Hedge fund chiefs and former bankers enter the shadows

June 23, 2014 Leave a comment

June 19, 2014 5:21 pm

Hedge fund chiefs and former bankers enter the shadows

By FT reporters

In the six years since the financial crisis, the financial services world has seen all kinds of new institutions take over lending deals and clients that were once the domain of traditional banks. There has also been a parallel transformation: the mutation of bankers into shadow bankers, writes Patrick Jenkins in London.

The bosses of many shadow banks – hedge funds, private equity and debt funds, tax-efficient “business development companies” and peer-to-peer lenders – seem increasingly to have been drawn from the upper ranks of the big traditional lenders.

Many bankers have become disillusioned with the old ways of doing things, demotivated by weak market conditions and shrinking ambitions, and frustrated by a mountain of new regulations. The freer world of shadow banking offers welcome liberation. It also presents an opportunity for those with experience in banking because they know where the business opportunities – and the regulatory loopholes – lie.

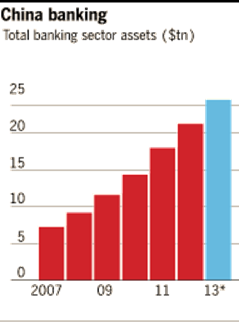

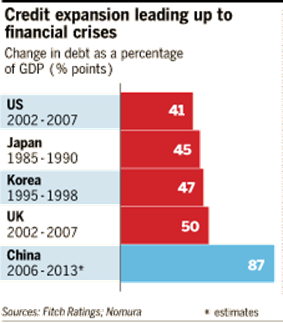

But if the migration of bankers into shadow banking is a clear pattern in western markets, elsewhere it is harder to make such generalisations. Anecdotal evidence in China, one of the biggest – and most concerning – shadow banking markets, suggests a far more eclectic heritage at the helm of big non-bank lenders, a development that adds to the potential risks.

Financial Times reporters around the world meet and profile a sample of the shadow banks and their bosses:

BlueMountain Capital: ‘We try to maximise the net we cast’

At certain times of day, BlueMountain Capital is literally in the shadow of JPMorgan Chase, write Tom Braithwaite and Michael Mackenzie in New York.

Its New York headquarters on Park Avenue stand next to the US banking giant’s skyscraper. But, as befits a player in the business of shadow banking, seeking to capitalise on the dislocation of traditional sources of finance, the alternative asset manager seems happy to keep a low profile.

Unlike the banks it is seeking to usurp, BlueMountain does not operate a single branch anywhere in the country – and nor does it send teams of loan officers across the US. But it has become a provider of capital to companies, either directly or through other channels.

“Sometimes we might engage directly with an issuer because we have a relationship, or because our reputation earns us a call,” says Andrew Feldstein, chief executive, pictured, who used to work for the bank next door. “We also work with intermediaries like money centre banks, regional banks, or a boutique investment bank in one of many US cities. Sometimes it’s an accounting firm. We try to maximise the net that we cast, whether it be direct or through intermediaries.”

As banks have withdrawn from a range of lending operations, BlueMountain has considered different ways to profit: sometimes by lending directly, but often by taking equity stakes in alternative lenders.

To date, it has made investments in Navitas Lease Corporation, which provides loans against equipment; Global Lending Services, which provides car loans; and Shellpoint, which provides mortgages.

“Pre-crisis, they either were within the banking system or largely funded by the banking system,” observes Mr Feldstein.

As well as attracting former bank clients, the hedge fund has attracted many former bank staff. Mr Feldstein left JPMorgan to found BlueMountain in 2003 with Stephen Siderow from McKinsey – and, since then, bankers have continued to walk through BlueMountain’s door. Among those to have joined the company have been Jes Staley, former head of investment banking at JPMorgan, and a cluster of senior bankers from Goldman Sachs.

