The wisdom of the laity: Retail investors are more influential than most people think

June 20, 2014 Leave a comment

The wisdom of the laity: Retail investors are more influential than most people think

Jun 14th 2014 | From the print edition

“FOLKS are dumb where I come from,” wrote Irving Berlin in the musical “Annie Get Your Gun”. The song’s condescension towards yokels is reminiscent of professional investors’ disdain for their retail counterparts. The “smart money” in New York and London thinks it can make a living exploiting the “dumb money” of people who live in the sticks. Yet a new paper from researchers at the Federal Reserve shows that retail investors—in America, at any rate—are a lot smarter than the professionals imagine. In fact, they have a bigger effect on the markets than the highly paid investment strategists of Wall Street.

Much of the economic literature assumes that ordinary investors are “noise” traders who deal at random (think of Nate Silver’s book “The Signal and the Noise”). They trade too often, it is thought, and are susceptible to behavioural biases such as over-optimism and loss-aversion.

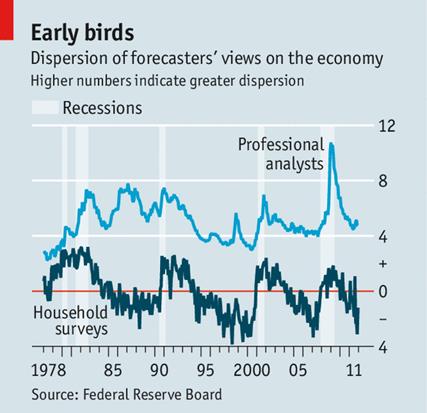

Some trading will always occur when investors have new cash to invest, or when they need to pay their bills. But it is also quite rational for investors to trade if their view of the economic outlook alters. The researchers tested whether they do using regular surveys conducted by Thomson Reuters and the University of Michigan, which ask consumers a series of questions about economic conditions. From these surveys they created a “belief dispersion index”, which shows when views on the economic outlook are most divided. That was then compared with the views of professional forecasters, as revealed in various surveys.

Strikingly, the researchers find that the views of retail investors show a sharp rise in dispersion just before recessions, whereas the views of professional forecasters do not diverge until the tail end of recessions. In other words, the amateurs are better at forecasting downturns than the experts (see chart).

This may be because the consumer surveys interview people with a wide range of backgrounds and from many different locations, whereas investment strategists are a tightly knit group, and may accordingly suffer from a herd mentality. One investment strategist once told your correspondent, “It makes no sense for me to predict a recession. If I’m right, no one will thank me and if I’m wrong, I will get fired.”

The next step for the researchers was to compare the beliefs of investors with stockmarket activity, both in the form of trading volume and in the form of mutual-fund flows. In both cases, when the views of retail investors diverged sharply, activity increased. In contrast, the views of professional investors seemed to have little impact. The paper concludes, “It is likely that household investors collectively have information that professional analysts do not have and therefore contribute to price discovery and market efficiency.”

Not all consumers are equal, however. The study finds that older (over 35), wealthier and better-educated (with at least a high-school diploma) investors are most likely to have an impact on trading volume—hardly surprising, as those are the people who are most likely to own stocks. The paper also finds that the stocks most affected by retail investors’ beliefs are the blue chips, the ones most likely to be of interest to the general public.

Given all this, why do retail investors have such a bad reputation? Part of the reason must be the propaganda put about by the finance profession: if the average guy realised he was financially shrewd, he would have no need to pay 1-2 percentage points a year to have his money handled by a fund manager. Yes, retail investors got caught up in the dotcom bubble of the late 1990s but so did professional investors. Tony Dye, a great tech-stock sceptic, was pushed out of his fund-management job in early 2000 by institutional clients, not Joe Public. Retail investors may overestimate the likely returns on their portfolios but so do the vast majority of American state and local pension funds. Nor is there any real evidence that retail investors panic in bear markets. The record week for equity-fund outflows was $20.5 billion in December 2000, just 1.1% of their assets at the time.

All professions are a conspiracy against the laity, said George Bernard Shaw. One way that conspiracy manifests itself is in the use of jargon, so that outsiders cannot follow what is going on. Another tendency is to belittle the contribution that amateurs make. The Fed paper shows, when it comes to markets, how wrong such assumptions can be.