Competitors are working hard to break up Qualcomm’s dominance, but the company maintains a strong lead. Its latest LTE baseband chips are in their fourth generation, while rivals are launching their first.

November 22, 2013 Leave a comment

Qualcomm Is Still a Smart Bet

DAN GALLAGHER

Updated Nov. 21, 2013 4:27 p.m. ET

Some may believe the party’s over at Qualcomm, QCOM +0.96% but it is too early for last call. The stock has jumped 18% over the past four months and just hit its highest level since an inflated dot-com run-up back in 2000. Qualcomm also just notched a three-year run averaging 31% annual revenue growth and warned investors in its last earnings call that the current fiscal year would see a notable slowdown from those levels.But the company has many things going its way, some of which are likely to come into play in the coming year.

Gartner projects global smartphone shipments to increase by an annual average of 20% over the next four years, even as the high end of the market slows. This will boost sales of Qualcomm’s baseband chips, a key component that manages a device’s radio connection to wireless networks and represents the largest portion of the company’s revenue.

Increasing demand for tablets has a similar effect, especially as more competing devices gain share against Apple’s iPad. Many of those rival tablets also are using Qualcomm’s Snapdragon processor, including the latest versions of Samsung’s Galaxy Tab, Amazon’s Kindle Fire and Google’s Nexus.

Competitors are working hard to break up Qualcomm’s dominance, but the company maintains a strong lead. Its latest LTE baseband chips are in their fourth generation, while rivals are launching their first.

Intel, INTC +2.73% flush with cash and challenged by a slowing PC market, wants more presence in the mobile-device business—and badly. But the company has so far managed to get its chips into relatively few smartphones and high-volume tablets. Qualcomm faces more competition from MediaTek

2454.TW +2.17% with regards to lower-tier devices in developing markets like China. But Qualcomm has historically been weak in this segment anyway, so any headway it makes will add to the top line.

China, in fact, represents even more of an opportunity for Qualcomm as the country’s wireless carriers build their LTE networks. This will increase demand for Qualcomm’s chipsets and royalties to its licensing business. About 30% of overall revenue comes from licensing its deep portfolio of wireless patents, and high margins on these mean they accounted for nearly 70% of the company’s pretax earnings in fiscal 2013.

Some investors have worried that the licensing business could be approaching a cliff. The concern is that much of Qualcomm’s patent portfolio has its base in older 3G technologies and their usefulness will wane as more devices become LTE-only.

But at an analyst meeting in New York on Wednesday, the company said that if the customers who currently hold bundled license deals went to deals that covered LTE only, this would cut revenue for the licensing arm by less than 5%.

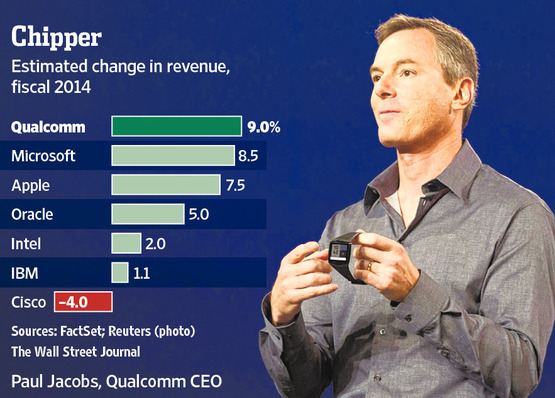

Qualcomm’s stock trades at 13.8 times forward earnings, about 16% below its five-year average, according to FactSet. The high end of the company’s revenue-projection range for fiscal 2014 still implies double-digit-percentage growth. That is above the consensus forecasts for other big tech companies including Apple, Microsoft and Oracle.

Qualcomm also plans to return about 75% of free cash flow to shareholders over the next five years, up from 62% over the last five. That target strongly suggests an increase in the company’s dividend yield, which, at 2%, lags behind many of its tech peers.

Qualcomm’s strong run of late makes taking profits a tempting idea. But investors should keep some chips in this game.