But while the hedge fund aims to profit at the expense of traditional banks, it can also help to solve some of their problems. It was BlueMountain that took the other side of JPMorgan’s infamous “London whale” trade – and made money from the bank’s botched bet on credit derivatives. But it was also BlueMountain to which the bank turned to extricate itself, by requesting that the asset manager unwind some of the trades.

Similarly, when Crédit Agricole wanted to improve its capital ratio in 2012, BlueMountain stepped in to buy one of its trading desks, helping the French bank to reduce its risk-weighted assets by €14bn.

But the hedge fund, and others like it, has not been able to benefit from a more widespread bonfire of the balance sheets that some had predicted. Mr Feldstein suggests that regulators have given banks so much breathing space that they have been able to avoid the fire sale of assets that some shadow bankers had longed for.

“Regulators in most jurisdictions decided that they were not going to be as aggressive as they might otherwise have been,” says Mr Feldstein. “I think there was not nearly the wave of selling that people had anticipated.”

Renshaw Bay: helping banks reduce capital requirements

Bill Winters, pictured, was one of the first wave of shadow bankers to emerge in the aftermath of the financial crisis, writes Patrick Jenkins in London.

A former number two at JPMorgan – and heir apparent to chief executive Jamie Dimon until the two men fell out – he began planning his private debt fund soon after leaving the US bank in 2009.

By tapping longstanding financial connections in Europe, he was soon able to secure principal backing from two of the region’s wealthiest family investment groups: RIT Capital Partners, Lord Rothschild’s listed investment trust; and Reinet, the Luxembourg investment vehicle of Johann Rupert, a South African financier, which was created from the restructuring of Richemont, the Swiss luxury group.

Having raised additional funds from third parties, Mr Winters’ Renshaw Bay oversees close to £2bn of funds, and specialises in the two activities most dislocated by the financial crisis and the regulatory response to it: commercial property lending and corporate credit.

Renshaw Bay is also involved in what it calls “bank capital optimisation” – or “arbitrage”, as critics prefer to describe it. This involves taking on slices of a bank’s credit risk exposure in certain areas.

In this way a non-bank such as Renshaw Bay, with modest capital needs, can reduce a bank’s ever-higher regulatory capital requirements.

Critics point out that this is in essence a version of the pre-crisis arbitraging that weakened the global banking system – and left many conventional and shadow banks vulnerable to collapse.

But there is a crucial difference, according to Mr Winters: today’s structures involve a genuine transfer of risk, with Renshaw Bay typically taking “first-loss” slices of banks’ credit exposures.

Mr Winters is well placed to understand both the opportunity and the risk that come with providing non-bank finance. Aside from his inside knowledge of banking, the US-born Anglophile has been an architect of the UK’s regulatory response to the crisis.

First he sat on the Vickers commission, the UK government-appointed body behind the ringfencing plan to isolate banks’ retail operations from their riskier investment banking units within five years.

Then he was commissioned to write a report on lending reforms for the Bank of England. Among his proposals was a suggestion that non-banks be treated more like banks when it came to access to central bank finance – an idea that seems to have found favour with Mark Carney, the BoE governor.

Mr Winters brushes off suggestions that his stint in public service roles has helped him to feather his own nest. An expansion of shadow banks – or “non-bank financial institutions”, as he prefers to call them – is essential if the economy is not to be derailed by moves to make banks safer, he says.

There is particular scope for traditional bank finance to move to the “shadows” in Europe, he says, where three-quarters of corporate credit is still supplied by banks, the inverse of the situation in the capital-markets dominated US.

Mr Winters accepts that if shadow banks are to be brought more into the fold, tougher regulatory oversight will need to follow. At the moment, however, Renshaw Bay is subject to what he describes as a lot of bureaucratic form-filling but no meaningful supervision.

This, he says, will be the next challenge for the authorities. With thousands of companies like his springing up in London, New York and elsewhere – and many of their lending risks correlated but little understood – shadow banks are fragmenting the world in a way that will make the next crisis harder to spot.

