The Balkanisation of banking: Putting Humpty together again; Regulators risk fatally fracturing the financial system. It need not be so

November 23, 2013 Leave a comment

The Balkanisation of banking: Putting Humpty together again; Regulators risk fatally fracturing the financial system. It need not be so

Nov 23rd 2013 |From the print edition

OF THE many things that keep financial regulators awake at night, perhaps the most alarming prospect is the collapse of a sprawling international bank with local operations. “The one thing they don’t want to be blamed for is if a big foreign bank blows up in their market,” says a senior executive at just such a bank.The anxiety is natural. Huge progress has been made since the financial crisis in making banks safer in general, and in giving authorities the tools they need to deal with the collapse of even very large domestic banks. But if a big cross-border one were to teeter, bank supervisors would in essence face the same choice they did five years ago: bail it out using taxpayers’ money or allow a messy collapse that could freeze the financial system and the economy while spilling contagion and losses across borders.

In search of more palatable options, bank regulators around the world have considered two alternative strategies to deal with the problem of banks that span borders. The first is to craft global rules that would allow the resolution of big international banks from the top down, treating them in death as the global entities they were in life. The Financial Stability Board (FSB), a club of supervisors and central banks, has produced a detailed set of principles showing how regulators could work together to achieve a top-down resolution of a cross-border bank. At the end of last year the Bank of England and the agency charged with winding up failed banks in America, the Federal Deposit Insurance Corporation, issued a joint paper outlining plans to work together if any of their big banks were to implode. Yet daunting barriers remain.

A global system to handle failures of international banks would require regulators in different countries to place a great deal of trust in one another. Officials in all the countries where a wobbly bank has operations would have to believe they will be treated fairly if they are not to grab all of the assets they can get their hands on. Yet trust is fleeting in times of crisis.

One way of building cross-border confidence would be to have banks’ parent companies buy convertible debt issued by their subsidiaries. This would be written down if the bank got into trouble, ensuring that losses from an ailing subsidiary would flow up to the parent.

Most regulators see the merits of a global system buttressed by these sorts of measures, yet many are taking a different path towards a more fragmented one, in which regulators in each country unwind local subsidiaries of failed international banks on their own, relying on the capital they have required banks to keep locally. In Britain and Germany bank supervisors are tightening the screws on the subsidiaries of foreign banks, forcing them to hold more capital and liquid assets that can be quickly sold. In America Daniel Tarullo, a governor of the Federal Reserve, is expected to announce new rules within weeks that will also require the American units of foreign banks to hold much more capital and liquid assets than they do now. The American rule, by making explicit what others are doing quietly, “lets loose the dogs of protectionism, of Balkanisation”, says one senior banker.

At first glance a more compartmentalised banking system does not seem such a terrible idea. Some large banks such as HSBC and Santander already have Balkanised structures, with networks of subsidiaries, each of which has enough capital to stand alone. Many are retail operations in emerging markets where it makes sense to match local loans and deposits. Regulators could do worse than to adopt this model for other retail banks, especially since taxpayers are often exposed to losses through government deposit guarantees.

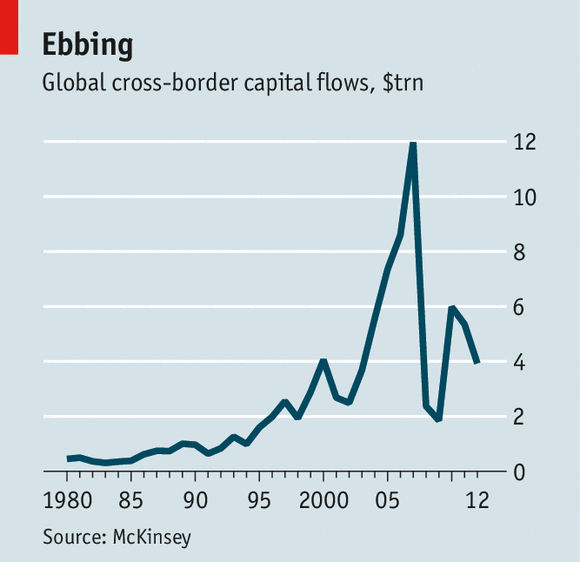

Yet forcing big wholesale and investment banks to run as networks of stand-alone subsidiaries is a different matter entirely. These are global businesses best run on global lines. Balkanising them would hinder capital from moving to where it could be put to the most efficient—and lucrative—use. It would also distort competition by forcing international banks to hold far more capital in aggregate than their domestic counterparts. Cross-border flows of finance have already taken a huge knock since the financial crisis (see chart), driving up the costs of borrowing and reducing investment returns. If this trend continues then global economic growth could be trimmed by almost half a percentage point a year, reckon consultants at McKinsey.

Fragmentation might also make the financial system more fragile by reducing banks’ ability to diversify risk and by preventing them from shifting capital from strong subsidiaries to those in need. This is potentially exacerbated by other regulations, such as Britain’s ring-fence of retail banking and proposals in the rest of Europe to cordon off wholesale banking. The result may be banks sliced not just by geography but also by line of business. “There is genuine strength through diversity,” says Huw van Steenis, an analyst at Morgan Stanley. Most of the banks that failed during the crisis specialised in a particular part of the business, he points out, yet subsequent regulation is encouraging banks to follow their model.

The instinct of regulators to focus mainly on keeping their own banking systems safe is understandable, particularly since they are answerable to local taxpayers. The benefits of financial globalisation are diffuse, whereas the costs of a big bank failing are concentrated. It is not too late, however, to create a global resolution system that is both safe and efficient.