‘Dark Pools’ Face Scrutiny; Regulators Ask for Details on Stock Trading in Murkiest Parts of the Market

June 6, 2013 Leave a comment

June 5, 2013, 9:55 p.m. ET

‘Dark Pools’ Face Scrutiny

Regulators Ask for Details on Stock Trading in Murkiest Parts of the Market

WASHINGTON—Regulators are ramping up scrutiny of an opaque corner of the market where stocks change hands in the dark.

The Financial Industry Regulatory Authority, Wall Street’s self-regulatory body, last month sent 15 examination letters to operators of “dark pools”—lightly regulated, off-exchange trading venues that have been a rising concern for regulators and some investors as more activity shifts away from exchanges.

Finra is seeking details about how the increasingly popular venues operate, what they disclose to clients and whether they adequately police trades. It could bring enforcement action against dark-pool operators or issue recommendations for tighter oversight, depending on the answers it receives and additional examinations, said John Malitzis, executive vice president of market regulation at Finra. The letters are a follow-up to an initial round of questions the regulator circulated last fall.“We want to understand whether [dark pools] are disclosing to their customers how their orders work [and] whether customers are informed who their orders will interact with,” Mr. Malitzis said in an interview. “A big part of this is to get an understanding of practices that may or may not be problematic.”

Credit Suisse Group AG, CSGN.VX -2.37% Goldman Sachs Group Inc. GS -2.09%and Barclays BARC.LN -1.26% PLC, which operate three of the largest U.S. dark pools, were among the firms that received a letter, according to people familiar with the matter. Representatives for the three banks declined to comment.

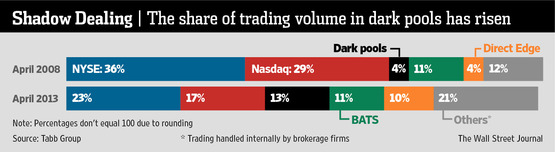

Dark pools don’t disclose traders’ buy or sell orders and only publish trade data after transactions occur. About 13% of all stock-market action takes place on dark pools, up from about 4% five years ago, according to Tabb Group, a market-research firm. Most dark pools are run by broker-dealers—firms overseen by Finra that buy and sell assets on behalf of customers as well as trade for their own accounts.

While dark pools command an expanding slice of trading volume, regulators still have little idea about how they operate since, unlike exchanges, they aren’t required to regularly disclose detailed information about their trading systems. Finra is weighing whether to submit a plan to the Securities and Exchange Commission this summer that would allow it to more closely track dark-pool trading volumes.

SEC enforcement officials also have been digging deeper into dark-pool trading. Daniel Hawke, the head of the SEC’s market-abuse unit, said at a legal conference in New York last month that, while dark pools aren’t “inherently bad,” they pose “potential for abuse, because the quoting activity can’t be seen.”

One form of suspicious dark-pool activity regulators are monitoring is whether firms are placing orders in the public market with the goal of manipulating prices in dark pools. High-speed traders can benefit by knowing the public price before it hits a dark pool. Finra Chief Executive Richard Ketchum in January told The Wall Street Journal that the regulator is broadening dark-pool oversight, with an eye on whether orders placed on public exchanges are “trying to move prices or encourage sellers that may advance their trading in the dark market.”

One area of focus for Finra is “order types”—commands dark pools and other trading venues use to determine how a client’s order interacts with other trades. The Finra letter asks for “any communications…sent for the purpose of explaining how an order type operates.” The letter also asks whether some order types are provided only to certain clients and, if so, for an explanation “why the order type is limited to certain parties.”

The SEC has for more than a year been investigating whether certain high-speed traders use order types on stock exchanges in ways that can hurt other investors. Finra hasn’t said whether it is investigating order types. For now, it is seeking additional information about how they work and are marketed and what dark-pool operators disclose about them, Mr. Malitzis said.

Finra also is seeking information about how various units of a broker-dealer interact with customer orders on the brokers’ own dark pools.

The letter asks whether a firm’s proprietary traders can “enter orders/quotes, or other trading interest” into its dark pool.

While the trading arms of broker-dealers can make markets on the dark pools they operate, regulators are concerned about broader sharing of information about client order flow with traders who can use that information to place trades elsewhere.

Another area of concern is whether dark-pool operators are policing for abusive trading activities.

The examination letter asks for details about the type of trading a firm’s surveillance system is designed to capture, organization charts showing individuals dedicated toward policing trading and response measures to “problematic activity.”

The steepening interest in how dark pools operate stems in part from recent investigations, said Mr. Malitzis. In 2011, the SEC fined Pipeline Trading Systems LLC, a now-defunct New York dark-pool operator, $1 million for allegedly failing to disclose that a secretive trading unit interacted with the vast majority of client orders. Pipeline didn’t admit or deny wrongdoing. Last October, a dark pool operated by several large Wall Street banks, LeveL ATS, settled SEC allegations, without admitting or denying wrongdoing, that it improperly shared confidential client trading information with a unit of Citigroup Inc., C -2.34% one of its investors.