Signs Multiply That Sentiment Is Too Upbeat; Surveys of Retail Investors, Advisers, Point to Froth

November 11, 2013 Leave a comment

Signs Multiply That Sentiment Is Too Upbeat

Surveys of Retail Investors, Advisers, Point to Froth

SPENCER JAKAB

Nov. 10, 2013 5:44 p.m. ET

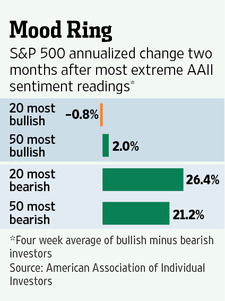

For those worried that irrational exuberance is back, Twitter Inc. TWTR -7.24% ‘s hyped initial public offering provides yet another bit of anecdotal evidence. More quantifiable measures of investors’ mood going into the end of 2013 may support that view, too. A particularly worrisome one is the Investors Intelligence gauge of adviser sentiment. Its last reading showed that 55.2% of respondents were bullish and just 15.6% bearish, tying the highest difference between the two this year. The last time the gap was bigger was April 8, 2011, which preceded the sharpest stock-market correction of the current bull market.Another signal of froth comes from a weekly survey of retail investors by the American Association of Individual Investors, which has been tracking sentiment since 1987. Though it is volatile, a four-week average of the difference between bullish and bearish respondents is the highest since February and near the upper end of the historical range since 1987.

In the two months following the most bullish 10% of readings, the S&P 500 proceeded to fall at a 1.4% annualized pace on average. The market did well following the most bearish survey periods, rising by 15% on average at an annualized rate. And while there can be a difference between what people say and do, respondents’ allocation of money to equities is at the highest since right before the last bear market began.

Those sentiment measures, coupled with the recent spike in bond yields, have Peter Boockvar, chief market analyst at the Lindsey Group, thinking the stock market may be near its peak for the year. His reading of interest rates seems counterintuitive at first. Market history will show that stocks were more likely to be thriving during periods of rising interest rates than at other times. That is because increasing bond yields coincided with an improving economy.

“You can throw that relationship out the window,” says Mr. Boockvar, who notes the Federal Reserve is the key mover now and may be losing its ability to control the long end of the yield curve. That would remove a key bullish investing thesis.

Of course, timing peaks in equities based on past patterns is fraught with peril. At least one thing about the next bear market, whenever it arrives, will be different. This one will be tweeted.