Twitter’s $25 billion market-value figure is based on 555 million shares outstanding—the headline number in Twitter’s IPO filing. But such basic share counts don’t take into account options, warrants and restricted stock. Altogether, Twitter has 150 million such shares, according to its IPO filing, bringing its total share count to 705 million.

Another adjustment is necessary for options and warrants. When those are exercised, Twitter will receive cash equal to the number of options multiplied by their weighted average exercise price. For the purpose of analysis, investors typically assume a company will reinvest the combined proceeds into buying back shares. That lowers Twitter’s diluted share count slightly to 704 million.

But that boosts its market value to $31.7 billion—or $6 billion more than its capitalization based on a basic share count. This only intensifies the pressure on Twitter to demonstrate that it can bring its revenue in line with its lofty valuation, while also underscoring how frothy the share price is, especially following its stunning first-day gain of 73% above the listing price.

Using its basic market capitalization, Twitter opened at about 26 times 2014 sales estimates. Using the diluted market value, the multiple rises to 33 times. That gap should close somewhat over time since companies like Twitter tend to issue fewer options and restricted stock following an offering.

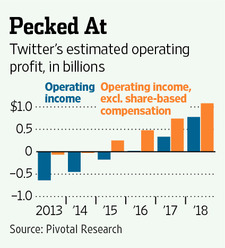

Still, the issue of dilution isn’t going away. While Twitter pointed investors to an earnings metric in its IPO filing that excluded stock-based compensation expense, that could continue to stand in the way of its gaining profitability on the basis of generally accepted accounting principles.

To attract and retain the best employees, Twitter will either need to pay them with shares or with cash. Brian Wieser, an analyst at Pivotal Research, estimates Twitter’s share-based compensation expense will be $430 million in fiscal 2014. Although that would be down from $580 million in 2013, future dilution will likely amount to an additional 1.5% annually, bringing Twitter’s share count to 777 million by 2018, he estimates.

As it is, Twitter’s value rests on a lot of vague assumptions about factors that affect the company’s ability to increase revenue, such as scale, engagement and the often fickle tastes of tech users. With the horizon so hazy, investors should at least be clear about their starting point.