The Primary of Governance Pitfalls in Value Investing in Asia

June 19, 2014 Leave a comment

“Bamboo Innovators bend, not break, even in the most terrifying storm that would snap the mighty resisting oak tree. It survives, therefore it conquers.” |

| BAMBOO LETTER UPDATE | June 16, 2014 |

| Bamboo Innovator Insight (Issue 38) |

|

Dalang-mite: The Primacy of Governance Pitfall in Value Investing in Asia

“Habis manis sepah dibuang.” – Local Indonesian proverb, translated as “When the sweetness is gone, the pulp is thrown out”, referring to the chewing of sugarcane. It means that when something is no use anymore, it is disposed of.

Why are the faces and clothes of puppets in the wayang performance – a traditional Javanese show – painted with bright colors when the audience sitting behind the screen can only see their shadows? More importantly, why is the philosophy underlying the wayang performance critical for value investing in Asia?

The answer will be revealed shortly but first, let’s join the over 200 million locals who were reached out in the first televised presidential debate last Monday night in Indonesia, the world’s third-largest democracy, ahead of the July 9 presidential elections in the battle between ex-general Prabowo Subianto and the highly-popular Jakarta governor Joko Widodo (“Jokowi”) of the PDI-P party. Indonesia’s 11 privately-owned national TV stations reach 95% of the country’s 240 million people; newspapers reach only 12%. Two media tycoons, Hary Tanoesoedibjo and Aburizal Bakrie, who control nearly half of Indonesia’s TV audience, are backing Prabowo of the Gerindo coalition that controls a combined 292 seats, or 52% of the House.

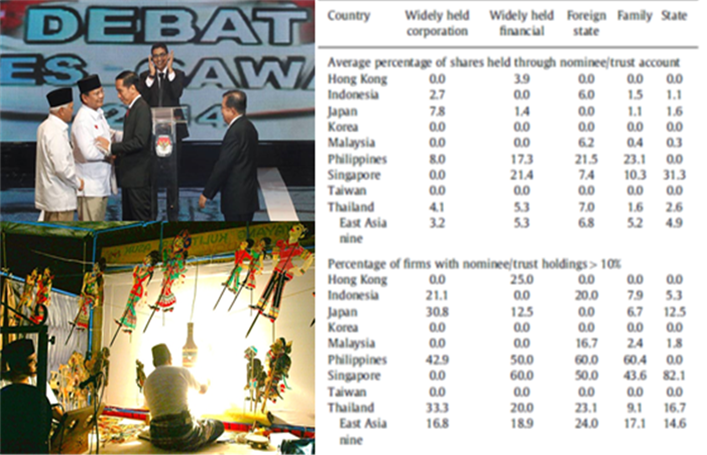

Top left: Presidential candidate Prabowo, second to left, greets his opponent Jokowi, center, next to vice presidential candidates Hatta, left, and Jusuf, right, before their TV debate. Bottom left: The dalang or puppet master in the wayang kulit show. Right: Prevalence of nominee and trust accounts by primary ownership category for 1,386 publicly traded corporations in 2008 (Source: Carney and Child (2013), Changes to the ownership and control of East Asian corporations between 1996 and 2008: The primacy of politics, Journal of Financial Economics 107: 494-513)

A missing argument in the presidential TV debate stands out. Prabowo and his running partner Hatta Rajasa surprisingly did not probe Jowoki-Kalla on the unspeakable problem: that Jowoki will always be suspected of being merely a puppet for Megawati Soekarnoputri, the former president, daughter of Indonesia’s first president Soekarno and current PDI-P chairwoman. As long-time head of the party, Megawati has the final say on major political decisions and the kingmaker has publicly described Jokowi as being only a party official appointed as presidential candidate and assigned to fulfil the party’s programme.

Thus, the answer to the opening question is revealed: Colors of the puppets are not meant to be seen by the common masses; only the audience behind the stage, those who are closer to the puppet master, the dalang, have the privilege of seeing the true colors of the faces and costumes of the puppets. When a warrior like Arjuna or Bima is about to appear, the dalang places on that puppet a golden mask. The privileged few behind the screen close to the dalang know in advance that a war is about to begin before the front audience sees it over the screen and they have a deeper understanding of the feelings and behavior of the manipulator.

