Worries about Federal Reserve policy have hit a favorite destination for mom-and-pop investors: closed-end bond funds. Leverage Juiced Returns When Rates Were Moored; Now It Is Magnifying Losses

June 24, 2013 Leave a comment

June 23, 2013, 4:52 p.m. ET

Closed-End Funds Bite Back

Leverage Juiced Returns When Rates Were Moored; Now It Is Magnifying Losses

Worries about Federal Reserve policy have hit a favorite destination for mom-and-pop investors: closed-end bond funds.

These mutual funds have suffered outsize losses during a rough month for bond funds overall. The average high-yield closed-end bond fund is down 10.7% in the past month through Thursday, according to Morningstar Inc. MORN +0.89% That compares with a 3.4% decline for its open-end counterpart.The same features that help closed-end funds offer fat returns, or yields, are backfiring amid rising expectations that the central bank will pull back on bond purchases that had kept interest rates low.

The primary culprit for the recent losses is leverage that debt-fund managers take on to boost returns.

Fund managers magnify gains by borrowing at low short-term rates and then turning around and investing in higher-yielding bonds that mature in many years.

But leverage also multiplies the losses when worries about rising rates take hold. The price of long-term debt tends to drop the most when rates rise, and the cost of borrowing climbs. This double whammy cuts into payouts that investors in closed-end bond funds receive.

Unlike standard mutual funds, closed-end funds issue a limited number of share¾s that trade much like stocks.

Individual investors own most of the shares in closed-end funds, market participants say. These funds held $276 billion at the end of the first quarter, according to Investment Company Institute. Of that, 61% was in bond funds, including a third in municipal-bond portfolios.

“People are going to be looking at their statements…and they could be down 10% for the year in a muni-bond fund,” says Daniel Lippincott, who follows municipal closed-end funds for Karpus Investment Management in Pittsford, N.Y., which oversees $2.5 billion. “And when you think muni bonds, you usually think safe.”

Other types of investments that offered high yields, such as real-estate investment trusts, utilities stocks and emerging-market bonds, also have taken a hit in recent weeks.

“Investors were looking for yield anywhere they can and not even caring what they were paying for it,” says Patrick Galley, chief investment officer at RiverNorth Capital Management in Chicago, a closed-end fund specialist which manages $2.4 billion. “All they could see is the high yields.”

At the end of May, the average closed-end high-yield bond fund was yielding 8.1%, according to Morningstar. Some municipal-bond funds were yielding 5%, which equates to yields topping 9% for some investors who can capitalize on the tax advantages that munis offer.

But those yields are being subsumed by a drop in prices.

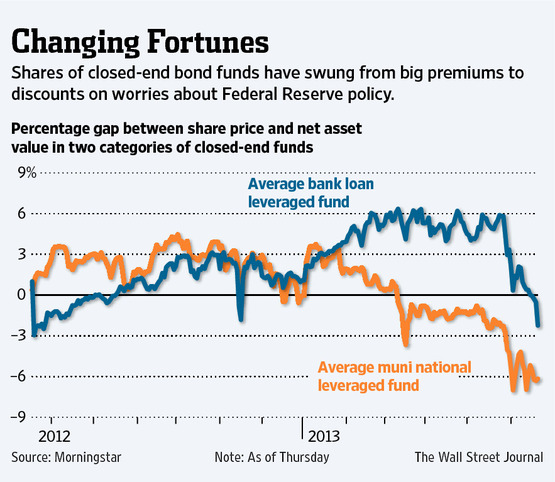

Throughout last year and into the early part of 2013, there were signs that closed-end bond funds were getting frothy. Many bond funds, especially those investing in long-term municipal and high-yield debt, were trading at prices well above the value of their underlying holdings.

Because closed-end funds have a fixed supply of shares, their share prices often deviate widely from the value of the bonds in the fund. When demand for these shares is high, they can trade at a premium to the value of the portfolio. When sellers dominate, they trade at a discount.

Shares in municipal closed-end funds on average were at a 6.2% discount Thursday, according to Morningstar. That compares with a premium of 2.1% at the end of January. The average high-yield closed-end fund, which had been at a 2% premium as recently as May 16, fell to a discount of 5.9%.

Some investors say the selloff is overdone.

Jonathan Isaac, who heads the $23 billion closed-end fund business at Eaton VanceEV +0.03% Investment Managers, noted that closed-end funds which invest in bank loans were caught up in the selloff, even though that corner of the market actually offers some protection from rising rates. Interest rates on bank loans generally rise together with prevailing rates.

The average bank-loan fund fell to a discount of 2.2% Thursday from premiums of 2.1% on June 6 and 5.8% on May 27, according to Morningstar.

RiverNorth’s Mr. Galley says he doesn’t expect bond yields to continue spiraling higher.

And given their steep declines, “munis are looking interesting to us for the first time in a long time,” he says.

Douglas Bond, who runs the $350 million Cohen & Steers Closed-End Opportunity Fund, which invests in other closed-end funds, says he is “selectively” adding to bond-fund positions.

While he thinks stocks are generally a more attractive proposition, Mr. Bond sees a potential silver lining in the market turmoil for bond funds.

A scenario where longer-term bond yields move higher, but the Fed keeps short-term rates low, could enable funds to earn greater yields off their leveraged investments and offset some of the damage from falling bond prices, he says. “The task gets a little bit easier for the fund manager,” says Mr. Bond.

At Karpus Investment, which manages about $2.5 billion, Mr. Lippincott says they have been buying “quite a bit.”

“If you can buy a fund at a 13% discount, over a two-, three- or four-year period you’re going to do OK because you’ve got a nice cushion,” he says.

However, there is the risk of more volatility.

If investors remain spooked, “you could see people just selling and these things going to a 20% or 25% discount.”