An exodus from emerging markets threatens to hurt the financing and growth prospects of developing economies that have come to rely on large inflows of foreign capital in the wake of the global financial crisis

June 12, 2013 Leave a comment

Updated June 11, 2013, 6:05 p.m. ET

Money Flows Out of Emerging Markets

By ALEX FRANGOS and DANIEL INMAN in Hong Kong and PATRICK MCGROARTY in Johannesburg

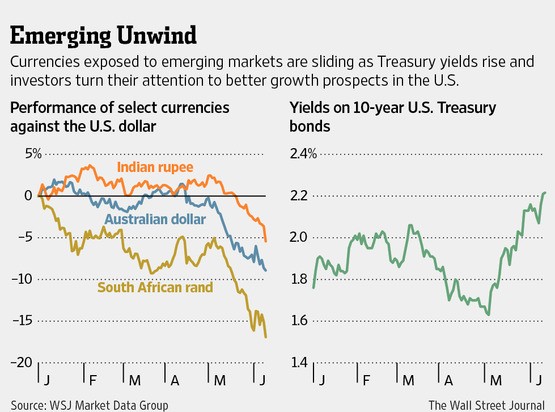

Money streamed out of emerging markets, destabilizing currencies, sinking stocks and creating headaches for policy makers already worried about faltering growth.

In the latest signs of turmoil, highflying stock markets fell in Asia, while currencies in India, Thailand and Indonesia reeled in the face of a surging U.S. dollar.

Some emerging-market currencies rebounded in New York trading hours but others remained weaker on the day. The volatile trading reflected the difficulties investors face in trying to predict when developed-world banks might start to withdraw stimulus and how such moves would ripple across global markets.An exodus from emerging markets threatens to hurt the financing and growth prospects of developing economies that have come to rely on large inflows of foreign capital in the wake of the global financial crisis.

Yields on Treasury bonds have risen as investors gird for the possibility that the Federal Reserve could ratchet back the monthly bond purchases it has been making in a bid to stimulate growth. That, along with a sense that the U.S. economy is outperforming the rest of the world, is making U.S. assets and the greenback look more attractive than relatively risky emerging-market stocks and currencies.

Investors’ nervousness was exacerbated Tuesday by a continuation of weak economic data from emerging economies. The Philippines said exports dropped 7% in April compared with the year before, reinforcing the view that global trade is slowing. Unrest in Turkey, investor disappointment over a Bank of Japan decision to leave its bond-buying program unchanged, and renewed concerns over Europe’s efforts to repair its fragile financial system added to the mix.

Asian stock markets were among the first hit.

Thailand’s benchmark index fell 5%, while the Philippines’s sank 4.6%, the worst day for both markets since late 2011. Indonesia’s market lost 3.5%.

“It feels like the party is ending,” said Howard Wong, managing director at Doric Capital Corp. in Hong Kong.

Facing the loss of foreign capital, central banks in these emerging markets have attempted to prop up their home currencies.

India’s central bank dove into foreign-exchange markets Tuesday to stop the rupee’s slide; the currency hit a record low of 58.98 to the dollar before it recovered some ground, finishing at 58.34 late in New York, from 58.16 late Monday. Pressured to attract capital to the country, a top Indian economic official promised a new round of measures to allow foreign investment in restricted parts of the economy.

Turkey’s central bank on Tuesday announced new measures to attract capital after spending much of the past four years trying to stop too much money from flooding into its economy.

That helped to stem the lira’s fall to near a multiyear low against the dollar, and the currency finished higher on the day. Turkey’s capital measures echoed Brazil’s move earlier this month to eliminate a 6% tax on foreigners’ bond investments.

Meanwhile, Poland’s central bank said last week that it sold foreign currency to prop up the tumbling zloty.

But the capital exodus has continued apace, especially for economies heavily dependent on commodities, whose prices have been falling. Foreigners have been selling local mining stocks, and countries’ prospects for generating foreign exchange through commodity exports appear weaker than before.

The South African rand fell nearly 2% to 10.38 to the dollar, marking a 23% plunge from the beginning of the year, before reversing course and ending higher for the day, at 10.07 rand compared with 10.18 rand late Monday.

Australia, seen as a proxy for emerging markets in Asia because of its exposure to Chinese and Indian demand for its raw materials, also saw its currency plummet to its weakest point against the U.S. dollar since 2010. The Brazilian real fell early on Tuesday as foreign investors continued to pull up stakes from Latin America’s biggest economy but ended the day higher versus the dollar.

Brazil’s central bank stepped up intervention amid the rapid currency depreciation that began on May 28, with a series of five foreign-exchange swap auctions in two weeks. The auctions allow investors to exchange bonds linked to domestic interest rates for debt indexed directly to the U.S. dollar. The auctions tend to stall depreciation, but not for long.

Just two months ago, a wave of money was coursing around the globe as investors searched for yield. The stimulus measures the Bank of Japan announced on April 4 coincided with a rate cut from the European Central Bank and expectations that the Federal Reserve would continue its $85 billion in monthly bond purchases for the foreseeable future.

Several things have changed. Fed Chairman Ben Bernanke telegraphed last month that bond buying could slow later this year. The Bank of Japan’s injections of money into the economy have heightened turmoil in financial markets, with a spike in Japanese bond yields and a 20% selloff of Japanese stocks.

And there is mounting evidence that emerging-market economies just aren’t expanding as fast as people expected.

Chinese data in recent days showed exports rose only 1% in May from the year earlier, the slowest pace in 10 months, weighed down by poor demand from customers in Europe. Brazil and India are both suffering from slowdowns that have confounded policy makers and taken the shine off what had been among the most promising big economies in the world.

South Africa’s central bank warned last week that growth this year would likely fall short of its already tepid forecast for gross domestic product to expand 2.4%. Thailand’s central-bank governor said on Monday that the bank would soon lower its forecast for 5.1% growth this year.

Dimming growth expectations have also prompted a number of interest-rate cuts to prop up economies in South Korea, India and Thailand, Turkey and Israel.

India’s economy is among the hardest hit by the recent reversal in capital flows. The country’s slow growth—less than 5% annually in the past two quarters compared with nearly 10% a few years ago—and the weak rupee have made a fragile economy more vulnerable.

A weaker rupee makes it more expensive to pay for imports such as oil and coal. It also widens the government’s already large deficit, much of which goes to pay for fuel subsidies. More expensive imports also exacerbate inflation, limiting the central bank’s ability to cut interest rates to spur growth.

South Africa is battling the same forces. As growth slows, the South African central bank has been reluctant to cut interest rates because annual inflation is threatening to breach its target ceiling of 6%.

“That’s why it becomes even more imperative to deal with your domestic issues,” Reserve Bank Gov. Gill Marcus said last week. “We must take steps to address areas of short-term vulnerability.”

The outflows had been mostly orderly, and some currency weakening was welcomed because over the long term it can make a country’s exports more competitive globally. But the orderly pace changed Tuesday, when investors rushed for the exits.

“Until very recently the conversation was all about capital inflows causing asset-price bubbles,” said Gareth Leather, an economist with Capital Economics in London. “It’s switched very quickly.”