‘Alternative’ Mutual Funds: Different, Yes. Better? Not Lately. Funds With Nontraditional Strategies Haven’t Beaten Stocks Over the Past Few Years

June 6, 2014 Leave a comment

‘Alternative’ Mutual Funds: Different, Yes. Better? Not Lately.

Funds With Nontraditional Strategies Haven’t Beaten Stocks Over the Past Few Years

DAISY MAXEY

Updated June 2, 2014 5:22 p.m. ET

Investors spooked by the stock-market collapse of 2008 have been pouring money into so-called alternative mutual funds ever since. It’s a strategy that they hope will help cushion the blow if stocks take another dive.

It may still do that yet. But meanwhile, many of those investors have taken a beating on their alternative funds as stocks staged an impressive recovery. Consider it a lesson in what to expect from funds whose mission is to set a different course from the stock market. If these funds perform as expected, “you’re protected on the downside, but you’re really going to pay a price if the market is raging,” says Adam Zoll, an analyst at research firm Morningstar Inc.

There are varied definitions of what constitutes an alternative mutual fund. Morningstar doesn’t count funds that invest primarily in gold, real estate or certain other asset types commonly used to diversify a portfolio. Rather, its alternatives universe focuses on funds that use a variety of investing strategies in an attempt to produce decent returns with limited risk—and to have a pattern of returns that isn’t closely correlated with that of the broad stock market.

That includes funds that bet on some stocks to go up in price and others to fall, as well as “multialternative” funds that employ a variety of strategies and invest in stocks and bonds as well as other assets. These approaches make the funds likely to trail the broad stock market in a big bull market—and hopefully will help them hold up reasonably well in a bear market.

A very different subset of the alternatives universe are bear-market funds. These aim to go up when stock prices tumble, but they get clobbered when stocks rise.

There are other types of alternative funds as well. “In this area—perhaps more than any other—it’s important to understand the process, what the fund was designed to do and how it works,” to understand how each type of fund might best be used in a portfolio, says Mr. Zoll.

Plenty of Buyers

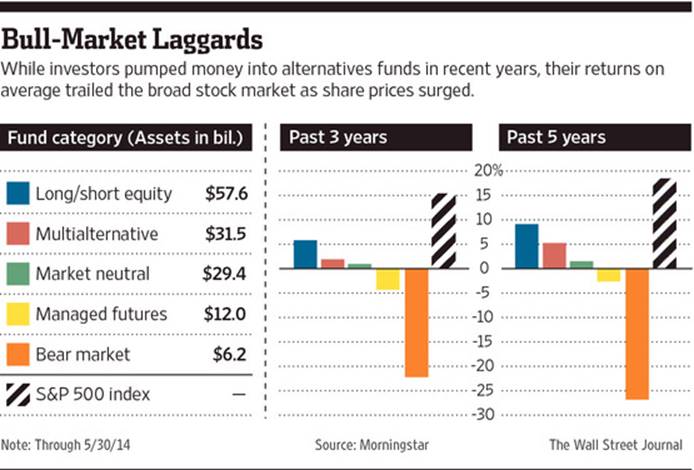

In 2008, some alternative funds cushioned investors as stocks plummeted. Since then, alternative mutual funds have grown faster than any other broad type of fund as defined by Morningstar, from about $36.4 billion in assets in 215 funds at the end of 2008 to $150.1 billion in 442 funds at the end of April.

Last year alone, 70 new alternative funds were launched and net inflows into the group topped $40 billion, Morningstar says.

In the first four months of this year, a net of $11.6 billion more flowed into alternative mutual funds.

Mixed Bag

Not surprisingly, bear-market funds have been big losers in this bull market. They posted an average annual return of negative 26.8% for the five years through the end of May, compared with an 18.4% annualized return for the S&P 500 stock index over the same period, according to Morningstar. Back in 2008, bear-market funds returned nearly 30% on average as the S&P 500 dropped nearly 40%.

Other types of alternative funds have fared better than bear-market funds in the recent bull market, but have still lagged behind the broad market. So far this year, with the S&P 500 returning 5.0% through May, alternative funds’ returns have ranged from an average of 1.6% for long/short equity funds to an average of negative 1.5% for managed-futures funds, according to Morningstar.

Long/short funds are the largest sector among alternative funds and have drawn the most money from investors in the three years through April—a net $35.71 billion, according to Morningstar. These funds take long and short positions in stocks in an effort to offer participation in rising markets yet protect investors when markets decline.

Multialternative and market-neutral funds are close to each other in asset totals, but multialternative funds—the ones that use a variety of strategies—have been much more popular with investors in recent years, taking in a net $19.85 billion in the three years through April, compared with $4.44 billion for market-neutral funds. Market-neutral funds aim to generate consistent returns regardless of the market’s direction by using a mix of long and short positions.

Managed-futures funds have far fewer assets, though still about twice as much as bear-market funds. Managed-futures funds employ derivatives, such as futures, options and swaps, to capitalize on price momentum, going long in markets that are moving up in price and shorting markets that have been falling. They have drawn a net $7.26 billion from investors in the three years through April, compared with $5.77 billion for bear-market funds.

Learning Curve

“These funds were designed for a flat to down market, and we haven’t had a flat to down market in so long that if you compare them to long-only equity funds, they’re going to show significant underperformance,” says Todd Rosenbluth, a fund analyst at S&P Capital IQ. “But that hasn’t stopped fund companies from launching them and investors from putting money in for fear that the market’s going to pull back sharply.”

Josh Charlson, director of alternative-funds research at Morningstar, wonders how many investors will have the patience to hold on to alternative funds for the long haul. “It’s partly a question of how well do investors understand the role that these should play in a portfolio,” he says.

His advice: Investors should view alternative funds as portfolio insurance and shouldn’t expect market returns. With that understanding, he says, alternative funds can play a long-term role.

“A well-selected basket of alternatives of different strategies can diversify a portfolio and can add that lower correlation [to stocks] that a lot of investors and advisers are looking for,” he says.