India expects Narendra Modi-inspired equity spree

June 30, 2014 Leave a comment

June 23, 2014 12:50 pm

India expects Narendra Modi-inspired equity spree

By James Crabtree in Mumbai

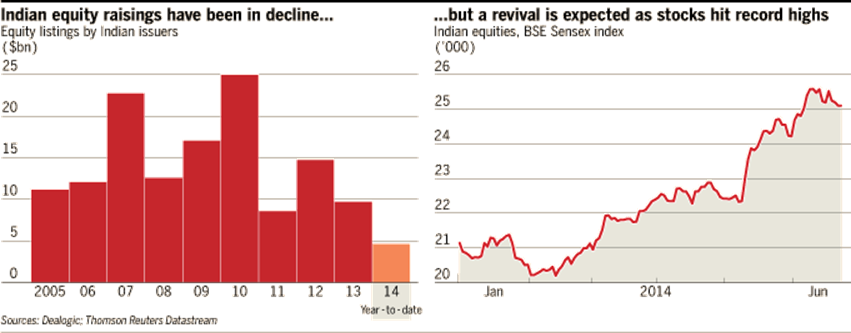

With stocks still close to record levels one month after the election of prime minister Narendra Modi, might India’s long-dormant equity markets be about to open up in earnest? So far, the signs are good.

The country is in the midst of a post-election “gold rush”, according to one senior investment banker at a global institution in Mumbai. “There aren’t enough hours in the day to have meetings with people who want to talk about raising money,” he says.

Capital markets in Asia’s third-largest economy have long been in a rut. Just $4.7bn of new equity has been raised over the past six months, according to data group Dealogic. That is roughly half the level at this stage in 2013, another weak year, and far below bumper periods such as 2010, which pulled in around $25bn overall.

This lengthy fallow spell partly explains India’s new optimism, however. “There is major pent up equity demand,” says Vedika Bhandarkar, head of investment banking at Credit Suisse in Mumbai. “Investors are feeling much more bullish . . . Over the next six to 12 months there will be substantial new equity raising.”

Early signs of life arrived soon after May’s poll. Shares hit all-time highs, prompting Yes Bank, a private sector bank, and Idea, a mobile telecoms group, to raise about $500m each from institutional investors.

Saurabh Mukherjea at broker Ambit Capital says he now expects half a dozen further institutional placements in the run up to Mr Modi’s inaugural budget in early July, ranging between $100m and $200m.

A number of heavily indebted industrial conglomerates are quietly sounding out investors for larger infusions, too, including power and energy group Adani, and Reliance Communications, the telecoms flagship of billionaire Anil Ambani.

The same is true for various public sector banks, many of which are struggling to meet strict new capital norms. Rana Kapoor, founder of Yes Bank, told the Financial Times last week that Indian companies could raise as much as $5bn by October, an improvement on recent years, although still far from “gold rush” territory.

Such hopes first require further action from Mr Modi, who has so far provided few details about planned economic reforms. These are expected in next month’s budget, and could in turn filter through into corporate valuations, especially in struggling sectors such as power and infrastructure.

A jump in foreign capital inflows has also been partly responsible for India’s bullish mood. Tapping further new sources of international money could provide a second crucial step for a revival of Indian primary markets, and especially initial public offerings, says Ayaz Ebrahim, head of Asian equities at French asset manager Amundi.

“This thing is really going to take off when those big global endowment and pension funds say we want to allocate separate chunks of money to India, and that is starting to happen,” he says.

One indication came on Monday, when the Canada Pension Plan Investment Board, a large Canadian fund with C$219bn in assets, confirmed plans to invest $166m in a division of Larsen & Toubro, India’s largest infrastructure group.

CPPIB’s move is part of a growing interest from sovereign and other long-term funds, attracted by prospects of an upturn in India’s economy, which could in turn provide renewed appetite for equity issuances.

One test of that demand will come whenever one of India’s many struggling industrial groups – long out of favour with investors – tests the market, as part of a drive to patch up its balance sheet.

Mr Modi’s government is itself likely to provide another. India raised less than half of a $9bn target to sell-off equity in government assets last year. Now its new prime minister looks set to launch a renewed push to sell-off stakes in large public sector businesses, including mining company Coal India.

Overall, India’s market recovery remains fragile. Any further increase in oil prices could dent valuations, as could a weak monsoon.

But after years of slowing growth and political drift, the return of companies seeking fresh funds for new ventures, rather than just to patch up old mistakes, will be the most important test of all, says Sunil Sanghai, head of global banking at HSBC in India.

“The real kicker in the capital market will come with the announcements of new projects either from the government or from the private sector,” he says. “There is a lot of long money abroad that is waiting to come in. The problem is not one of demand, the problem is one of supply.”