How EPF makes money for dividend payment; CEO reveals EPF’s strategies

November 24, 2013 Leave a comment

Updated: Saturday November 23, 2013 MYT 12:45:20 PM

How EPF makes money for dividend payment

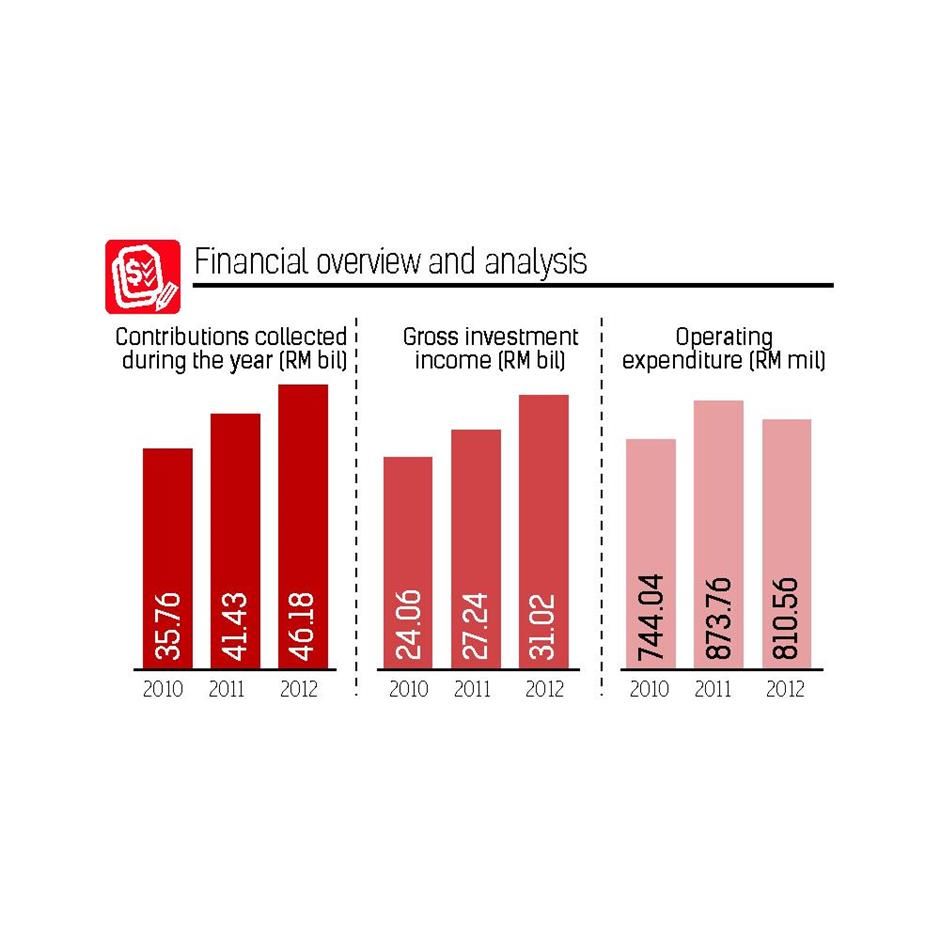

IT’S probably the one dividend rate most Malaysians will scrutinise. The rate will be dissected, debated and then the verdict from the people will be whether it’s satisfactory or poor. That single dividend is what the Employees Provident Fund (EPF) announces yearly. Last year’s 6.15% was the highest in a decade but the challenge that the EPF faces is how to keep that going.The circumstances in generating that kind of return are getting tougher but the transformation in how it invests is helping.

The fund is growing fast – the size of the fund is RM568bil – and the environment of super low interest rates is not helping. Hence, hitting a decade-long high in terms of dividend payments is nonetheless a pleasant achievement for EPF members.

“There are two key goals for the EPF when it comes to financial management. The first is capital preservation.

“Paramount in the way we structure our assets is basically capital preservation. We cannot afford even a low risk in the loss of capital. Because of that, we carry a very high percentage of government debt and high grade corporate securities. When it comes to equities, we only invest in blue-chip companies and the larger companies because of liquidity,” says CEO Datuk Shahril Ridza Ridzuan.