The primacy of dalangs can be seen both at the politics and corporate risk level. Current president Susilo Bambang Yudhoyono (SBY) has familial ties with Prabowo’s running mate, Hatta, through their children’s marriage, even though SBY’s Democratic Party has taken a “neutral stance”. While the powerful Golkar party, the oldest and most established of all the political entities in Indonesia and the election machine behind long-time strongman Soeharto, is unable to put up its unpopular chairman Bakrie as the presidential candidate, it continues to play a pivotal role after making the unexpected announcement on May 19 that it would back Prabowo. Jusuf Kalla, the former Golkar’s chairman and still a card-carrying member, is Jokowi’s running mate as vice-president. Thus, Golkar has its feet in both doors for the country’s top job to maintain influence. It has been said whatever the outcome, the already entrenched corrupt practices will be business-as-usual with Golkar behind the scene.

At the corporate level, shares of most companies in Asia are not as widely held as those in the West. From the above table summarizing the prevalence of nominee and trust accounts by primary ownership category for 1,386 publicly traded corporations in Asia, Indonesia has one of the highest percentages of firms with nominee accounts or trust holdings that hide the ultimate identity of the shareholders at 21% for widely-held corporations and 7.9% for family-firms. When corporate transparency and governance is measured this way, the Philippines and Singapore clearly ranked at the bottom, while Taiwan is ranked at the top. The controlling owner with the ultimate beneficial ownership is like the dalang behind the screen, sitting at the apex of the complex pyramidal or cross-holding or dual-class structure controlling the puppet firm(s) with dexterity through layers of intermediate companies, opportunistically misrepresenting economic prospects given weak enforceable legal rules of investor protection in emerging markets. Insiders closest to the dalang would have advance knowledge of the dalang’s short-term plans, such as major contract wins that can trigger a jump in the share price, or issuance of shares that are dilutive to existing shareholders, or transferring of resources within the group of companies and affiliates via related-party transactions, positioning themselves ahead of the minority investors.

Thus, it would appear that avoiding pitfalls in value investing in Asia is about having “knowledge” about painted puppets and thedalang. Financial numbers are mere shadows and quantitative analysis, however sophisticated, cannot capture the intricate plans of the dalang, rendering clever short-term tactical gains irrelevant – often reversing in dramatic fashion without time for the investor to react and take portfolio action – once the dalang alters his or her plans, as evident from how high-profile western investors have stumbled when applying their once-successful investment methods in Asia without any adaptation. Hernando de Soto, the influential economist and author of the book “The Mystery of Capital: Why Capitalism Triumphs in the West and Fails Everywhere Else”, sums up why such an opaque dalang system is not effective in the long-run for sustainable value-creation: “Knowledge lies at the heart of western capitalism; Knowing who owned – and owed – what allowed long-term investors to take risks and allocate capital productively.”

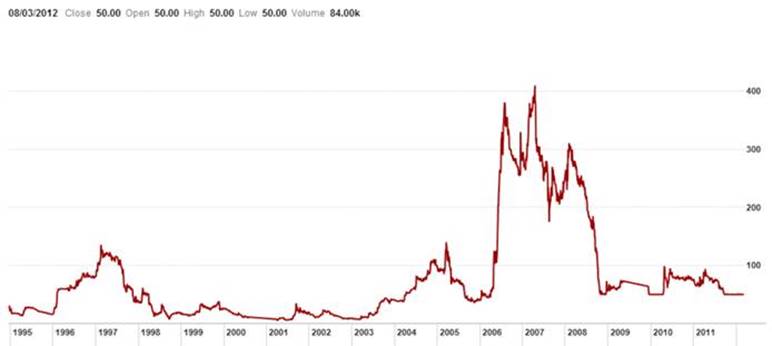

Although Indonesia is an investor favourite, corporate governance is a longstanding concern. The case of PT Davomas Abadi, supposedly Indonesia’s second-biggest cocoa processing and chocolate firm, is instructive on the ills of the dalang.