Corsair Capital: spun out of JPMorgan

Since Lord Davies of Abersoch, pictured, joined Corsair Capital nearly four years ago, the US private equity group has struggled to generate the returns he would have liked from investing in the financial services sector.

Corsair, which spun out of JPMorgan Chase in 1992, could certainly do with a few successes to boost its performance. Its third fund raised about $1bn in 2006, to back financial services companies – but it suffered from the bad timing of investments made shortly before the financial crisis and is down more than 6 per cent in the past five years, according to one investor.

As a result, in 2010, the New York-based group was only able to raise $863m towards the $1.5bn target for its fourth fund, according to research house Preqin. This fund is now down more than 5 per cent over three years.

Nevertheless, the diminutive 61-year-old former chief executive and chairman of Standard Chartered, remains buoyant. “The world is awash with money from high net-worth individuals, pension funds and sovereign wealth funds,” he argues. “A lot of that liquidity is going to shadow banks, which will generate a very good yield from all this activity.”

Born into a Welsh-speaking family living in Colwyn Bay, Lord Davies followed his father into banking after school by joining Midland Bank. He went on to spend a decade at Citigroup in London before joining Standard Chartered in 1993.

His 15-year career at Standard Chartered ended in 2009 when he was appointed trade minister under the last Labour government. The following year, when Labour lost the election, he surprised many people in the banking industry by joining Corsair.

Before becoming trade minister, he had been mentioned as a possible chairman of Royal Bank of Scotland, after its bailout by the British government.

And, like Bill Winters – the former head of JPMorgan’s investment bank who now runs the credit fund Renshaw Bay – Lord Davies still crops up on lists of potential candidates whenever a big UK bank’s chairmanship opens up. However, both men seem to prefer life out of the spotlight.

“There’s a great shift of talent,” he says. “Bill Winters and I are examples of people who would have been expected to run or chair a big bank, but we’re both in shadow banking. There is a generation of bankers that find the demands and exposure of running a big financial institution too great.”

His most high-profile deal since joining Corsair was buying buy 314 branches of RBS that the bank was forced to sell by the European Union, as a condition of its state bailout.

Corsair joined forces with fellow US private equity investor Centerbridge to lead a bidding consortium with backing from RIT Capital Partners, the investment vehicle of Lord Jacob Rothschild, and the Church of England’s investment unit.

The consortium paid £600m for a stake of slightly less than 50 per cent in the branches that are to be rebranded as Williams & Glyn’s. It will work with RBS on a carveout of the business, with the aim of floating on the stock market in 2016.

Lord Davies enthuses about the “huge process” of change taking place in the banking system, and points out that Corsair is playing the long game.

“You don’t redefine the most important industry overnight,” he says. “This will be a 10 to 15-year process. It is about making sure that the system is safer and ensuring that the banks don’t blow up again.”

Sunny Hill Top: ‘The quality of our customers is worse’

For a lender that is supposed to operate in the shadows, Sunny Loan Top has an incongruous name. But then, until recently, the small Chinese finance company did not seem likely to morph into a quasi-bank, doling out tens of millions of dollars in high-interest loans to high-risk clients, writes Simon Rabinovitch in Beijing.

The fact that the group has undergone such a rapid evolution in such a short period of time tells a lot about the ingenuity of Chinese entrepreneurs – and the dangers that stem from the rise of shadow banking.

Initially the company, which was founded in 1988 in Ningbo, a coastal city home to many small exporters, operated a mishmash of businesses: electronics, car repairs, department stores. But in 2008, before China unleashed a gargantuan stimulus in response to the global financial crisis, credit was becoming hard to find. It was then that Sunny Loan (or Big Red Eagle Enterprises as it was known at the time) realised that it could make money by lending spare cash.

Its first lending ventures were small scale – more pawnshop than shadow bank. But the company soon found that its profits from lending far outstripped those from making trinkets for export.