The return of 6.15% for a near zero-risk investment represents a bounty in investment circles. The rate not only bettered EPF’s internal targets of beating the rate of inflation, it also managed to pip the second target it has set for itself, which is to give a return to shareholders that is more than 200 basis points, or 2%, above the rate of inflation over a long-term horizon. Last year’s return was inflation plus 3.8% for a rolling 3-year period.

“Because of that, in the current environment where interest rates are very low because of quantitative easing, the biggest challenge we have today is getting high nominal returns because interest rates everywhere have collapsed.

“Even property yields have fallen as well. Yields have sunk to sub-6% levels in some cases,” says Shahril.

The outlook for this year has been patchy although there are those who are expecting the EPF to keep its streak of better returns over the past four years. The first quarter was slow because of election worries and the EPF is trying to catch up with last year’s performance because of the handicap in returns because of the first-quarter jitters.

“Since the general election is over, we have done quite well but because it’s a low inflation period, we should not have the problem of meeting our inflation targets again,” says Shahril.

“In terms of yield, because we are focused on blue chips and long-term yields, we are still able to meet our targets for this year.”

There will be calls for the EPF to invest in small cap stocks to bump up its return to members, but that piece of risk is something the EPF doesn’t want to digest.

“It doesn’t suit the kind of portfolio building we are trying to do here which is very much focused on long-term, cashflow driven stabilised returns,” says Shahril.

It’s safety first for the EPF as it is responsible for managing and growing retirement savings of most Malaysians. But the job for Shahril and his team is not so easy. Because of comparison against unit trust industry, where in the good years the more heavily skewed equity funds tend to perform well, the EPF will always be benchmarked against its peers.

“If you compare the EPF against a similar balanced fund, I think you will find the EPF, effectively because we have a minimum return guarantee, tends to outperform a lot of these funds. It’s not to say there are no outperformers, there will always be.

“When you compare the EPF against a unit trust, you need to be careful in what you are comparing against. Unit trusts that are 100% equities will have a much higher risk return profile. That means they will outperform the EPF in times when the markets are good but they will significantly underperform the EPF when markets turn.

“But against a 100% equity fund, you will find some of the balanced funds actually outperfrom some 100% equity funds over the long term,” he says.

The returns of a fund depends on the ability of the person managing a fund and the EPF feels it has the the right skillset to manage the retirement money of Malaysians.

“You will find basically that if you benchmark EPF’s investment skillset to a lot of its peer groups, we rank quite favourably. In some areas, we are still learning, and in those cases, we partner with people such as established funds to co-invest or we work with partners and we invest in their funds and learn,” says Shahril.

