Buffett’s favorite market tool is flashing red

November 12, 2013 Leave a comment

Buffett’s favorite market tool is flashing red

This little-known valuation metric has entered familiar territory. Here’s why investors should share the Oracle of Omaha’s concerns — and how they can protect themselves.

By David Sterman

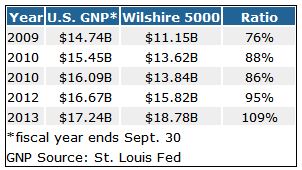

In the go-go days of 1999, Warren Buffett grew very concerned. Not because his value style of investing had grown unpopular, but because investors were becoming delusional in their zeal for further gains. In a speech he made to friends, as recounted in a 1999 article in Fortune magazine (that was published just a few months before the market peaked and then plunged), Buffett warned that “once you reach the point where everybody has made money no matter what system he or she followed, a crowd is attracted into the game that is responding not to interest rates and profits but simply to the fact that it seems a mistake to be out of stocks.” A simple test of how much stocks were loved: The aggregate value of the largest 5,000 U.S. companies (as measured by the Wilshire 5000) exceeded the GNP of the U.S. economy. In fact, a market melt-up took this ratio up to 150% by early 2000 (meaning the Wilshire 5000 was 50% larger than the U.S. economy), which set the stage for one of the most painful corrections ever for investors.This ratio eventually dipped well below 100%, which for Buffett has been seen as a time of deep value for stocks. “If the percentage relationship falls to the 70% or 80% area, buying stocks is likely to work very well for you,” he told Fortune in a 2001 follow-up.

Indeed stocks went on to deliver solid gains into that decade, but by 2007, Buffett’s handy ratio again flashed red. Stocks were becoming so frothy that this measure once again exceeded 100%. The resulting market blow-off in 2008 was another painful lesson for investors, but at least put the market deep into value territory, setting the stage for the bull market we’ve been enjoying ever since.

Yet as we head towards the end of 2013, investors need to once again tread cautiously, because Warren Buffett’s market valuation tool is again in the red zone.

The Wilshire 5000 has risen 68% since the end of 2009. Yet the economy has grown just 17%, throwing this key ratio out of whack.

Is this time different?

There is a pair of pretty good explanations to justify the current 109% ratio. First, interest rates are near historic lows (though they are unlikely to fall much lower and more likely to rise in coming years, turning this tailwind into a headwind).

More importantly, corporate profit margins are at all-time highs, so every dollar of corporate sales is worth more than it used to be. What should we infer about profit margin trends and their impact on the market? Well, profit margins tend to surge in the early phases of an economic recovery as companies maintain very lean headcounts and restrain discretionary spending. Yet as an economy recovers, companies finally invest in more staff and equipment, which tends to push profit margins back down to historical norms.

And if margins have peaked, how will stocks fare? A study by Brown Brothers Harriman suggests stocks can still rise — but on the three of the past seven times occasions when margins have peaked, stocks fell by double digits the following year.

Risks to consider: As an upside risk, robust economic growth would provide the chance for companies to maintain current margin levels, as a higher fixed overhead is matched by rising revenues. Yet few are calling for robust U.S. economic growth in coming years.

Action to take: The Wilshire-to-GNP ratio is stretched, but it could well go even higher for a while, as was the case in 1999. Yet a clear margin for error has been removed from this market, and there is ample reason to shift your portfolio into a defensive posture. That means missing out on further upside in the aggressive growth segments of the market, but also means a greater chance of capital preservation.