Chinese exporters have a long record of using fake trade receipts to bring US dollars onshore, swap them into local currency and benefit from the higher interest rates and appreciation. That distorts China’s economic data

June 8, 2014 Leave a comment

June 2, 2014 7:50 am

Renminbi bulls seize on hopes for economy

By Josh Noble in Hong Kong

Remember when currency policy, rather than maritime disputes, used to top the agenda for US-China relations?

Washington long complained that Beijing kept its currency artificially weak, helping it win manufacturing business and amass roughly $4tn in foreign exchange reserves.

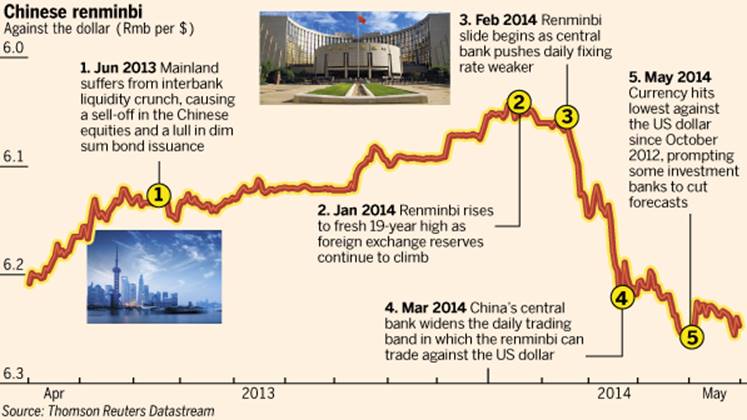

For a while, appreciation proved an effective antidote – a stronger renminbi meant a quieter US Treasury. Between the summer of 2010 and January this year, the renminbi had risen almost 12 per cent against the dollar, to reach its highest level in almost two decades.

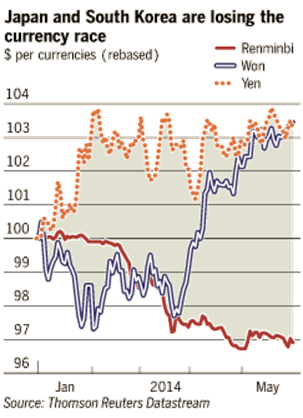

But now exchange rates are creeping back on to the list of talking points, with the US increasingly concerned that China is back to old habits. The renminbi has been the worst performing currency in Asia this year, down more than 3 per cent against the US dollar. Last week it hit Rmb6.26, its lowest since late 2012.

Most analysts believe that the weakness has been directed by China’s central bank, which has used the fixed rate around which the renminbi can trade to nudge the currency down.

In March, Chinese authorities widened the daily trading band to 2 per cent above or below the daily fix. Taken together, these two policies have both guided the currency lower and given it the freedom to fall faster.

The prevailing theory goes that the People’s Bank of China is using a weaker currency to ward off “hot money” inflows from speculators. Chinese exporters have a long record of using fake trade receipts to bring US dollars onshore, swap them into local currency and benefit from the higher interest rates and appreciation. That distorts China’s economic data, and fuels further currency gains.

The battle to ward off speculation has lasted longer than originally expected – many predicted a fall of just a few weeks when it began four months ago. Worsening sentiment towards investing in China – where the property market is showing signs of stress – may have contributed.

But declining intervention by the central bank points to waning upward pressure on the currency. According to calculations from Barclays, China experienced more than $8bn in capital outflows in April, following a six-month period where about $140bn came in the other direction. Exporters, it seems, may finally be getting the message.

“We should from now on see the currency appreciate, given that the job seems to have been completed,” says Hamish Pepper, FX strategist at Barclays, who believes recent outflows may allow the PBoC to “ease off” from pushing the currency down further.

However, there is increasing debate within the market over whether the managed drop is instead being used to prop up a stumbling export sector. If so, the lower renminbi could yet endure, especially if accompanied by more capital leaving China.

Some investment banks have chosen to trim their guidance. JPMorgan recently cut its forecast for the renminbi to 6.15 against the dollar by the end of this year, and 6.1 by the end of 2015.

That equates to just 2.5 per cent of appreciation over the next year-and-a-half, and with a bumpier ride along the way than during previous bouts of currency strength. If correct, the 19-year record high hit back in January could prove the zenith until at least 2016.

But as the gloominess about the renminbi becomes more entrenched, the outlook for China’s economy seems to be brightening. Credit Suisse economists recently hailed a “turning point” in growth, with their in-house leading indicator showing a distinct improvement in activity.

“The pick-up in this leading indicator is tentative and from a low level, but we believe that the worst in terms of the economy losing momentum is perhaps behind us,” they said in a research note.

Container port volumes, electricity consumption and auto sales figures all suggest that the slowdown has been arrested. Data released on Sunday showed China’s official purchasing managers’ index rose from 50.4 in April to 50.8 in May, a five-month high.

Further support from policy makers, perhaps in the form of cuts to bank reserve requirements, could help embed that recovery and balance the risks from a weak property market. The Hang Seng China Enterprises index – mainland companies traded in Hong Kong – rose 4 per cent in May, a small indication of improving sentiment.

Building evidence of an economic turnround could give renminbi bears pause for thought. Dariusz Kowalczyk, strategist at Crédit Agricole CIB, said that now is the time to bet on a rebound. “Technical negatives in the renminbi have played themselves out already while fundamentals are turning round,” he wrote in a recent report.