Emerging Currencies Are Pressured Anew; Looming Fed Pullback Sparks Selloff

November 14, 2013 Leave a comment

Emerging Currencies Are Pressured Anew

Looming Fed Pullback Sparks Selloff

ANJANI TRIVEDI

Updated Nov. 12, 2013 6:56 p.m. ET

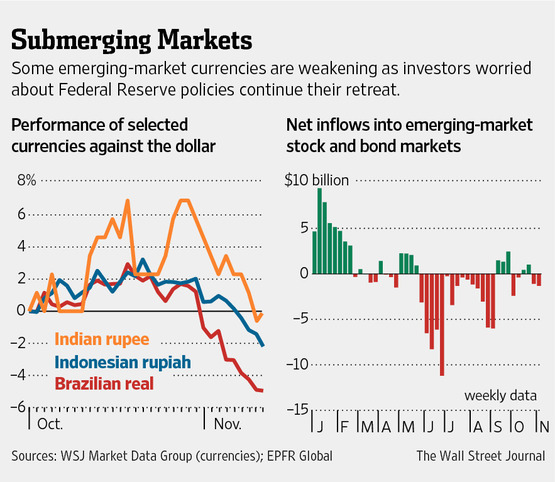

Investors worried about a cutback to the Federal Reserve’s easy-money policies are withdrawing from some emerging markets, sparking a currency selloff that echoes last summer’s rout. The stronger-than-expected October U.S. jobs report, released on Friday, heightened expectations that the Fed could be just months away from scaling back, or tapering, its $85 billion a month of bond purchases. Taken together with other positive indicators about the U.S. economy, the jobs report spurred a rise in U.S. bond yields, which many money managers said lessens the allure of emerging markets.Over the past several years, low interest rates and easy-monetary policies in the developed world sent investors on a hunt for higher-yielding assets in emerging markets. As bond yields have risen in the U.S. and other Western nations, investors have pulled money out of developing economies.

Several emerging-market currencies fell for the third consecutive trading day on Tuesday. Since the start of the month, India’s rupee has declined 3% against the dollar. The Brazilian real has fallen 3.2%, and Indonesia’s rupiah is off 2.2%.

While the scale of the declines pales in comparison with a three-month selloff that began in mid-May, many investors already are starting to exercise caution. Nima Tayebi, a portfolio manager at J.P. Morgan Chase & Co. unit J.P. Morgan Asset Management, recently has pared back emerging-market exposure.

“The price action shows that people are nervous of taking longer-term bets,” Mr. Tayebi said. He has sold the Mexican peso, the Korean won and Indonesian rupiah-denominated government bonds.

Even before the jobs data, investors had started to pull funds out of emerging markets. Emerging-market fund managers yanked $1.32 billion out of stock and bond markets in the week ended Nov. 6, according to data provider EPFR Global. That compares with weekly inflows of $2.44 billion as recently as late September.

Last summer’s selloff was trigged by statements made in May by Federal Reserve Chairman Ben Bernanke, who signaled that the central bank could take steps to taperbond purchases. In the weeks following Mr. Bernanke’s comments, the Indian rupee and the Turkish lira hit record lows against the dollar, while Brazil’s real fell to four-year lows versus the greenback.

To be sure, some investors said they aren’t expecting the selloff in emerging markets to match the exodus during the summer. Individual investors and those with relatively short investment time frames fled emerging markets from May to August. Now, some institutional investors with longer-term outlooks said emerging-market assets still look cheap despite the risks.

While some investors and analysts expect the Fed to begin curbing its easy-money policies soon—some think as early as December—many see other major central banks, including Europe, the U.K. and Japan, in easing mode for months, if not years, to come. That is likely to keep yield-seeking investors coming back to high-yielding emerging markets, some money managers said.

“I don’t expect the same volatility that we got in May, June and August,” said Edwin Gutierrez, portfolio manager at Aberdeen Asset Management, which has $312 billion under management.

Mr. Gutierrez noted that currencies of countries such as Indonesia, Turkey and Brazil are less vulnerable now due to interest-rate increases, which act to draw in investors. Mr. Gutierrez’s fund holds the Mexican peso and the Indian rupee and government bonds denominated in the Brazilian real.

Some emerging-market central banks already are fighting back. Indonesia unexpectedly raised interest rates on Tuesday to bolster the currency and fight inflation. A weak currency pushes up the cost of imports and can stoke broad-based price increases.

As was the case earlier in the year, the developing countries that have been particularly hard-hit are those with large current-account deficits, in which imports exceed exports.

“Those that need the funding desperately, like India and Indonesia, are selling off more, and Thailand to a degree,” said Geoff Kendrick, a currency strategist at Morgan StanleyMS -0.77% in Hong Kong. The investment bank advises investors to stay away from the currencies it has dubbed for this reason the “fragile five”: the Indian rupee, Brazilian real, Turkish lira, Indonesian rupiah and South African rand.

The rand has slipped back toward its lowest levels in nearly five years as the dollar has jumped by more than 7% since late October. Against the Turkish lira, the dollar has climbed nearly 5%.

Adding to the woes in Asia, Philippine markets have declined. Stocks have fallen 4% this month, as a typhoon formed in the Pacific Ocean and devastated the islands. Meanwhile, antigovernment protests in Bangkok have weighed on sentiment in Thailand, contributing to a 1.5% decline in the SET index since Nov. 6.

“We recommend being cautious on currencies with significant external vulnerabilities or where there is little in the way of preparedness for a future tightening of global liquidity conditions,” analysts at Barclays BARC.LN -2.65% wrote in a research note.