World’s smallest stock markets battle growing pains

June 8, 2014 Leave a comment

June 2, 2014 4:38 pm

World’s smallest stock markets battle growing pains

By Elaine Moore

Every day, the flip-flop wearing moped drivers who make up the majority of Cambodia’s street traffic can look up at the tallest tower in Phnom Penh and check the performance of their country’s stock market.

It does not take long. Three years after the exchange opened the electronic billboard outside still shows the price, value and trading volume of a single listed company: the Phnom Penh Water Supply Authority.

The received wisdom is that a frontier market planning to grow needs to open a stock market in order to attract foreign capital. Almost as soon as Myanmar began to make the transition away from military rule in 2011 the country announced that it was working with Japan to create a securities exchange.

Investors point to past success stories such as Vietnam, which established its stock market in 2000 and now lists more than 800 companies. But turning a new stock exchange into a busy exchange is not straightforward.

“There is a belief that it is worth opening a stock market because it attracts foreign capital,” says Sam Vecht, head of BlackRock’s emerging markets team. “But there are some that just don’t have the scope. Bahrain, for instance, has never attracted much interest and barely trades.”

South Korea’s stock exchange, the KRX, helped to set up the Cambodia Securities Exchange, six months after opening one in Laos, and admits progress has been slow.

“The Cambodian government first approached Korea in 2006 to help establish a stock market,” says Steve Dae Chun Kim, head of emerging market business at the Korean Stock Exchange and part of the team that set up Cambodia’s exchange.

“We designed it, educated the people, provided the software. But these things take time. Also there are cultural differences. Koreans work at night-time. In Cambodia they go home at 5pm.”

If there was a prize for the world’s smallest stock market, Cambodia would be in pole position but it has competition.

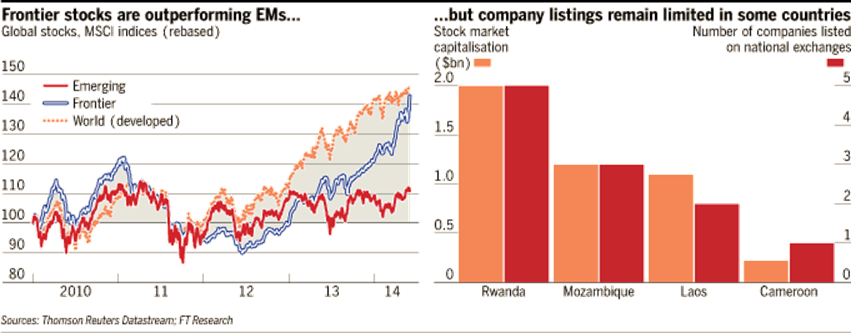

Cameroon’s Douala stock exchange, which has its own Facebook page, has two companies, while Mozambique’s exchange, the Bolsa de Valores Moçambique, has three. Three years after it established its stock market, Laos also has just three companies listed: Banque Pour Le Commerce Extereiur Lao, Lao World Public Company and power company EDL-Generation.

The Seychelles, which has a population of just 87,000 across its islands, opened its stock exchange in late 2012. So far Trop-X, which is owned by South Africa’s Quote Africa Group, has three companies listed, only two of which are traded: builders merchant Bodco and insurance company SACOS.

Which companies list on a new exchange depends on a country’s background. In ex-communist countries, for example, the companies tend to be state-owned.

“A stock market should represent the scope of a country’s economy,” says Mr Vecht. “But in some countries that will never happen because the scale is so small that the listings are driven by politics.”

Politics can also act as the driver for an exchange being set up.

“Countries know that creating a stock market will generate headlines and will make the country more visible to international investors,” says Sam Mahtani, director of emerging market equities at F&C Investments. “So in the evolution of frontier market economies opening a stock market is a critical point.”

Demand for new companies across the world has been strong in recent years as appetite for exotic investments grows.

Frontier markets have performed well this year, boosted by improvements in domestic economic data and growing international trade. The MSCI Frontier Markets Index is up 17 per cent year to date.

Individual company listings on new exchanges also have a good record of strong initial investor demand. On its first day of trading, the Phnom Penh Water Supply Authority closed up 48 per cent, and the Seychelles’ first listing closed 13 per cent above its opening price.

But finding a second, third or fourth IPO is tricky. Last week the Cambodian arm of a Taiwanese garment maker, Grand Twins International, delayed its plans to become the country’s second listed company, citing regulation problems.

“Listing takes time,” says Ali Khalpey, head of equities at boutique investment firm Exotix. “You are starting from the beginning so that means that you have to set up the infrastructure, create an equity culture and there is a long due diligence process for the companies planning to list.”

South Korea insists that the time and cost is worthwhile. The country’s exchange, which owns a minority share in Cambodia and Laos stock exchanges, is reported to be in talks with countries in Africa and South America to export its trading system.

“Some people ask questions about whether these countries deserve stock markets,” says Mr Kim. “But when Korea launched its market in 1956 our GDP per capita was just $80. The question is not what stage the countries are at but what plans the governments have for the future.”