Abenomics Faces Emerging Pressures

November 11, 2013 Leave a comment

Abenomics Faces Emerging Pressures

Trouble in Developing Markets Blurs Growth Picture

TAKASHI NAKAMICHI

Updated Nov. 10, 2013 5:31 p.m. ET

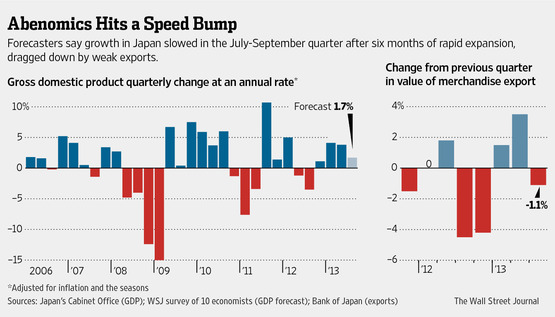

Japan is expected to report this week that its economic-revival experiment hit a speed bump over the summer, with growth for the three months through September likely slowing to less than half the pace recorded in the first half of the year. That doesn’t necessarily mean Abenomics—Prime Minister Shinzo Abe’s master plan involving weakening the yen and temporarily boosting infrastructure spending—is faltering.But Thursday’s report will underscore some key points about the country’s recovery from its two-decade slump. Progress remains fragile, vulnerable to market gyrations at home and abroad, especially in emerging markets from Indonesia to Brazil. And for all the talk of retrofitting the mechanics of Japan’s economy to rely more on domestic private demand, the growth engine still depends heavily on government stimulus and exports.

“Abenomics is off to a good start,” Jerry Schiff, the International Monetary Fund’s mission chief to Japan, said in a speech this past week at the Peterson Institute for International Economics in Washington. “But in some sense, the hard work remains to be done.” Economists polled by The Wall Street Journal say Japan’s economy likely posted annualized growth in gross domestic product—the broadest measure of a nation’s goods and services—of 1.7% in third quarter, slower than the 2.8% rate for the U.S. and a sharp deceleration from the 3.8% and 4.1% rates of the prior two periods, when Japan outgrew the other Group of Seven advanced economies.

The implications of a possible Japanese slowdown go beyond Tokyo, as policy makers around the world have been hoping that a resurgent Japan could, for the first time in a generation, provide a lift for the global economy. As Mr. Abe himself said earlier this year in unveiling his growth strategy: “Now is the time for Japan to be an engine for world economic recovery.”

For now at least, rather than Japan pulling up global growth, softer overseas markets are tugging Japan down. One reason for the likely summertime deceleration: a falloff in exports over the past few months. In the Journal survey, economists estimate a drop of nearly 2% for the July-September period, a sharp reversal from the double-digit export growth enjoyed over the prior six months.

Much of the problem lies in emerging markets, now the destination for two-thirds of all Japanese exports, according to the Finance Ministry. The IMF cut its global growth projections as those economies have slowed recently amid market volatility sparked by uncertainty over how long the U.S. Federal Reserve will run full-bore with its easy-money policies.

“Conditions are harsher than what we had anticipated…due to the negative impact from the slowdown in emerging markets,” Masaru Kato, chief financial officer of Sony Corp.6758.TO -1.09% , told reporters last month, explaining why the electronics giant reported weak quarterly results and slashed its earnings forecast. “We expect tough conditions to continue for some time,” added Sony senior vice president Shiro Kambe, citing weakness in Latin America and the Middle East.

Another early growth generator from Abenomics—a jump in consumer spending—is also wearing off. The initial burst of optimism sparked a surge in Tokyo stocks early this year, which prompted wealthy consumers to open their pocketbooks. But share prices have since leveled off as the markets have gotten used to the policy shift, and spending has leveled off as well. Consumption likely posted its weakest growth in four quarters, just 0.4% in the July-September period, according to government figures.

One big factor pumping up the economy in the third quarter: government-funded public works. Infrastructure spending likely jumped an annualized 35% on the ¥10.3 trillion ($104 billion) stimulus package passed by parliament earlier this year, helping muffle weakness in other sectors. “When exports are weak, the government just spends away to drive the economy forward. This pattern has hardly changed,” said Ryutaro Kono, chief economist at BNP Paribas Securities.

The government is planning a fresh ¥5 trillion spending package for next year as well. Yet, saddled by public debt worth over 200% of GDP, more than double the U.S.’s debt ratio, Japan’s government may find it difficult to keep spending at such a pace.

Consumer spending is all but certain to accelerate and lift growth over the next six months—but that spending is widely seen as artificially and temporarily inflated as consumers rush to make purchases in advance of an April sales-tax increase enacted to contain the country’s debt.

At that point household consumption is likely to drop—unless Japanese firms raise wages and salaries during annual labor negotiations next spring, something a majority of them have avoided since the early 2000s. Policy makers are openly prodding executives to do so, and a sharp jump in profits—the result of a weaker yen making Japanese exports more competitive in global markets—would seem to make that feasible. Net profits for listed Japanese firms have, on average, more than doubled for the six months ended Sept. 30, compared with a year earlier, according to SMBC Nikko Securities.

An income boost would offset the tax increase and give consumption a fresh, sustainable lift. That is the “virtuous cycle” scenario for Abenomics.

But some companies, such as Sony, are now marking down earnings forecasts for the next few months. And if strong growth doesn’t continue through the spring, employers may hold off hiring or reduce bonuses, which would cancel out the benefit of the pay raise.

In the IMF World Economic Outlook last month, Japan’s GDP was forecast to grow 1.2% next year, below the 2.0% pace for advanced economies, with domestic demand growing just 0.6%, about the same as the still-anemic euro zone.

Pressure is thus on the Bank of Japan, 8301.TO +1.34% whose radical monetary easing has played a major role spurring growth to date. The markets expect the BOJ will take additional measures in spring to limit the economic blow from the sales-tax increase. But the BOJ is already buying assets at a furious pace, absorbing 70% of newly issued government bonds, and it is unclear how much more the central bank can do.

So that means the Japan growth story, at least for the foreseeable future, will rely on “external demand”—exports—to pick up the slack. And that is a question mark.