Bond king Bill Gross and his protégé Mark Kiesel are among the hardest hit from bonds’ recent declines, a sign the selloff has caught some of the most trusted hands in the investing community

June 26, 2013 Leave a comment

Updated June 25, 2013, 8:15 p.m. ET

Bond Selloff Creates Fits for the ‘King’

MIN ZENG and KIRSTEN GRIND

Bond king Bill Gross is one of the hardest hit from the broad credit market selloff.

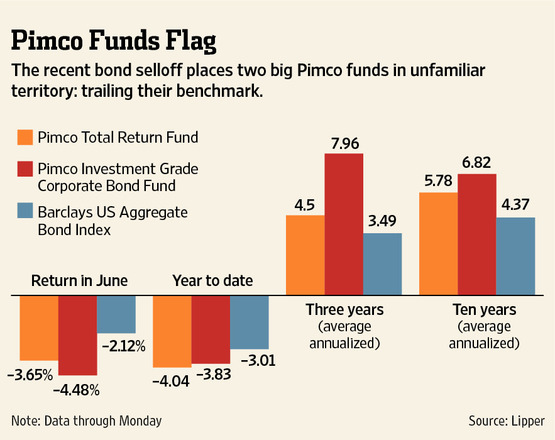

Pacific Investment Management Co.’s $285.2 billion Total Return Bond Fund has lost 3.65% in June alone, making it the 12th-worst performer among 177 similar bond funds tracked by data firm Lipper.The June losses come after investors pulled $1.32 billion out of the fund in May, its first outflow since 2011. Newport Beach, Calif.-based Pimco is a unit ofAllianz SE ALV.XE +1.27% .

The fund is now on a two-month losing streak, the latest evidence that the weekslong selloff in bonds ranging from ultrasafe Treasury debt to emerging-market securities has unnerved some of the most trusted hands in the investing community.

Even longtime investors fled. Ross Schmidt, a Denver-based financial adviser who has long invested client money in the fund, says he recently moved money out for the first time. “It was really painful, actually,” Mr. Schmidt said. “It was like saying goodbye to an old friend.”

Mr. Gross isn’t alone. Bond-market fears have pummeled mutual funds across the industry. All similar bond funds tracked by Lipper have performed poorly so far in June, posting an average loss of 2.65%. They are down an average of 4.29% since the end of April.

“In the short run, good managers can be out of place,” said Jeff Tjornehoj, head of Americas research at Lipper.

The bout of poor performance after years of strong returns is a blow for Mr. Gross, who for years has presented himself as the face of the surging bond market. The Pimco Total Return fund has returned 6.69% a year, on average, over the last 15 years, according to Morningstar, as of Monday. That compares with 5.49% average annual returns on the benchmark Barclays BARC.LN +1.45% U.S. Aggregate Bond Index. In 2010, Morningstar named Mr. Gross the best manager of the decade.

Mark Kiesel, a protégé of Mr. Gross, has fared even worse in the recent rout. His $11 billion Pimco Investment Grade Corporate Bond Fund has lost 4.48% in June through Monday, the biggest loser among intermediate investment-grade bond funds tracked by Lipper.

Mr. Kiesel was named in January as U.S. fixed-income fund manager of the year by Morningstar after his fund posted a 15% return in 2012, which beat the results of 98% of its competitors, including Mr. Gross’s fund.

A spokesman said Mr. Gross was unavailable for an interview Tuesday and Mr. Kiesel didn’t immediately respond to requests for comment. But in a question-and-answer note on the company’s website this month, Mr. Gross asked clients to be patient.

“Times are challenging, to be sure, but [Pimco] has been successfully investing through more than four decades of market and economic cycles, which gives us some perspective, as well as the confidence that we’re going to be around to fight for the next 40 years,” Mr. Gross wrote. “We certainly hope our clients take some comfort in that,” he added.

Mr. Gross’s fund is faltering now largely because of his holdings in U.S. Treasurys, which last week suffered the fastest rise in yields in a decade. Yields rise when prices fall.

Mr. Gross turned bullish and scooped up 10-year Treasury notes in April. The strategy initially went well as Treasury yields fell and prices rose that month. But the market started selling off in May as worries intensified that the Fed would pull back from buying bonds.

Mr. Gross cut Treasury bondholdings in May, but only marginally to 37% of the fund from 39% the month before, according to Pimco.

Mr. Gross has signaled from the company’s Twitter account over the past couple of weeks that the bond market selloff is overdone and could present a buying opportunity. He said Treasury bonds that mature in five years in particular are an attractive bet.

In an investor newsletter Tuesday titled “The Fog That’s Yet to Lift,” Mr. Gross said that investors selling Treasurys in anticipation of the Fed’s easing out of the market might be disappointed.

For the year, the Total Return Bond Fund and Mr. Kiesel’s corporate bond fund are faring worse than the bond market’s marquee benchmark index.

The bond fund is down 4.04% so far this year through Monday, and Mr. Kiesel’s is down 3.83%, according to Lipper, compared with a drop of about 3% for its benchmark, the Barclays Aggregate Bond Index.

The last time Mr. Gross saw outflows in the Total Return Bond Fund, in December 2011, was because of an ill-timed bet on Treasurys. Mr. Gross pulled out of Treasurys early in 2011, just before yields plunged.