A Study Being Passed Around Silicon Valley Shows That Raising Tons Of Money Can Hurt Startups

June 4, 2014 Leave a comment

A Study Being Passed Around Silicon Valley Shows That Raising Tons Of Money Can Hurt Startups

ALYSON SHONTELL TECH MAY. 31, 2014, 9:49 PM

When startups raise large rounds of financing from investors, it’s often praised in the press. And in Silicon Valley, founders are often encouraged to raise as much money as possible. But a new study shows that most startups shouldn’t strive to raise gobs of cash, and they can actually exit for more money if they take less funding.

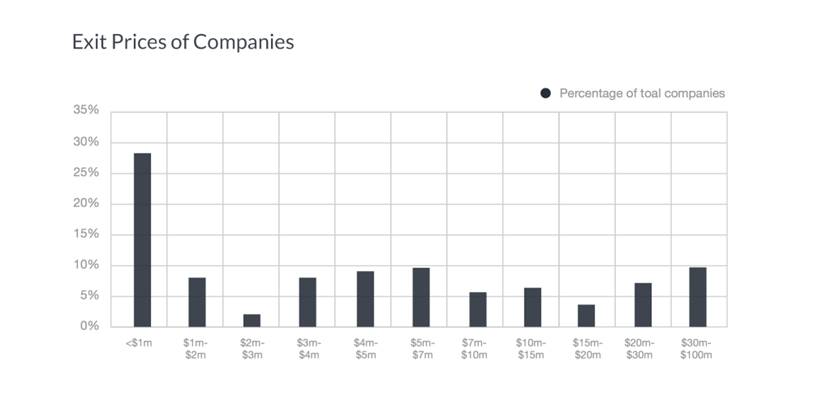

Exitround, a startup that matches early stage companies with potential acquirers,analyzed the sales of 200 startups. It worked with startup accelerator programs Y Combinator, Techstars and SoftTech VC to compile the data and only looked at companies with sale prices under $100 million. Exitround says 88% of all startups are sold for less than that price. The study has been

The study found that startups with the most lucrative exits raised either $2-3 million or $5-10 million. They also tend to be about four years old.

From the study:

In Exitround’s analysis, companies that raised $5 million to $10 million actually generated larger average exits than those that raised $10 million to $50 million. And those companies that raised $3 million to $5 million had a lower average exit price than those that raised $2 million to $3 million.

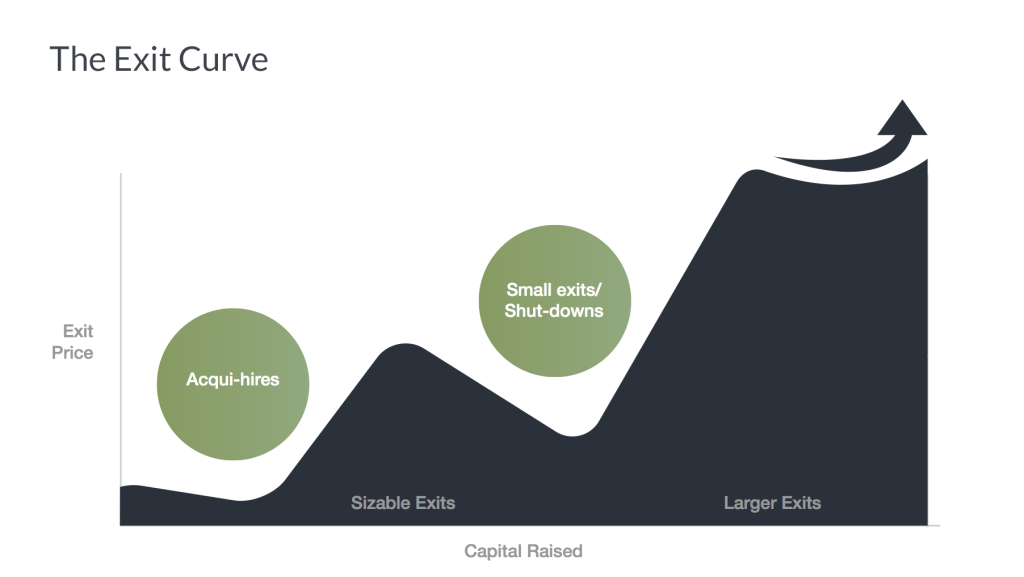

Here’s a chart that supports the data.

