Shedding of the Asian Snake’s Skin, The Opportunistic Tunneling of Corporate Wealth

January 26, 2015 Leave a comment

| Bamboo Innovators bend, not break, even in the most terrifying storm that would snap the mighty resisting oak tree. It survives, therefore it conquers.” |

| BAMBOO LETTER UPDATE | January 26, 2015 |

Bamboo Innovator Insight (Issue 67)

|

| Shedding of the Asian Snake’s Skin, The Opportunistic Tunneling of Corporate WealthDuring the 1990s in the city of Yichang, Hubei province, central China, you are considered a god if you are a “Monkey King” – if you work at the Monkey King Group (MKG) (宜昌猴王焊丝有限公司). MKG was a Shenzhen-listed industrial powerhouse as one of China’s 512 key SOEs (state-owned enterprises) and formerly China’s #1 maker of welding materials. Around 14 years ago, at the end of 2000, the parent company of MKG was placed in liquidation.The MKG case reminded us about the technical default saga of Shenzhen developer Kaisa Group Holdings (1638 HK). Bondholders and investors in earlier cases were burnt – investors in Suntech, Ocean Grand Holdings, Celestial Nutrifoods and China Milk Products Group got 5% or less, while investors in Asia Aluminum Holdings, which collapsed in March 2009 with $17.7bn of debt, received about 7%. Sino-Forest debtholders recovered 17%.

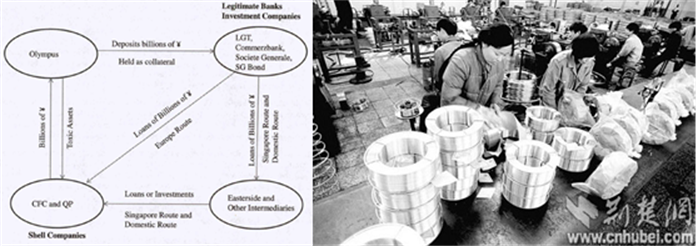

Like Kaisa and many of the Asian companies, MKG had guaranteed the loan of its parent company who had used the money to speculate in the stock market, property and speculative ventures. In Dec 2000, MKG started an accounting “tunneling” exercise that shrunk group assets from RMB2.42bn to RMB371m, according to its biggest creditor Huarong Asset Management who bought RMB622m in MKG debt. Tunneling is the very reason why the recovery amount is always a small fraction of the audited net asset value, and the reason why western-style financial statement analysis, the elaborate spreadsheets of net-net asset value etc, break down as garbage-in-garbage-out exercise in the Asian capital jungle. Loan guarantees presents a seemingly innocuous Opportunity to maliciously tunnel out corporate wealth in Asian companies. Take the case of Olympus. It deposited ¥21bn in Japanese government bonds with LGT Bank and arranged for the bank to use these bonds as collateral for a loan to two shell companies, the “tobashi”. The unconsolidated shells in turn used the borrowed funds to buy the toxic investments from Olympus at the original cost. Olympus recorded the amount it deposited with LGT and the toxic assets were considered “sold” to the shells, thereby avoiding recognizing losses on these underwater securities. In other words, Olympus acted as a guarantor of loans made by the banks to the shells by depositing funds at the banks equal to the amount loaned (figure on left).

(L): Olympus accounting: DR Government Bonds ¥21bn, CR Cash ¥21bn; DR Cash ¥21bn (from the shells), CR Toxic Financial Assets ¥21bn (“sold” to shells); (R): Photo of MKG plant in the 1990s Hence, cash in the balance sheet in Asian companies is invariably never really cash unless one examines these related-party transactions (RPTs), often held in scant regard by investors using western-style financial statement analysis and by Asian auditors. Even in Singapore, the Qualification Programme (SQP), a post-university professional accountancy qualification, does not cover at all the auditing of RPTs which is all-important in the Asian capital jungle. The Monkey King is just one of the many brief cases that we will be sharing in Week 4 of the Accounting Fraud in Asia course in SMU. Last week, we have discussed about the Incentivized Asian “Wedge” Snake with indirect measurements of accounting tunneling using the complex and opaque corporate structures set up by the controlling owners. This week, we are making the breakthrough to explore the Shedding of the Asian Snake’s Skin: The Opportunistic Tunneling of Corporate Wealth with the direct measurements of accounting tunneling. This Week #4 is a breakthrough in the sense that we are exploring new frontiers that have NOT been discussed even in top-tier accounting and finance research journals since the Asian Snake has adapted itself to escape the various measurements devised by researchers and practitioner. Take loan guarantee which has shifted to intercorporate loans, classified under “Other Receivables”. With some reforms mitigating these RPTs, the Asian Snake has adapted and shifted to other accounts in disguised forms. Hence our earlier article for a sense of urgency to develop a new composite measurement of tunneling. We will be dissecting both actual and potential real-world Asian accounting cases in this week and we’ll observe up-close the process in the shedding of the Asian Snake’s skin and the accounting transgression skin left behind. PS: Our monthly Moat Report Asia will be out in the week of 6 February. Warm regards, KB The Moat Report Asia http://accountancy.smu.edu.sg/faculty/profile/108141/KEE-Koon-Boon A new monthly issue of The Moat Report Asia is now available! Access the in-depth idea presentation: |