The ownership of Italian firms: Untangled; Control of corporate Italy is changing hands

June 20, 2014 Leave a comment

The ownership of Italian firms: Untangled; Control of corporate Italy is changing hands

Jun 14th 2014 | MILAN | From the print edition

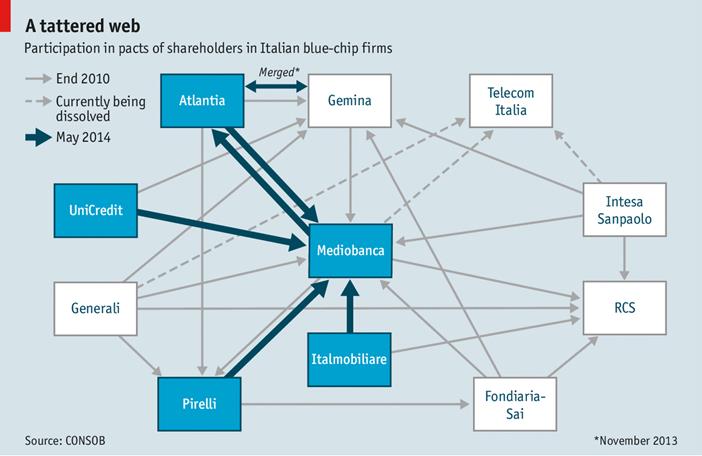

MEDIOBANCA was founded in 1946 with an explicit mission to rebuild Italian industry in the aftermath of the second world war. The result was a web of cross-shareholdings and pacts among big shareholders, with the Milanese investment bank at its centre, which allowed a narrow elite to control many of the country’s biggest businesses for decades. So the announcement last year that Mediobanca would exit these pacts and focus on its core business constituted a dramatic reversal. What with a similar move by Generali, Italy’s biggest insurer, the web is beginning to look a little tattered (see chart).

Mediobanca has sold €800m ($1.1 billion) of equities over the past nine months, half of its three-year goal. Both it and Generali say they will exit the pact that controls Telecom Italia this month, and eventually sell their shares. Privatisation is also changing things. The government is selling part of Fincantieri, one of Europe’s biggest shipbuilders, this month; Poste Italiane, the postal service, will probably be next. Many privately held firms plan offerings too, led by Cerved, a big data-services company. Commentators are hailing the emergence of the Italian “public company”, as controlling cliques retreat and foreign and institutional investors gain more clout.

Since 2010 the share of listed Italian banks held by once-controlling foundations has dropped slightly, while the free float has risen from 70% to 77%. Of the latter category, institutional investors with sizeable stakes almost doubled to 11.3%. Foreigners are a growing presence: in the past 16 months they invested €18 billion in Italy—€5 billion in the first four months of 2014 alone. The two biggest shareholders of Monte dei Paschi di Siena, a struggling bank which until recently was one-third-owned by a local foundation, are a Mexican asset-manager and a French insurer. BlackRock, an American asset-management colossus, is the main shareholder of UniCredit, Italy’s biggest bank; it has doubled its investments in the country over the past year and is now Italy’s biggest shareholder after the government.

The shift seems already to be affecting corporate governance. Attendance and participation at shareholder meetings have increased. The recent vote on a poorly drafted ethics clause put forward by the government at various partly state-owned firms illustrates the difference such shareholders make. At Eni, Finmeccanica and Terna, which have lots of institutional shareholders, the clause, which seemed to muddy the treatment of managers charged with financial crimes, was voted down. However at Enel, the former electricity monopoly, which has fewer institutional investors, it was approved.

There are also stirrings at the smaller family-run firms which account for 66% of Italian businesses. The Italian stock exchange has launched a programme to help such firms prepare for an eventual listing; interest has been high. Many family firms are managed by successful but ageing entrepreneurs whose offspring have little interest in taking over. Others need capital and outside expertise to grow and go abroad. Private-equity investment is also rising, albeit from a meagre base. Meanwhile, Mediobanca’s shareholders are changing too: the stake of participants in the pact that once controlled the firm has fallen from 55% in 2004 to 30% today.