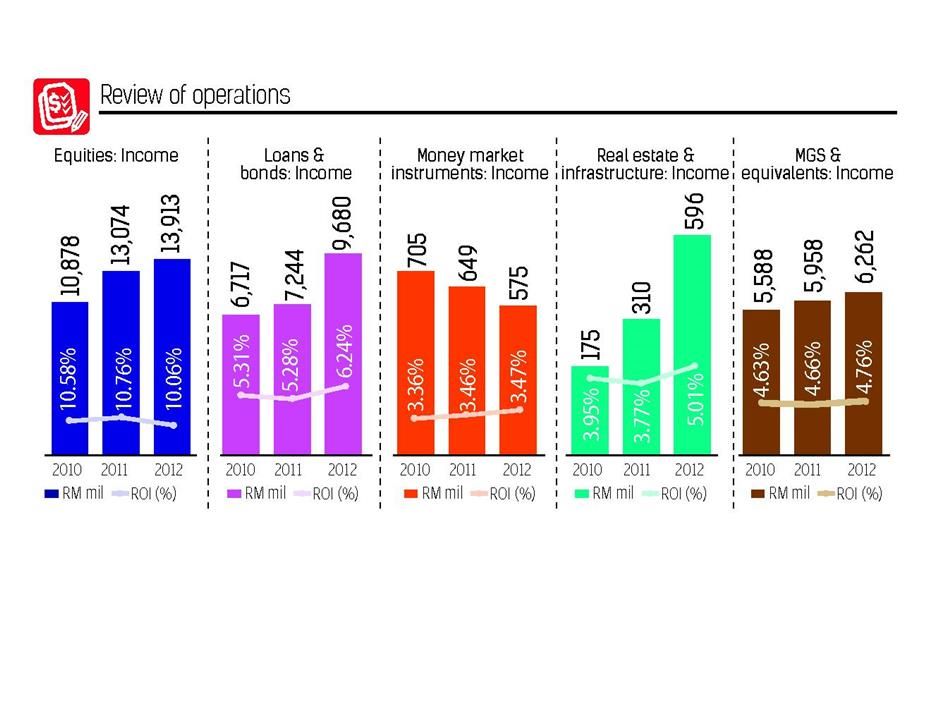

He says that in the global assets it invests in, which now accounts for 20% of EPF’s portfolio, it has managed an average return of 6%. That rate of return satisfies Shahril as the fund is looking for consistent returns over a long period of time rather than volatile returns.

The EPF invests in slightly less than 200 listed companies, of which, 30%, in its own classification, are small and medium caps. Most of the money it invests in equities though reside with big cap stocks.

“We are focused on companies with good cashflows and have a good track record in terms of paying out cash to their shareholders. So we are heavily invested in the banks, plantations – despite the low price of CPO, they are a decent long-term investment because of the nature of the cycles they are in – and we have invested a lot in consumer goods and consumer facing operations.

“We are also large shareholders of the major REITs. We like REITs generally because of their exposure to the property market and they are directly tied into consumer spending as well. Most of them are retail focused,” he says.

EPF’s investments are roughly about 50% in Government debt and other high grade corporate securities, 40% in equities and the rest are in properties and infrastructure, and money market instruments.

It is increasingly investing overseas and its investments abroad now account for 20% of its portfolio. It’s self-imposed limit is 23%. It’s giant size and influence on the markets here means that it needs to invest abroad.

“On some days, we constitute 20% of trading on Bursa (Malaysia) and this is a high concentration risk and we need to diversify. The Government understands that and we stick close to a diversified model and invest in blue-chip companies. I understand the concept that investing overseas is riskier but this depends on what you invest in.

Look at properties we have. It’s leased to blue-chip companies. Similarly, we invest only in the biggest blue-chip companies overseas,” says Shahril.

Investment in property

The EPF’s first foray into the property sector was after the Asian Financial Crisis when it entered into a venture with S P Setia to develop Setia Eco Park. It has paid off handsomely for the EPF and the one key lesson it has learnt is to always partner a blue chip name. “It’s not just with property, and it’s with any industry. In property, our investment in Setia Eco Park has done very well for us. We also have investments with Sunway and YTL, although they are not as visible. We are comfortable with that,” he says.Its exposure into the direct property business is about 3% of its portfolio. Small in percentages but big on publicity.

There was none bigger though than when the EPF decided to get into business with S P Setia again and Sime Darby Bhd to develop the massive Battersea power station in London.

Already comfortable with the property market in the UK as it holds buildings in the country, Shahril says its role is purely as a financial investor.

As it stands, the Battersea development has met with strong buying interest, and that pleases Shahril.

“From the plans we have seen, the second and third phases that are coming up soon will be equally if not more exciting. It’s a good investment for all parties. We are quite comfortable with where the investment is right now,” he says.

That’s not the only big property project the EPF has embarked on. Under unit Kwasa Land, the EPF has bought 2,000 acres in Sungai Buloh where it is planning an integrated development.

Investment in property is a hedge against inflation but it is also a big income earner for the EPF for the next 15 to 20 years. Right now the project is on the cusp of being launched as it is waiting the final nod from the Selangor government.

“It is a way for us to protect against inflation and as we progressively develop the land; we will get income in a few ways. One will be from land sales, and secondly, in joint ventures with developers in the development of the land. Thirdly, for those assets we want to hold, it will be from rental yields. It plays out nicely across the investment curve for us,” says Shahril.

Shahril says the development will be conducted transparently and each parcel sold – ranging from 20 to 100 acres in size – will have strict covenants as what developers can do.

Kwasa Land will replicate KL Sentral in some ways at the former Rubber Research Institute (RRI) land as there will be a 300-acre depot for the MRT system. Two stations will reside on that land and with the KTM Komuter extending its tracks to the Subang airport, Shahril feels connectivity will be a major selling point for the development.

