‘Consistent’ Earnings Surprises

June 25, 2014 Leave a comment

‘Consistent’ Earnings Surprises

Cornell University – Dyson School of Applied Economics and Management; Korea University – Department of Finance

Florida State University

London School of Economics & Political Science (LSE)

May 5, 2014

Abstract:

We hypothesize that analysts with a bullish stock recommendation have an interest in not being subsequently contradicted by negative firm-specific news. As a result, these analysts report downward-biased earnings forecasts so that the company is less likely to experience a negative earnings surprise. Analogously, analysts with a bearish recommendation report upward biased earnings forecasts so that the firm is less likely to experience a strong positive earnings surprise. Consistent with this notion, we find that stock recommendations significantly and positively predict subsequent earnings surprises, as well as narrow beats versus narrow misses. This predictability is concentrated in situations where the motivation for such behavior is particularly strong. Stock recommendations also predict earnings-announcement-day returns. A long-short portfolio that exploits this predictability earns abnormal returns of 125 basis points per month.

Biased Analysts Create Big Profits?

Jack Vogel, Ph.D. 06/19/2014 22:04

‘Consistent’ Earnings Surprises

Hwang, Liu, and Lou

A version of the paper can be found here.

Want a summary of academic papers with alpha? Check out our free Academic Alpha Database!

Abstract:

We hypothesize that analysts with a bullish stock recommendation have an interest in not being subsequently contradicted by negative firm-specific news. As a result, these analysts report downward-biased earnings forecasts so that the company is less likely to experience a negative earnings surprise. Analogously, analysts with a bearish recommendation report upward biased earnings forecasts so that the firm is less likely to experience a strong positive earnings surprise. Consistent with this notion, we find that stock recommendations significantly and positively predict subsequent earnings surprises, as well as narrow beats versus narrow misses. This predictability is concentrated in situations where the motivation for such behavior is particularly strong. Stock recommendations also predict earnings-announcement-day returns. A long-short portfolio that exploits this predictability earns abnormal returns of 125 basis points per month.

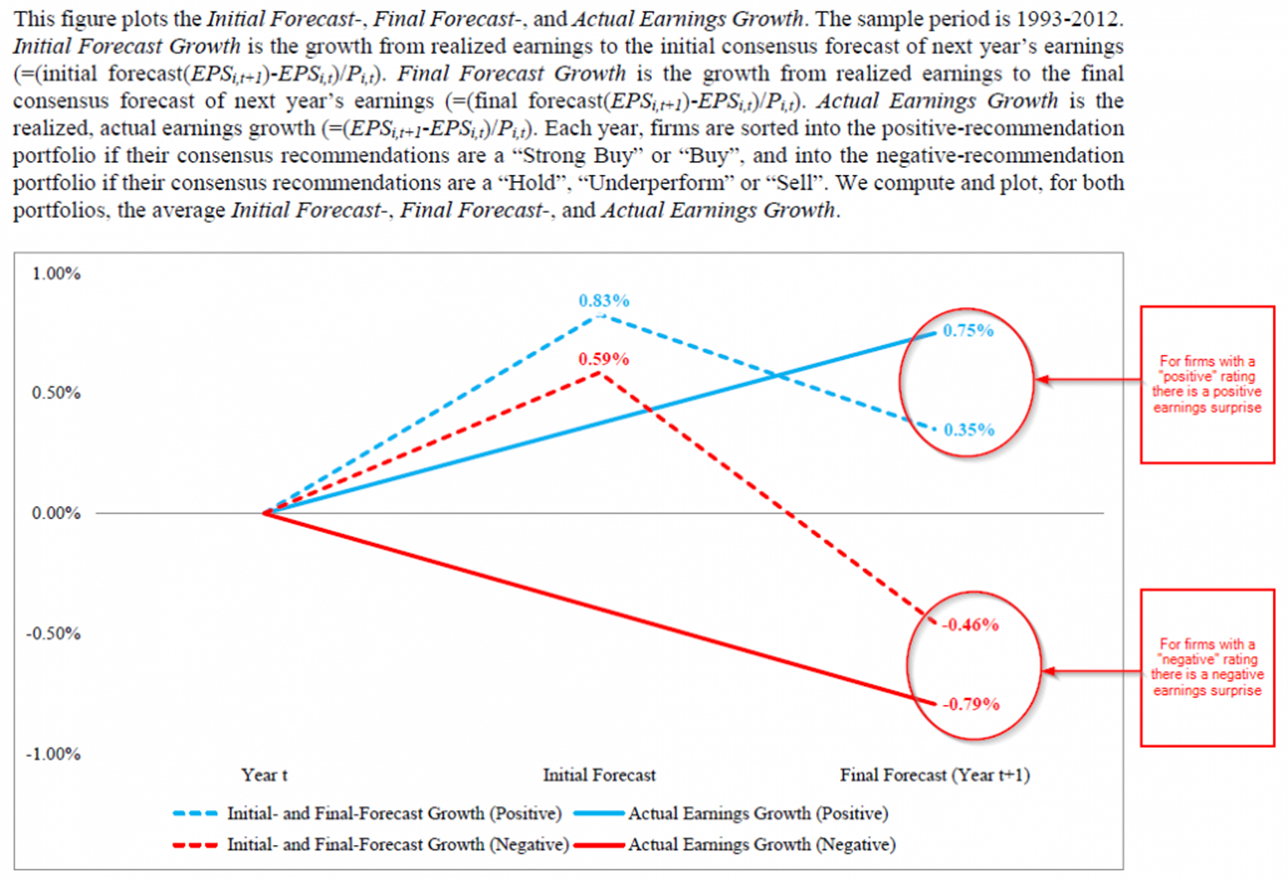

Alpha Highlight:

The paper documents that analysts with a bullish recommendation walk down their EPS growth estimates (creating a positive surprise). For analysts with a bearish recommendation, EPS growth estimates are too high (creating a negative surprise). The paper shows this in the figure below:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

Is there a way to take advantage of this? The paper recommends the following trading strategy:

From page 23 and 24:

To better assess the economic magnitude of our finding, we employ the following calendar-time portfolio approach: We sort earnings announcements into two groups based on the consensus recommendation prior to the earnings announcement. On any given trading day, we purchase stocks that have a strong buy/buy consensus recommendation and that are announcing earnings in three trading days (i.e., we purchase stocks at time t=-3, where t=0 is the earnings announcement day or the next trading day if earnings are announced on a non-trading day; “long leg”). We short stocks that have a hold/underperform/sell consensus recommendation and that are announcing earnings in three trading days (“short leg”). Each stock is kept in the long/short-portfolio for seven trading days (i.e., until t=+3). If on any given day, there are less than or equal to 10 stocks on either the long or short side, we hold the 3-month Treasury bill instead of the long-short portfolio (this is the case for less than 5% of the trading days).

As shown below, this strategy produces significant monthly alphas (at 5% and 10% levels):

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index. Additional information regarding the construction of these results is available upon request.

150bps x 12 months = some SERIOUS annual alpha!