“We are very clear now that financing is our main business,” says Lin Weiqing, Sunny Loan’s soft-spoken board secretary, who has been with the group since the 1980s.

Of its Rmb2.3bn ($370m) in assets, Rmb1.1bn is loans to other companies. But Sunny Loan is also guarantor of a further Rmb980m in loans. Together the loans and credit guarantees make up more than 90 per cent of total group assets.

For all the money coursing through the group, and China’s shadow banking industry more generally, Sunny Loan’s headquarters are disarmingly modest. In a meeting room staff sit on plain wooden furniture and drink tea from paper cups. The only decoration is a small river-and-mountain watercolour.

But, as China’s economy slows and financial strains mount, the number of potential clients wanting a meeting has soared. Ms Lin says the company is having to become more selective. “We see a big need for financing, but there just aren’t that many good projects out there,” she says.

Her caution is born of experience. Reports of near-defaults in China’s shadow banking industry caused concern in the market this year, though for Sunny Loan they are a way of life. In the past five years it has sued 19 borrowers for missing debt payments – and those lawsuits were a last resort.

And a successful litigation can merely be the start of a protracted battle for repayment. In 2011 a court ruled that Shanghai Xingyu Real Estate had defaulted on a Rmb37m debt, but Sunny Loan is yet to collect the money or collateral.

When Ms Lin and her board do sign off on loans, however, they have been able to demand dizzyingly high interest rates. In recent deals they lent Rmb60m to Jinchen Siji Real Estate for one year at 21.6 per cent, and Rmb50m to Huadong Real Estate for 18 months at an annualised rate of 20 per cent.

The vast majority of Sunny Loan’s credit goes to real estate and construction companies – sectors to which banks all but refuse to lend.

“As a rule the quality of our customers is worse than those that banks have, so we have to be extra careful with our risk controls,” Ms Lin says. “But even with the best due diligence, conditions sometimes change, cash runs short and borrowers can’t pay us back.”

GSO Capital Partners: ‘We can’t have a run on the bank’

Earlier this year, GSO Capital Partners, the credit arm of private equity group Blackstone, raised a $750m fund to provide loans to homebuilders for the purchase of land, writes Henny Sender in New York.

GSO had first ventured in to land bank financing through its junior debt fund, in 2012. It provided a $125m loan to Hovnanian Enterprises – making a return of almost 50 per cent on the deal in a mere six months.

Since then, GSO’s money has been in great demand, as US banks have become subject to new regulations limiting the amount of capital they can lend against land development.

“Such higher capital requirements make banks safer and give alternative capital funds their raison d’être,” says one competitor.

Indeed, a mix of tougher regulation and easier money – which has cut returns on mainstream investments – has worked to the advantage of the credit operations at all private equity firms, and none more so than GSO.

Blackstone bought the credit operation in 2008 when GSO had a mere $10bn in assets, in an attempt to exploit the turmoil in the credit markets.

Before Bennett Goodman formed the business with Tripp Smith and Doug Ostrover, the trio had worked together at US investment bank Donaldson, Lufkin & Jenrette, and later at Credit Suisse First Boston, when it acquired DLJ. At the Swiss bank, Mr Goodman ran the unit that provided finance to private equity groups seeking to do leveraged buyout deals.

Today, he is still doing that, which has enabled GSO to expand its assets to more than $66bn – almost exactly as much as Blackstone’s main private equity operation. Some now suggest Mr Goodman may one day run the whole firm, alongside Blackstone’s property guru, Jon Gray.

And, although GSO’s net income fell 18 per cent in the first quarter, GSO’s credit operation is widely accepted to be far more scaleable than Blackstone’s buyout business.

It also appears more flexible, and far less risky, than the business model of the banks, because of the way it structures deals. In addition to charging higher interest rates to compensate for the risk, GSO takes large amounts of collateral to make sure it will get its money back, as well as equity warrants in some instances, or equity stakes in its borrowers.

