Picking holes in Piketty: The latest controversy around Thomas Piketty’s blockbuster book concerns its statistics

June 2, 2014 Leave a comment

Picking holes in Piketty: The latest controversy around Thomas Piketty’s blockbuster book concerns its statistics

May 31st 2014 | From the print edition

FEW economics books have been as popular or as controversial as “Capital in the Twenty-First Century”. The blockbuster analysis of wealth and income distribution has been a publishing sensation, turning its French author, Thomas Piketty, into a household name. The book’s thesis, that wealth concentrates because the returns to capital are consistently higher than economic growth, has spawned furious debate. Mr Piketty’s preferred remedy (a progressive wealth tax) even more so. But amid the argument most commentators have agreed on one thing: “Capital” is an impressive piece of scholarship.

In recent days that assessment has come into question. A scathing analysis by Chris Giles, economics editor of the Financial Times, claims Mr Piketty’s statistics on wealth distribution are undermined by a series of problems. Some numbers, he says, “appear simply to be constructed out of thin air”. Once apparent errors are corrected, some of Mr Piketty’s central findings—for instance, that wealth inequality has begun to rise over the past 30 years—no longer seem to hold. Thus, Mr Giles claims: “The conclusions of ‘Capital in the Twenty-First Century’ do not appear to be backed by the book’s own sources.”

These are bold words. And, if true, they would be a damning indictment of the book as well as of Mr Piketty’s professional standards. Assessing whether they are justified means answering three main questions. First, what statistics are in doubt? Second, are the discrepancies within the bounds of reasonable professional judgment? And third, do the errors, if that is what they are, undermine the book’s conclusions? The evidence so far suggests that, though Mr Piketty may have made mistakes and been sloppy in places, his broad analysis still holds.

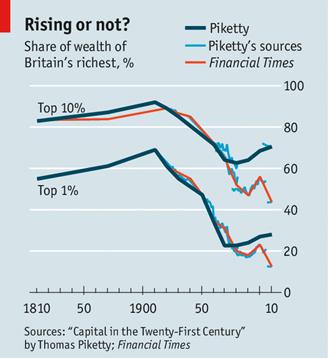

Mr Giles’s focus is on wealth distribution, where the book provides numbers for Britain, America, France and Sweden. His interest was piqued by a discrepancy between Mr Piketty’s numbers on the share of wealth held by Britain’s richest 10% (over 70%) and the latest figures from the government statistical agency (44%). This gap prompted Mr Giles to pore over Mr Piketty’s spreadsheets, which, to the economist’s credit, are all posted online. Several oddities surfaced, such as discrepancies between numbers in the source material Mr Piketty cites and those that appear in his spreadsheets; a large number of unexplained adjustments to the raw data (often in the form of a constant written into the Excel spreadsheet cell); inconsistency in how underlying source data were combined; and the frequent interpolation of data, without explanation, when underlying sources were missing. For instance, none of the sources Mr Piketty used had data for the top 10% wealth share in America between 1910 and 1950. So he assumed their wealth share was consistently that of the top 1% plus 36 percentage points. All told, Mr Giles finds “problems” in 114 of 142 data points in Mr Piketty’s wealth inequality tables.

These findings led Mr Giles to conclude that Mr Piketty’s estimate of wealth inequality are “undercut”. Yet adjustments and interpolations are always necessary when disparate data sets are combined. The question is whether Mr Piketty had a reasonable basis for making the judgments he did. His lack of explanation in places makes that hard to assess. As The Economist went to press Mr Piketty was preparing an update to the technical appendix to further explain his data and calculations, and take issue with the Financial Times’ concerns. Whether he made reasonable choices will be the issue. Economists who disagree with Mr Piketty but have worked with his data have defended his empirical record.

More important is whether the errors—if they are errors—undermine his thesis. To find out, Mr Giles adjusted the wealth-distribution series to correct the discrepancies he found. In the case of France and Sweden the basic trend was unchanged. In America’s case, some of the underlying source data show a more gradual recent rise in inequality than Mr Piketty’s estimate. However, a new, highly regarded study published after “Capital” was printed (written by frequent co-authors of Mr Piketty’s but using different methodology) also finds a steep rise.

The biggest question-mark over Mr Piketty’s data concerns Britain, where his findings that the share of wealth going to the richest is rising seems less clear in the underlying source data he cites and not at all evident in Mr Giles’s adjusted figures, which include the latest government statistics (see chart). The differences are troubling. One explanation is that the government’s new figures are based on surveys of self-reported wealth which tend to understate wealth concentration among the most affluent, while Mr Piketty prefers tax statistics. The picture is clearly murky, but Mr Piketty’s numbers are not self-evidently worse. What is odd, as Mr Giles points out, is that Mr Piketty takes an unweighted average of wealth distribution in Sweden, France and Britain and describes it as “Europe”. Population-weighted would be better. But even then, it’s a stretch to call these three countries “Europe”.

Nitpiketty or a pickle?

All told, Mr Piketty is guilty of sloppiness (certainly in his notation), and perhaps of some errors. But there is little evidence, so far, to support the serious charge of cherry-picking statistics. Nor have his findings that wealth concentration is, once again, rising been fatally undermined.

Nonetheless, Mr Giles’s critique is enormously useful. By taking a tooth-comb to the wealth-distribution numbers, he has provided a powerful reminder of the limitations of such historical data series. Mr Piketty’s conclusions are drawn from huge numbers of sketchy figures (many of which have not yet been subjected to such a review). He has pulled them together in what remains an impressive piece of scholarship. But just as the statistics have their limits, so does the certainty of the trends Mr Piketty identifies. The logic of “Capital in the Twenty-First Century” is not an iron law.