Western Tools To Catch An Asian Snake?

January 13, 2015 Leave a comment

| “Bamboo Innovators bend, not break, even in the most terrifying storm that would snap the mighty resisting oak tree. It survives, therefore it conquers.” |

| BAMBOO LETTER UPDATE | January 12, 2015 |

Bamboo Innovator Insight (Issue 65)

|

| Western Tools To Catch An Asian Snake?“Why are there so many short-sellers’ reports, including those by Muddy Waters’ Carson Block, Kerrisdale’s Sahm Adrangi and Anonymous Analytics, in 2011? Why do so many Chinese stocks unravel in accounting frauds in 2011? There’s Sino-Forest, Long-Top, China Agri-Tech, ChinaCast Education etc. Is there a contagion effect in accounting fraud cases? Is accounting fraud a systemic risk? Why is 2011 so ‘special’ as a year of accounting fraud?”

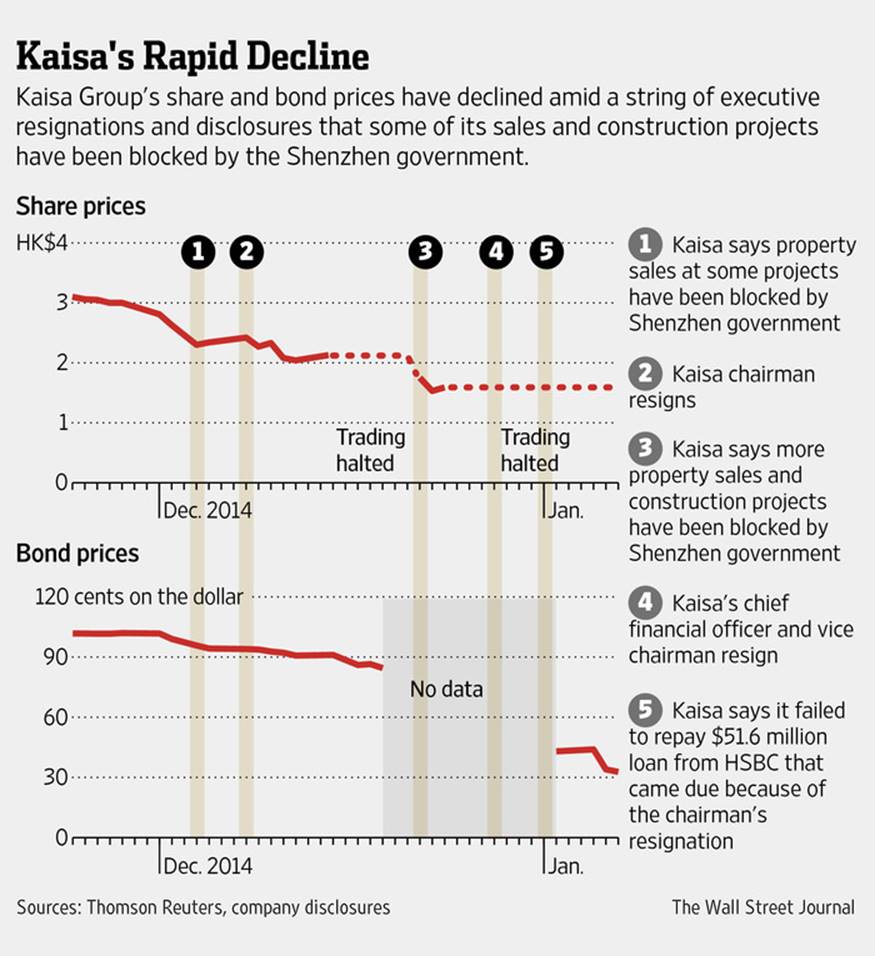

Interestingly, “2011” had happened before – in the late 1990s. This week marks the 16th anniversary of the bankruptcy of GITIC (Guangdong International Trust and Investment Corp) on Jan 16, 1999, which was the biggest in the history of China to date, and still the first and formal of a major financial institution. The collapse of GITIC led to the closure of hundreds of trust companies and thousands of urban credit cooperatives. Zhu Rongji tasked financial wizard Wang Qishan, the current Vice-Premier and anti-corruption tsar, to clean up the mess. Accounting irregularities were uncovered in many Chinese companies that were affiliated to GITIC. The central government did not bail out GITIC despite great expectations and foreign bondholders in GITIC saw a recovery rate of 12.5%. 2011 is the year of the shadow banking crisis rearing its ugly head, akin to the late 1990s, leading to a tightening in credit conditions, which in turn resulted in companies finding it more difficult to opportunistically use the roll-away “other receivables” accounting tunneling trick with cheap money. The GITIC case informed us that many of the audited investment and financial assets that stood in the books of the balance sheet to generate “revenue” in the income statement did not belong to GITIC at all since it held it in some sort of “trust”. Hence the low asset recovery rate. Credibility of China and Chinese financial system was tarnished for a long time. Last week also witnessed the first Chinese property company – Kaisa Group Holdings (1638 HK) – to default on offshore bonds held by foreign investors, ranging from BlackRock to Fidelity. Kaisa has total debt of around $5bn. This news was followed by the $24bn reorganization of the business empire controlled by Asia’s wealthiest entrepreneur Li Ka-Shing. The non-property assets of Li’s Cheung Kong (1 HK) and its subsidiary Hutchison Whampoa (13 HK) would be injected into a new company, Caymans-incorporated CK Hutchison (CKH). Property interests will go into another new Caymans-registered entity, Cheung Kong Property (CKP), which will seek a separate listing. The “official” reason is said to eliminate the 23% valuation discount that the Cheung Kong stock has to bear with as a holding company of Hutchison. Under the restructuring plan, Cheung Kong shareholders will receive one CKH Holdings share for every Cheung Kong share, while CKH will offer Hutchison shareholders 0.684 CKH share for every Hutchison share. All eligible CKH shareholders will receive one CKP share for every CKH share. The share swap ratio puts Cheung Kong shareholders, including the Li family, at an advantage. Hutchison shareholders will get 31% less of the new entity of the future property and non-property arms than their Cheung Kong peers. The Li family will get a 30.15% direct ownership in both the property and non-property arms, instead of an indirect holding of Hutchison through Cheung Kong. Noteworthy is that Hutchison could have sold its property business to Cheung Kong for the latter’s non-property assets. This could have been followed by a distribution of Hutchison shares held by Cheung Kong to Cheung Kong shareholders. In addition, Li’s controlled companies have been reducing their exposure to Greater China property, with Hutchinson Whampoa selling off its stake in Hutchinson Harbour Ring, which owns two properties in Shanghai, and other property assets in China. Coupled with the Kaisa default event, the strong actions appear to reflect his bearish outlook on the Greater China market, that something ominous could be imminent?… Warm regards, KB The Moat Report Asia http://accountancy.smu.edu.sg/faculty/profile/108141/KEE-Koon-Boon A new monthly issue of The Moat Report Asia is now available! Access the in-depth idea presentation: |