Despite a tarnished record, commodities have not lost their lustre for all

November 30, 2013 Leave a comment

Despite a tarnished record, commodities have not lost their lustre for all

Nov 30th 2013 | From the print edition

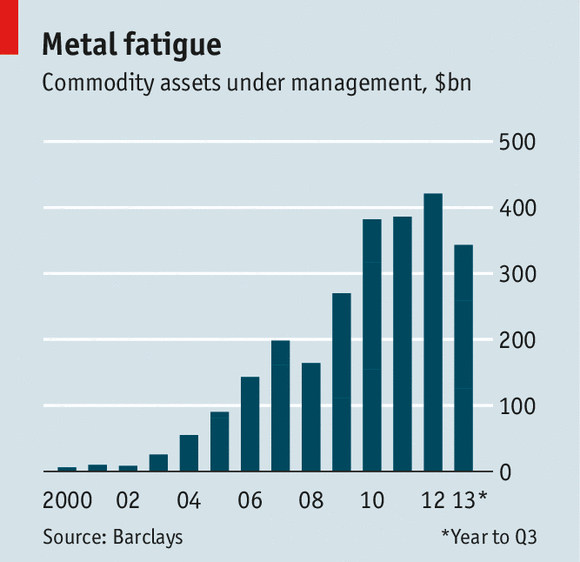

GRAIN silos, oil pipelines and copper smelters are not exactly glamorous. Yet for a glorious couple of years up until mid-2008, commodities were all the rage. China was booming, and supplies of everything from soyabeans to iron ore were failing to keep pace, prompting a giddy leap in prices. Financial engineers minted all manner of products tied to these movements. Not only were commodities on a roll, their patter went; they also provided a crucial hedge for any diversified portfolio, since they did not move in tandem with other assets.This spiel convinced all sorts of big investors to pile in. Pension funds, endowments, sovereign-wealth funds and the like scrambled to grab a piece of the commodities boom, only to see prices wobble along with the world economy, and then slip as China’s growth slowed. Yet overall investment in commodities has barely fallen, even though the sales pitch that drummed it up has been largely disproved.

According to Barclays bank, the flood of investment in commodities reversed only slightly this year (see chart). If gold, which behaves more like a currency, is left out of the picture, the sum of commodity-related assets under management has hovered at a little under $220 billion since 2011.

Falling commodity prices, thanks both to increased supply and to slower economic growth in emerging markets, have called into question the long-term return that the burgeoning asset class was presumed to offer. But that is not the only reason that investors have gone lukewarm on commodities. The role of raw materials as a hedge against rising prices remains untested and unimportant while inflation stays stubbornly low.

The supposed power of commodities to diversify portfolios has also failed to match the billing. In the decades leading up to the financial crisis there had been no consistent correlation between returns from commodities and other investments. But the crisis hit all types of asset. Commodity indices and the S&P 500 moved more or less in sync. Commodities, in other words, were no hedge against economic cataclysm. It is little comfort that the link seems since to have been broken again, as equities have prospered while commodities have not. Indeed, historically, commodities have yielded little return except during the oil crises of the 1970s and the heady years before prices peaked in 2008.

These disappointments have provoked retreats from some prominent advocates of commodities. A few big commodity-focused hedge funds have closed and several investment banks are getting out of the commodities business. CalPERS, a giant pension fund for state employees in California, which helped to cement commodities’ status as a mainstream asset class with a big investment in 2007, cut its exposure late last year from 1.4% of its total assets to a niggardly 0.5%. But it says this reversal may only be temporary, and other investors continue to pile in.

Indeed, some boosters argue that commodities’ time will come again. Nick Brooks of ETF Securities, a commodities-investment firm, senses tentative interest and reckons a small recent inflow of investors’ cash might herald better times.

Kevin Norrish of Barclays also sees reason for optimism. Both reckon that investors in commodities are becoming cannier. Although most still bet on simple price rises, the more sophisticated are exploring subtler strategies to eke out returns, tied to relative movements in price between different commodities, for example. As a fairly new and little-studied asset class, more research might boost returns.

Of course, across-the-board price rises would provide the biggest boost. Mr Norrish says that commodities tend to perform better in the later stages of an economic recovery. That still looks some way off. Worse, China is unlikely ever to return to the tearing growth that sent commodity prices skyward a decade ago. But miners are cutting investment and oil production growth is sluggish. So there is a chance that prices will rise again and commodities will swing back into fashion.