“We have called the pre-qualification in three tiers. The Tier-1s are all your major developers. Tier-2 are the middle sized guys and Tier-3 are bumi developers,” he says, adding that the pricing of land sold will be market driven.

Updated: Saturday November 23, 2013 MYT 12:48:58 PM

CEO reveals EPF’s strategies

Employees Provident Fund (EPF) CEO Datuk Shahril Ridza Ridzuan (pic) spoke to Business editor (features) Jagdev Singh Sidhu recently outlining the retirement fund’s strategies and aspirations. Below are excerpts:

What’s happening at the EPF?

As the people we serve change and if you look at the demographics of Malaysia, half of our members now are below the age of 40. We need to change along with them in terms of what they expect from our service delivery and what the EPF means to them.

Tan Sri Azlan (Zainol) did a great job in transforming the EPF to become an efficient, business-driven organisation it is today. What we are doing is taking that base and bring it a step further.

We are looking at putting a lot of our services online and on mobile devices. The clients we are facing now are young and mobile and they’ll rather not step into our office and branches.

We have been pushing a lot of the electronic services to both employers and employees. We are making it compulsory for all new employers to make their submissions with us electronically. We are going to convert the existing employers to move onto electronic submissions.

We are also going to give them the option to pay electronically. Right now its linked to RHB, but we are working to get the other banks as well.

For us, it makes a difference. When employers submit their forms, we have to manually check for errors. Errors create a huge problem for us because we want to make sure the right amount of money is credited to the right person. With electronic submissions, everything is pre-checked. EPF spends a lot of money fixing errors caused by employers. It’s not fair to members because every ringgit that we save is money earned for our members.

We are also going to expand into electronic withdrawals for our members as well. We have started that with housing in a pilot project. Later on, when we link up with universities, hospitals and banks, when members want to make a withdrawal for medical or education or whatever, they can go to the hospital or university they are registered with and the organisations can pull the data from us on the eligibility of the member. Everything can be done electronically as well and it saves time and money for the members.

The idea is that over the next 5 years we want to get between 60% and 70% of our current processes online.

We manage between 12 and 13 million transactions a year.

A lot of it is investment withdrawals and that’s online already and that saves a lot of time and money.

If we can achieve that goal of 50%-70% in online transactions, we will then retrain our officers to become financial advisors.

That means the EPF branches will move from being process-driven to service centres with financial advisors.

The biggest issue we are faced with and we are working with Bank Negara and other agencies is the lack of financial education among the general population. Bank Negara is working with the Education Ministry to put elements of financial literacy into the new school curriculums. What we intend to do is to provide those financial advisory services in our branches in the next 5 years so that our members can start their financial planning from the time they start work. We can help them to understand how important it is for them to save and they can do pre-retirement planning as well so that when they retire they will know exactly what to do with their money.

By next year, we are going to have a pilot phase in the Klang Valley where we are going to turn two of our branches into these service centres and we will see what’s the demand and what kind of services people are looking for and use that pilot programme to rollout our services nationwide by 2015/16.

When you say half your members are below the age of 40, what kind of problems does that create?

It boils down to financial literacy. What we see basically is like any country, developed or otherwise, there is a high correlation between financial literacy and mathematics, income levels and family backgrounds as well.

What we and people like bank Negara are trying to do is to introduce more elements of financial literacy in the education system as well as in training with the employers as well.

We are looking at big employers to introduce modules of financial literacy for their staff. The whole idea is to get people from an early age to realise the importance of savings, compound savings, yields and growth.

The Gen-Y, and the millennials who are coming into the workforce in the next 10 years, you can see the shift in thinking between consumption versus savings.

The EPF has stressed on the need to manage retirement funds as the average now at the age of 55 is RM158,000. What can be done to improve that?

The amount of money saved at the age of 55 on average by our members is probably insufficient for their retirement plans. We are going to raise from next year the targeted minimum savings to RM196,000 at the age of 55. The way that is calculated is that is pegged against the minimum pension the Government gives to their civil servants which is RM850 a month.

We are looking at RM850 a month for 20 years. That’s the sum we feel people should be working towards as that is a certain base level of income for your retirement.

