Volatility Traders Have More to Fear than Fear Itself

June 13, 2014 Leave a comment

Volatility Traders Have More to Fear than Fear Itself

SPENCER JAKAB

June 10, 2014 4:45 p.m. ET

The latest big worry to hit markets is an unusual one: calm. With stock prices high and various gauges of risk low, investors appear to have thrown caution to the wind.

That isn’t entirely true, though. Exchange-traded notes that profit handsomely from market-shaking events have boomed since the financial crisis. But they have two big shortcomings: They may not work as designed in another financial crisis since their value depends on the bank backing them. And due to the way the products work, anyone holding these for the long term will inevitably see their value erode.

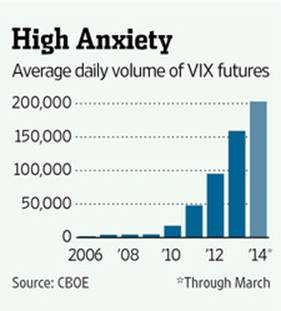

Futures contracts linked to market volatility were pioneered by the Chicago Board Options Exchange CBOE -2.20% in 2004, offering a way for professional investors to hedge the risk of stock-market swings. The more accessible notes that opened bets on the CBOE’s Volatility Index, or VIX, only began after the 2008 crisis.

They have grown rapidly, with assets under management rising to nearly $3 billion. Their impact is wide-reaching; they form the lion’s share of turnover in a derivatives market capable of hedging $200 billion in stock portfolios, according to Jeff Kilburg, chief executive of futures broker KKM Financial.

One popular product with the catchy name of the VelocityShares Daily 2x VIX Short-Term ETN is designed to produce double the daily return of short-term VIX futures. Had it been around in September 2008, it would have surged by over 1,000% during the next three months. Or it could have gone to zero. That is because the notes are dependent on the firm sponsoring them. The VIX is just a calculation based on the prices of options for the S&P 500 index. So unlike oil futures, contracts tracking the VIX aren’t backed by anything besides the promise of a bank to pay the return on the index.

Yet those who buy these notes are forgetting history. In a true meltdown, so-called counterparty risk can flare. After all, investors who owned ETNs backed by Lehman Brothers in 2008 had to get in line with the collapsed bank’s other senior unsecured creditors. An ETN also could suffer if investors simply grow fearful about a firm’s creditworthiness.

The other structural issue facing ETNs is that, when markets trudge higher, the products suffer the investing equivalent of death by a thousand cuts. Daily changes in the products’ prices don’t perfectly mimic an underlying index. Over a short period this doesn’t matter much, but it compounds over time. Add in leverage and this amplifies the mismatch, even if the VIX fluctuates only slightly.

Worse, VIX futures prices typically trade at a slight premium to the actual index and fall in price as they near settlement. Those headwinds take a toll for anyone who buys and holds. Take the VelocityShares Daily 2x VIX Short Term ETN. A $10,000 investment at its inception in 2010 would be worth around $3.00 today. While some investors don’t grasp this erosion, sophisticated ones do. That presents tactical trading opportunities, although these carry risks in such low-volatility times.

The past few years have been a bonanza for those who sold short volatility-linked ETNs, betting on them losing ground. Plus, there are products providing inverse exposure to moves in VIX futures, rising when they drop and vice versa. This is effectively the same as selling the index short. Those who bought the VelocityShares Inverse VIX Short-Term ETN have made 91% over the past year.

This strategy isn’t for the fainthearted either: A financial or geopolitical crisis can send the VIX surging. The Inverse VIX ETN lost 35% in three days in August 2011 after the U.S. credit rating was cut.

Proponents of VIX futures and their associated products tout their tendency to zig when markets zag. A potential use might be purchasing a volatility ETN hours before a critical Federal Reserve announcement. Fans cite a deep, liquid futures market as a solid underpinning for the products. Over 200,000 contracts have traded daily this year on the CBOE, compared with less than 5,000 back in 2009.

Nevertheless, hiccups occur. The VelocityShares Daily 2x VIX ETN, sponsored byCredit Suisse, CSGN.VX +0.44% temporarily suspended creation of new units in March 2012. Other brokers surmise this reflected Credit Suisse’s difficulty hedging its growing market exposure. Since supply suddenly was limited, those selling the ETN short engaged in panic buying. The price surged by nearly 90% in a few days, then crashed as the bank reversed course.

Now that volatility has emerged not only as a concept but an investment in its own right, there probably is no putting the genie back in the bottle. And while portfolio managers largely welcome the products, the droves of speculators drawn to VIX notes may be in for a wilder ride than they realize.

Above all, investors who use them as a form of insurance could find the product doesn’t behave as expected when the storm really hits. Drawing comfort from today’s ample liquidity, they should recall the adage: it is always there, except when you really need it.