PT Davomas Abadi – Stock Price Performance, 1994-2014

<Article snipped>

We often wondered aloud and lament at the low valuations in Asia as compared to the West. Why is it that Asian entrepreneurs do not see the need to build “moats”, preferring to be the dalang? Asian entrepreneurs whom we spoke to over the past decade are often perplexed and exasperated why sales and earnings growth at their companies do not necessarily translate into corresponding market capitalization growth. Over time, some of these entrepreneurs….

<Article snipped>

Value investing in Asia has to progress beyond painted puppets and the dalang. Short-term clever tactical trades from “insider knowledge” about short-term plans of the controlling shareholders cannot be robust and sustainable. As the sagely Warren Buffett puts it aptly: “But in the end, the only wealth creation comes about through what the business creates. If a company that’s not worth anything sells for $20 billion and 5% of it changes hands, somebody takes $1 billion from somebody else, but investors as a whole gain nothing. They are all fee richer. It’s a very interesting phenomenon. But they can’t be richer as a group unless the company makes them richer.” Asking the penetrating long-range fundamental questions, identifying the business model gaps of the emerging companies, assessing the possibilities whether they can cross the chasm to become Bamboo Innovators, and adherence to good governance principles – these are what diligent long-horizon value investors should possess to stay ahead of the curve when investing in the tricky minefields of Asia with all the dalang-mite.

To make headway in understanding Indonesia and Asia, one must first understand the profound philosophy of the wayang. Apart from excitement, the people went to the wayang to gain wisdom, insight, and peace of mind. The true spirit of thewayang is in alignment with the values of the Bamboo Innovator. Like the clown god Semar, who in the wayang plays often steps in to save the situation when more refined characters have failed, Semar’s role is also to expose the evil in the human character. He looks ugly but is kind-hearted, powerful but humble, brave but faithful. He appears stupid but is often brilliant and wise. Endowed with supernatural powers, Semar never once misuses them, but always comes to the rescue of the helpless. When Arjuna was groomed to be a good leader, the dalang said:

“To be a knight or a good leader, one must have a strong mind and character to bear troubles and sorrows, just as the earth has to bear everything which exists on the surface of the planet. A good leader must be like the sun, giving warmth and life to all creatures without expecting anything in return; like the moon, giving peace and joy to all; and like the stars twinkling in the sky, maintaining high ideals to serve mankind. He must also be like the ocean, vast and broad-minded; like the fire, fierce and just; like the wind, intelligently knowing the aspirations of the people; and like water, giving knowledge to all who thirst for it.”

To read the exclusive article in full to find out more about the story of PT Davomas Abadi, APP, Golden Key, Astra, including the impact of hidden controlling ownership on governance risks and business valuation, please visit:

Some updates:

1) We will be away from July 1 to July 11 for our mandatory military camp training in Singapore, following which we will be on a business trip in Italy from July 13-20.

2) Value Unplugged 2014 and Value Investing Seminar in July in Italy

Value Unplugged 2014 (www.valueunplugged.com) in Naples, Italy is now full. We’ll gather in a small, relaxed setting to learn and make friends. We’ll also attend Ciccio Azzollini’s sold-out Value Investing Seminar in July in Trani, Italy — the definitive summer conference for value investors – as one of the keynote speakers. http://www.valueinvestingseminar.it/content_/relatori.asp?lan=eng&anno=2014

|

| The Moat Report Asia |

|

“In business, I look for economic castles protected by unbreachable ‘moats’.” – Warren Buffett

The Moat Report Asia is a research service focused exclusively on competitively advantaged, attractively priced public companies in Asia. Together with our European partners BeyondProxy and The Manual of Ideas, the idea-oriented acclaimed monthly research publication for institutional and private investors, we scour Asia to produce The Moat Report Asia, a monthly in-depth presentation report highlighting an undervalued wide-moat business in Asia with an innovative and resilient business model to compound value in uncertain times. Our Members from North America, the Nordic, Europe, the Oceania and Asia include professional value investors with over $20 billion in asset under management in equities, secretive global hedge fund giants, and savvy private individual investors who are lifelong learners in the art of value investing.