The kicker question is how do we get to that? That is an issue that is linked to wages itself. With the minimum wage coming in now we expect to see is an upward pressure on wages to move up as the economy becomes more efficient and generate productivity.

Slightly more than 90% of people in formal employment who are contributors to the EPF earn less than RM5,000 a month. Hopefully that percentage will come down in the future as more people earn more than RM5,000 a month. That will definitely help at arriving at the target. RM196,000 is the amount that will provide you with a minimal comfortable retirement. That’s assuming people will not have any other savings but people over their working life withdraw money from us to buy a house and that house will add value as well.

But you have started to tweak how much a person can withdraw for unit trusts?

That is linked to the minimum savings concept. As long as you have savings above the required amount set according to age (please refer to table below) you can withdraw that excess for your investment scheme.

The reason for that is the EPF is basically a balanced fund and is designed to provide a lot of certainty as to the capital you are going to retire with. When you take out the money for unit trusts, you will always draw the risk that should you retire in a year when the market is down and the amount of capital you have at that point in time is going to be affected as well.

The idea is to have a certain minimum safe savings with the EPF. Anything above that is really up to the membership.

Part of financial literacy is for people to recognise what are their goals and what is the amount of risk they are willing to take to achieve those goals.

Are you still doing deals in Malaysia?

We are in the process of acquiring strategic parcels of land which we believe will act as a great inflation hedge and as an income earner for the EPF for the next 15 to 20 years. A classic example is RRI. But we also doing co-investments with other parties but that is more selective. There we are ccareful to look at the deal and to see whether it makes sense for us financially and whether we can manage ther risks of moving into those kind of properties.

We actually own a significant portion of the Giant Hypermarkets in Malaysia which we bought over the physical hypermarkets and those are leased back to Giant. We also own the Sogo shopping centre. The guys who run Sogo are fantastic operators.

The PLUS Expressway?

So far so good. In terms of achiveing the investment thesis we had when we went in. It seems to be achieving that. Obviously there is a bit of a balancing act because when we took over Plus, we were able to restructure the toll.

We should be able to achieve our targeted IRR returns of about 10-plus to 11%, which I think is a fair return for this kind of project. The Malaysian public gets a lower toll burden over the life of the project.

It’s stuff like this and Battersea that is going to paint a nice outlook in terms of returns?

Our investment in Sungai Buloh is RM2bil but our fund size is RM568bil. As a percentage it is small but that is the philosophy of EPF. We have a diversified portfolio. Some of which is RRI where we hope to get better than normal returns because we are taking slightly more risk in terms of development. The rest is stable returns. If we make great returns on RRI, yes it will help the fund on the whole but it won’t move the needle that much.

Apart from Battersea, you have gone into other UK properties and Germany and even Australia. What’s the thinking behind those moves?

We moved into those property markets for a few reasons. The markets we have moved into really have unique characteristics compared with the Malaysian market. For one, we can get very long leases. and they are all triple A clients.

In Malaysia, if you own an office building you can get long leases but the general lease terms in Malaysia tend to be 3+3 years.

There is always an element of uncertainty on your leases but place such as the UK or Australia, because of the way the markets there have developed, you get a lot less risk in your lease structures and the leases themselves are structured in a way where the tenants take care of all the costs in terms of the upkeep of the building. As a landlord, you know for sure with a great certainty what your net returns are going to be.

With property prices in the UK at a high, does it make sense to do deals there?

For us it’s been about risk and return. We started moving into the UK three years ago and we got good deals at that point. Then there were few people looking at the market. Today, there are too many players in the market and we have not done an office deal in the UK for nearly a year now because primarily we cannot find any good deals.

In the UK, in the past one year we are focused on assets other funds are not looking at yet. We have done hospital deals which have turned out very well for us but not an office deal for some time.

We buy out the hospitals and lease them back to the operators themselves.

It is a space no other funds are looking at and we have got some good deals in the space.

How much money have you allocated for property from your funds under management?

The property side of our investments is relatively small. Property as a whole is about 3% or less of the total assets. The thing about property is that it is very visible. When we look at the assets we invest in, we do more trading in one day in the equity markets than the amount of property we will buy in an entire quarter. Because of that, we have been very careful about the property assets we acquire. We think the right size for us in terms of these hard assets will be 5% at this point.