It Pays to Look Under Tata’s Hood; Indian accounting standards give Tata discretion in accounting for R&D spending.

November 16, 2013 Leave a comment

It Pays to Look Under Tata’s Hood

ABHEEK BHATTACHARYA

Nov. 15, 2013 4:30 a.m. ET

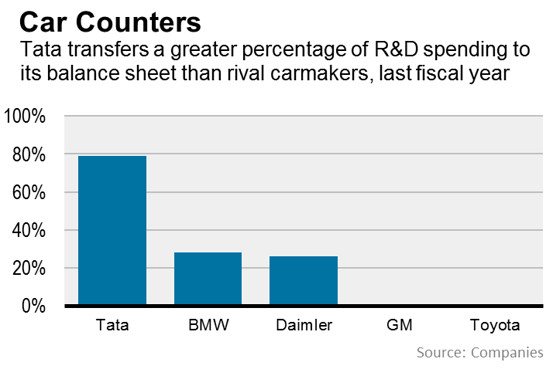

India’s Tata Motors 500570.BY +4.66% is in the big league of global car makers. When it comes to accounting for certain costs, though, it doesn’t play exactly the same way as its peers. India’s largest auto company by market value leapt onto the world stage after buying JaguarLand Rover in 2008. Now that the British luxury car maker makes up roughly 80% of Tata’s revenue, this Indian firm is competing with BMW, BMW.XE -0.06% Mercedes-Benz and a host of American and Japanese premium brands. And when compared with some of these peers, Tata looks to be a relative bargain. Although its shares are up more than 20% so far this year, the stock trades at 9.6 times estimated profit for the fiscal year that ends next March. That is at a discount to Daimler, which owns Mercedes, and BMW. Yet Tata’s valuation may be flattered by the way it treats certain costs. This has the effect of boosting its profit—in the near term, at least. Taking that into account, Tata is more expensive than it initially appears. At issue is how Tata treats research and development costs. Tata’s R&D program, at 6% of sales, is higher than the 4% or 5% global car makers typically spend on new products and designs.Indian accounting standards give Tata discretion in accounting for such spending. The company can treat it as an immediate expense that cuts into income. Or it can capitalize the spending, recognizing it over a longer period of time. Tata capitalized roughly 80% of R&D activity last fiscal year. In this, Tata is ahead of Indian counterparts—Indian SUV-maker Mahindra & Mahindra capitalized 44% of its R&D last fiscal year.

Tata’s practice also contrasts with global rivals. American and Japanese car makers expense all their R&D spending, as local accounting rules require. German auto makers, who report under international accounting standards, can capitalize R&D, though this has averaged only a third at BMW the last five years.

To be sure, Tata may need more R&D than BMW and Mahindra. JLR sported outdated models and platforms before 2008, and Tata says it’s treating the British unit as a young company hungry for new designs. The company says it has followed this practice for years, meaning it isn’t changing course.

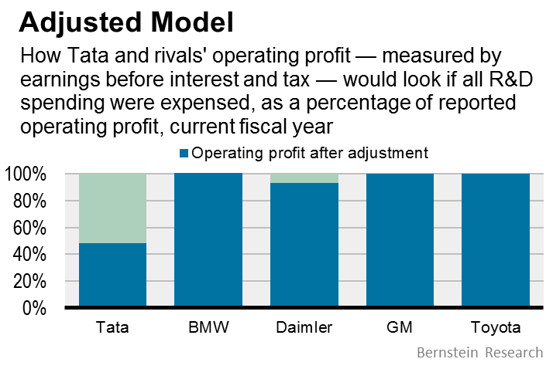

Still, Tata’s R&D accounting bolsters the bottom line. If all R&D spending were expensed, Tata’s net profit for this fiscal year would fall by two-thirds, estimates Bernstein Research. Tuning the numbers this way decreases earnings by 10% at Daimler. And at BMW, it actually boosts earnings 1% since this car maker amortizes older R&D spending and bears the expense on its income statement.

Adjusting for R&D this way, Tata’s valuation would rise to 28 times this fiscal year’s earnings. Valuations at Daimler and BMW come in at 11.3 times and 10.1 times, respectively, after similar adjustments. Meanwhile, Tata will have to amortize R&D spending once the cars under development hit the market. This will crimp profits down the line.

Investors are revved up about Tata because sales of Jaguars and Land Rovers are growing faster than rivals such as BMW. But they should kick the accounting tires before driving away with the stock.