Learn more about membership benefits here: http://www.moatreport.com/subscription/

https://www.moatreport.com/individual-subscription/?s2-ssl=yes

Our latest monthly issue for the month of June investigates the world’s #1 ODM (Original Design Manufacturer) and global #5 manufacturer of a consumer healthcare device product that is used frequently, even daily, thus providing the foundation for stable recurring cashflow. This company is also a hidden champion in a niche product segment (50-55% of group’s sales) that has become a high-growth fashion product currently accounting for less than 10% of the overall industry. The company is able to mass-manufacture this niche product, but not the giants, because of its unique process IP in flexible manufacturing system and know-how to handle large-scale complex orders. The manufacture of this product itself is difficult to replicate and requires FDA/CE licenses because of its medical device nature and the entry barrier is not capital but the know-how and R&D expertise. In particular, the manufacturing integrates different fields of science including polymer chemistry, physics, optics, engineering, materials control, process control, microbiology, and, injection molding. The firm has also developed a proprietary system of tracking the manufacturing process of different sets of product so that if a quality issue arose, when and where the problem set of products was being produced could be swiftly identified, thus diminishing the scale and cost of product recall. This system has helped the firm win the long-term trust of its ODM customers to place stable large orders. The Big Four giants do not have such a system and have to incur substantial losses from product recalls. The company also possess its own brand which has many loyal followers and support in its home market where it enjoys a 30% market share and contributes to 25% of group’s sales while sticky ODM customers account for 75% of group’s sales, mainly from the Japan market. As a result of its wide-moat advantages, the firm enjoys a consistently high ROE of 41%, double or triple that of the giants. From FY07 onwards, even during the depths of the Global Financial Crisis in 2007/09, the firm has not raised equity. Since listing in Mar 2004, the company has only done one rights issue in May 2005. Also, it is able to sustain a strong stable cash dividend payout (>70% with 3% yield) with its healthy net-cash balance sheet (net cash $30m; net cash-to-equity ratio 23%) and proven management execution in prudent capex expansion to support sustainable quality earnings growth. M&A deals in the healthcare and medical device sector has been growing due to their strong defensive nature and giants seeking growth to overcome their own patent cliff. The firm will always be an attractive takeover target by giants who wish to swallow it up to possess its valuable flexible manufacturing system and know-how to fill their own missing competency gap and hence will enjoy long-term downside protection in its terminal value. In the battle between “ODM vs Brand”, we find the story of the company to be quite similar to that of TSMC (2330 TT, MV $103bn), now the largest ODM foundry in the world. “Skate to where the puck is going to be, not where it has been,” as hockey legend Wayne Gretzky advised. In our view, the profit and valuation premium in the value chain will start to skate to the “Inno-facturers” who are the hidden ODM innovators (the brand behind brands) consolidating the industry, such as TSMC and this company. While its valuation is not cheap with EV/EBIT (FY13) at 20.6x, when we compare EV/EBIT relative to ROE, the company is relatively cheap, by as much as 130-220% when compared to giants and other comparables. When we compare EV/EBITDA relative to ROE, the valuation gap is 90-160%. This long-term valuation gap implies that the company, with its far superior and sustainable ROE, could potentially double to $2.4bn, as it continues to consolidate its niche product segment and enter into a new product cycle of an innovative product whose patents are expiring in 2014/15 (US/worldwide) to make ASP/margin improvements in sustaining quality profits and cashflow.Its share price has dropped 18% from its recent high and underperformed the index by 26% in the last six months. This will present a buying opportunity for long-term value investors who can penetrate beyond conventional valuation metrics because of a deep understanding of its business model and underlying source of its wide-moat advantages. In Asia, many firms break apart or become value traps due to shareholder conflict, envy and differences in opinion on the business direction of the company. The stable long-term corporate culture infused by the late founder, who established the company in 1986 with the current executive chairman and 2 other key shareholders, to combine the energy and ideas of everyone to work hard to keep the business running forever is underappreciated.