In March, for example, GSO gave Ring International Holdings, an Austrian stationery and coatings company, $200m in a mix of debt and structured securities to fund its acquisition of Helios, a competitor. Ring had lacked access to bank finance and was too small to turn to its local capital markets. As a result, the interest rate on the loan was 12 per cent. In addition, GSO received free equity warrants which, if exercised, could give it a one-third stake in Ring.

In most cases, GSO does not have to compete directly with the banks, either. It deals with clients who cannot access bank finance and have no option but to take the more expensive money on offer from GSO.

But, while the banks do not want to make land bank loans themselves, they will provide leverage to the likes of GSO – by offering credit lines.

GSO argues that, by providing loans to borrowers that banks will not consider, they make the financial system better and safer. “We are not a domino,” argues Mr Goodman. “We have long-term capital. We are not vulnerable to forced selling by others. We can’t have a run on the bank.”

Fifth Street Finance: ‘There are some questionably creative models’

Leonard Tannenbaum can attribute at least some of the early success of his shadow banking business – Fifth Street Finance – to being on the right side of David Einhorn, pictured, writes Tracy Alloway in New York.

As a close poker buddy of the billionaire hedge fund manager, Mr Tannenbaum benefited from one of Mr Einhorn’s calls during the dark days of 2008 – when Fifth Street Finance was trying to launch an initial public offering as share prices of banks and other financial companies plummeted.

At that time, Mr Einhorn was aggressively betting against Allied Capital – which, like Fifth Street, was a type of financial business known as a “business development company”. But he chose to back actively Fifth Street’s development.

Business development companies (BDCs) are widely considered a part of the broader shadow banking system, as they make loans to small and midsized companies or invest in their debt while enjoying a tax-free status that makes them popular with investors.

And, as has happened in other pockets of the shadow banking system, the assets held by BDCs have ballooned in recent years – thanks to a combination of low interest rates, yield-starved investors and new regulations governing conventional banks. Chief among these is new leveraged-lending guidance created by US regulators, in a move to rein in the riskiest loans to the most indebted companies.

“When you’re squeezing the banks, the money’s got to go somewhere,” points out Mr Tannenbaum, who is chief executive of Fifth Street Management, which advises Fifth Street Finance and another BDC. “It’s going into shadow banking, although I hate that term. We go where the banks can’t tread.”

This shift has increased the assets of publicly traded BDCs from about $28bn in early 2008 to $43bn in the third quarter of last year, according to data from Wells Fargo.

At the same time, a host of privately owned BDCs are on the verge of selling shares to investors for the first time, as they seek to tap strong investor demand for stakes in alternative lenders.

For Mr Tannenbaum, 42, the rapid growth of the industry is both a vindication of the BDC business model and a potential threat to its long-term future.

“There are some questionably creative BDC models out there,” he warns. “We don’t need another Allied Capital.” In 2008, Mr Einhorn’s bet against Allied Capital ultimately earned the hedge fund manager a reputation as a savvy predictor of the financial crisis, and some hefty profits, as shares in the BDC fell heavily.

Mr Einhorn’s backing for Fifth Street, through his hedge fund Greenlight Capital, therefore singled out Mr Tannenbaum’s business as something of an outsider in the BDC industry. It is a position that has been reinforced by Mr Tannenbaum’s public criticism of a proposal to double the amount of leverage, or borrowing, allowed at BDCs.

In his book on the episode, Fooling Some of the People All of the Time, Mr Einhorn paints himself as a crusader who went up against a “dishonest company” when other watchdogs – notably regulators and credit rating agencies – did not.

Mr Tannenbaum echoes this sentiment in his own warnings about the sector’s rapid growth.

“David Einhorn and I have something in common: we believe in complete transparency and, with that, we try to right the wrongs in the industry. Maybe that’s why we’re such good friends.”