China Sees Citic Listing as Model for State-Firm Overhauls; Skeptics Cite Government’s Continued Control, Even After Hong Kong Listing

June 4, 2014 Leave a comment

China Sees Citic Listing as Model for State-Firm Overhauls

Skeptics Cite Government’s Continued Control, Even After Hong Kong Listing

SHEN HONG and YVONNE LEE

June 1, 2014 3:25 p.m. ET

China is poised this week to complete plans for one of the world’s biggest mergers of the year, a $37 billion deal that could be a blueprint for overhauling massive, inefficient state-owned enterprises.

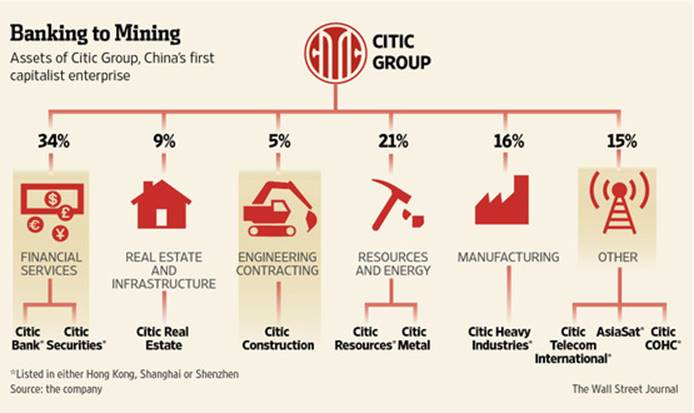

Beijing is using Citic Group, a conglomerate created under Deng Xiaoping as China’s first capitalist enterprise, to change the way the country’s biggest state-owned companies, known as SOEs, are controlled by investors. The merger will essentially list Citic Group’s assets in Hong Kong, where they will be subject to tougher rules and disclosure requirements than they face in mainland China.

“Citic’s original positioning was a Hong Kong-based platform for red capital,” said Li Xiaoyang, an assistant professor of economics and finance in Beijing at Cheung Kong Graduate School of Business, referring to investment arms of the Communist regime in the early phase of China’s economic reforms. “Now the authorities want to use the upcoming Hong Kong listing for it to become a role model again in the next wave of SOE reforms.”

But skeptics say this type of deal, orchestrated by Beijing, will do little to change the way SOEs operate because they will still be answerable to the Chinese government rather than outside shareholders. China’s wide swath of SOEs dominate and often monopolize the country’s industries, ranging from financial services to energy and telecommunications. They enjoy cheap credit from the state and easy access to the country’s capital markets. However, many of these companies are plagued by inefficiency and bureaucracy, while the often-disadvantaged private firms tend to be much more productive and generate the vast majority of new jobs in the country.

The Citic Group transaction itself and the end result highlight how far China needs to go to overhaul its state-owned enterprises.

Rather than holding an initial public offering, Citic Group is having its Hong Kong-listed unit, Citic Pacific Ltd. 0267.HK +0.59% , buy the assets of the parent company for $37 billion. A vote by shareholders, set for Tuesday, isn’t an issue because both companies are controlled by the Chinese government.

To pay for the deal, Citic Pacific will issue around $29 billion in shares that will be bought by its parent company. It will also issue $8 billion in shares that will be mostly bought by Chinese state firms like China’s National Social Security Fund. It has already signed agreements for 15 investors, including the pension fund and Singapore state investment firm Temasek Holdings Pte. Ltd., to buy $5.1 billion in shares.

After the transaction, Citic Pacific, which is now 58%-owned by the Chinese government, will be almost five times as big in terms of market value, but the government’s stake will be 82%.

Advocates of the deal say that by putting nearly all of Citic Group’s assets in a publicly traded company in Hong Kong, it will be forced to adhere to international standards. They expect other state-owned enterprises to follow, potentially giving investors a bigger say in how the SOEs are run.

But Beijing shows no signs of giving up control. The transaction required a waiver from regulators because the government’s stake is so big that less than the required 25% of the shares will be held by the public.

“Unless shareholders in Hong Kong have a true say in the running of the company and in business decisions, just listing the company doesn’t change the management in itself,” said Julian Evans-Pritchard, an economist at Capital Economics. “All these SOE reforms are welcome, but the main issue remains that in many cases the state is reluctant to loosen its grip on the firms.”

When Citic Group in April announced the plan to get bought out by Citic Pacific, Chang Zhenming, chairman of Citic Group and Citic Pacific, said, “Citic has always been right at the heart of the process of reform and development in China and this landmark transaction marks the next stage of the group’s transformation.”

The choice of Citic Group is considered symbolic. It was set up in 1979 by Rong Yiren, a legendary former textile tycoon, who was asked by Deng to “do some actual work and play a role” in Beijing’s nascent economic reform efforts. In 1990, Citic Group listed some of its assets in Hong Kong under the Citic Pacific name, making it one of the city’s first so-called red chips, or mainland-controlled companies listed in Hong Kong through offshore vehicles.

Citic Pacific owns real-estate assets and resources operations such as Australian iron-ore mines, among other holdings. The parent company’s empire ranges from an array of financial-services businesses like banking and insurance, to the country’s top offshore oil helicopter-service operator and even an underachieving football club.

Once the deal is complete in August, the new Citic Pacific, to be called Citic Ltd., will be the first state-owned company with virtually all its assets listed outside mainland China. That contrasts with a long-standing Chinese practice of cherry-picking the strong assets of a state firm to include when taking it public outside China.

“Most state-owned Chinese companies keep some of the assets on their parent level and just list part of their assets,” said David Wu, head of China corporate finance at ING Bank. “This creates a lot of complications, internal competitions and connected transactions between the listed company and the parent company.”

The performance of China’s state-owned enterprises has been weak. Between 2006 and 2013, annual returns on assets among domestically listed Chinese state-run enterprises averaged 2.29%, compared with 5.83% for listed privately run firms, according to data from WIND Info.

Citic Pacific struggled with some bad business decisions during its time as a publicly traded company in Hong Kong. In 2008, the company, then run by Mr. Rong’s son Larry Yung, revealed that a bad bet on the Australian dollar involving derivatives would cost it as much as US$2 billion. The company didn’t disclose the loss for six weeks after it was discovered, and was ultimately bailed out by its parent after being forced to sell stakes in companies including Cathay Pacific Airways Ltd. 0293.HK -1.67%