Our past monthly issues examine:

The Moat Report Asia Members’ Forum has been getting penetrating quality dialogues from our subscribers. Questions range from:

Do find out more in how you can benefit from authentic and candid on-the-ground insights that sell-side analysts and brokers, with their inherent conflict-of-interests, inevitable focus on conventional stock coverage and different clientele priorities, are unwilling or unable to share. Think of this as pressing the Bloomberg “Help Help” button to navigate the Asian capital jungle. Institutional subscribers also get access to the Bamboo Innovator Index of 200+ companies and Watchlist of 500+ companies in Asia and the Database has eliminated companies with a higher probability of accounting frauds and misgovernance as well as the alluring value traps.

|

| Professional Development Workshops for Executives and Lifelong Learners |

|

Our 8th run of the series of workshop From the Fund Management Jungles: Value Investing Exposed and Explored – (Part 1) Moat Analysis, (Part 2) Tipping Point Analysis and (Part 3) Detecting Accounting Fraud – on 14 June 2014 has been well-received with serious value investors, professionals, and serious lifelong learners attending, with some who flew in from Jakarta and KL!..

Our 9th workshop will be on Detecting Accounting Fraud Ahead of the Curve sometime later in the year.

Thank you for your support all this while!

|

|

Thank you so much for reading as always.

Warm regards, KB Kee

Managing Editor The Moat Report Asia Singapore Mobile: +65 9695 1860

A Service of BeyondProxy LLC 1608 S. Ashland Avenue #27878 Chicago, Illinois 60608-2013 Other offices: London, Singapore, Zurich

|

|

P.S.1 Here is a little more about my background: KB Kee has been rooted in the principles of value investing for over a decade as an analyst in Asian capital markets. He was head of research and fund manager at Aegis Portfolio Managers, a Singapore-based value investment firm. As a member of Aegis’ investment committee, he helped the firm’s Asia-focused equity funds significantly outperform the benchmark index. He was previously the portfolio manager for Asia-Pacific equities at Mirae Asset Global Investments, Korea’s largest mutual fund company. He holds a Masters in Finance and degrees in Accountancy and Business Management, summa cum laude, from Singapore Management University (SMU). KB had taught accounting at his alma mater in Singapore Management University and had also published an empirical research paper Why ‘Democracy’ and ‘Drifter’ Firms Can Have Abnormal Returns: The Joint Importance of Corporate Governance and Abnormal Accruals in Separating Winners from Losers in the Special Issue of Istanbul Stock Exchange 25thYear Anniversary Best Paper Competition, Boğaziçi Journal, Review of Social, Economic and Administrative Studies, Vol. 25(1): 3-55. KB has trained CEOs, entrepreneurs, CFOs, management executives in business strategy, macroeconomic and industry trends in Singapore, HK and China.

P.S.2 Why do I care so much about doing The Moat Report Asia for you? My personal motivation in embarking on this lifelong journey has been driven by disappointment from observing up close and personal the hard-earned assets of many investors, including friends and their families, burnt badly by the popular mantra: “Ride the Asian Growth Story!” I witnessed firsthand the emotional upheavals that they go through when they invest their hard-earned money – and their family’s – in these “Ride The Asian Growth Story” stocks either by themselves or through money managers, and these stocks turned out to be the subject of some exciting “theme” but which are inherently sick and prey to economic vicissitudes. They may seem to grow faster initially but the sustainable harvest of their returns is far too uncertain to be the focus of a wise program in investment. Worse still, the companies turned out to be involved in accounting frauds. Their financial numbers were “propped up” artificially to lure in funds from investors and the studiously-assessed asset value has already been “tunnelled out” or expropriated. And western-based fraud detection tools and techniques have not been adapted to the Asian context to avoid these traps.

After a decade-plus journey in the Asian capital jungles, it has been somewhat disheartening as I observe many fraud perpetrators go away scot-free and live a life of super luxury on minority investors’ hard-earned money. And these perpetrators make tempting offers to various parties in the financial community to go along with their schemes. When investors have knowledge in their hands, we have a choice to stay away from these people and away from temptations and do the things that we think are right. With knowledge, we have a choice to invest in the hardworking Asian entrepreneurs and capital allocators who are serious in building a wide-moat business.

|

| CONNECT WITH US

|

| MOAT REPORT ASIA OUR TEAM SUBSCRIBE MEMBERS CONTACT US

The Moat Report Asia Other offices: London, Singapore, Zurich |