The Exit Curve: Exitround’s Report On Tech M&A

Exitround News, Market Analysis

By Tomio Geron on May 30, 2014

inShare54

Raising as much capital as possible is often seen as a badge of honor in Silicon Valley. And there are many great reasons for startups to raise as much capital as possible. But raising more capital may not always be the best option. Exitround’s analysis of proprietary exit data has found that there are good reasons to remain cautious.

There’s a sweet spot for how much capital to raise for startups that want to get the most money out of their sale. Exitround determined these particular exit ranges based on data we analyzed covering more than 200 companies acquired since 2006 for less than $100 million. The best exits from a return-on-capital perspective form a pattern, which we call the Exit Curve. The best average exits tend to cluster around companies with total capital raises of between $2 million to $3 million and between $5 million to $10 million. But exit prices drop after companies raise more than $3 million and $10 million, respectively.

The information in the report will be of particular interest to entrepreneurs and investors seeking to understand the trajectories of startups and what possible outcomes are for their companies–particularly since 88% of tech M&A deals happen below $100 million. Determining potential outcomes is a useful baseline to have in mind as entrepreneurs and investors think about how much to invest or raise, and at what valuations. Knowing the market is also important when entrepreneurs and investors go through an acquisition process.

Here are some other key findings from the Exitround report:

– Raising more capital does not necessarily result in a larger exit price. Exitround’s analysis of proprietary exit data has found that exit prices do not always get larger as companies raise more capital. They sometimes go down.

– Companies that generate substantial exits are usually at least four years old. Companies below four years old on average did not show a substantial variation in price, but those more than four years old increased substantially in price. In other words, companies are not built overnight.

– Exit prices varied among companies in different sectors. Some sectors, such as cloud and mobile showed the best return on invested capital.

David Cohen founder & CEO of TechStars, a contributor to the study, said, “I was excited to participate and contribute data to Exitround’s report because for the first time we’ll have a broad-scale industry look into the long tail of tech M&A activity, which will help me make more informed decisions as an investor, and generally contribute to increased transparency within our industry.”

Seed Investing

The emergence of the seed investing has become a key part of the startup and venture investing landscape. The data in Exitround’s report shows that companies that have raised relatively small amounts of capital can generate substantial returns for those investing at the seed stage.

Michael Kim, founder and managing partner of fund of funds Cendana Capital, which invests in seed funds and is a contributor to the Exit Report, said, “The findings help support our thesis—with real data—that seed VC funds have potentially higher alpha with lower beta (risk) because meaningful returns can be generated by capital efficient start ups early in their life.”

Other topics covered in the report:

The Data Behind The New Seed/Venture Investing Landscape

What Size Exits Have The Best Returns?

Which Size Exits Have The Best Multiples?

How Long Does It Take to Build a Successful Startup?

Which Generates Better Return Multiples: Consumer or Enterprise?

How Does Team Size Affect Price? (or vice versa)

Who Pays More: Public Or Private Buyers

How Are Investors Paid?

How Much Of A Deal Is Held Back For Earn-out/Retention?

Which Sectors Have The Best Outcomes?

Methodology

Information on tech M&A is difficult to find, particularly for exits below $100 million. For founders this can make anacquisition process difficult, particularly for those who have not gone through it before or who do not have strong advisors to help them.

Typically, most M&A reports analyze already-available public data. The Exitround Exit Report is different because it is based on Exitround’s data, which is previously undisclosed data, and which we are presenting in an aggregate anonymized form.

Support in obtaining anonymous data was provided by top incubators and investors, including: Bowery Capital,Cendana Capital, IA Ventures, SoftTech VC, Techstars, Transmedia Capital, Xenon Ventures, Y Combinator and others. For their participation, these partners receive an in- depth detailed analysis of our proprietary data. To participate in future studies, please contact Exitround at exitround.com/data.

To get a copy of the report, click here: exitround.com/data.