Fast Retailing, operator of the casual clothing chain Uniqlo, has become the unlikely symbol of volatility in Japanese stocks

June 12, 2013 Leave a comment

June 11, 2013, 2:23 p.m. ET

Fast Retailing: The Stock That Wags the Nikkei

By MAYUMI NEGISHI And BRADFORD FRISCHKORN

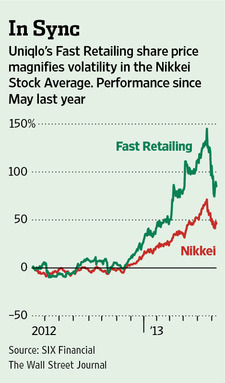

TOKYO—Fast Retailing Co., 9983.TO -1.44% operator of the casual clothing chain Uniqlo, has become the unlikely symbol of volatility in Japanese stocks, pulling with it the Nikkei Stock Average in its incandescent rise and sudden drop.

Shares in Fast Retailing, headed by Japan’s richest billionaire, Tadashi Yanai, more than doubled in 2013 to an all-time high of ¥44,400 before shedding 33% as Japanese equities markets underwent a severe correction stretching from late May to early June. Shares closed Tuesday at ¥31,250, down about 30%, and off 2.5% for the day, compared with a 1.45% loss for the overall Nikkei.

Neither the rise nor fall had much to do with the business performance of the maker of T-shirts and thermal underwear. The key was Fast Retailing’s 9.4% weighting on the Nikkei average—the highest of all 225 stocks in the index and more than the combined weighting of Japan’s four biggest companies by market capitalization.Prime Minister Shinzo Abe’s pledges to reflate a deflationary economy and boost government spending, coupled with a nearly 25% rise in the dollar’s strength against the yen, opened Japan’s markets to a flood of money. From November until May, institutional investors, hedge funds and retail investors flocked to find bargains in Tokyo’s long-ignored equities markets, and the sudden increase in trading volume made stocks rise and fall more rapidly..

Even amid one of the Nikkei’s most explosive rallies ever, the moves in Fast Retailing—one of Japan’s best performing companies—stand out.

“Our same-store sales go up 11%, and our share price drops. It doesn’t make sense,” a Fast Retailing executive said after the company released May sales data for Japan after the market closed June 4. The stock fell 9.5% the following day.

Fast Retailing has now become a favorite target of short-term trades. Some fund managers buy highly volatile shares such as Fast Retailing and Fanuc Corp.,6954.TO +1.09% while building up short positions—bets that the shares will decline—on the same stocks. Because prices are moving so fast, they can cash in on whichever position is making money, while holding onto the other until the market reverses.

Over the last 180 trading days, the price swings on Fast Retailing shares have been nearly twice as large on average as those inAeon Co., 6599.KU -1.07% Japan’s biggest retail group.Taking into account the recent slide, Fast Retailing stock is still up 43% from the beginning of 2013 and is trading at 36 times estimated earnings—more than double the valuation of Gap Inc., GPS -1.27% its closest rival.

“The valuations have stopped making sense,” said Makoto Kikuchi, head of Myojo Asset Management.

To the consternation of analysts and investors who try to value Fast Retailing based on its earnings prospects, the share price now is often at the mercy of Nikkei index futures. Trading volume doesn’t change much when news about the company comes out, but it spikes upward on days when listed options and Nikkei futures are settled.

“To someone looking at valuations, it’s frustrating, because the stock moves more on what [Prime Minister Shinzo] Abe or what [Bank of Japan Governor Haruhiko] Kuroda says, and how the Nikkei index futures move,” said Kazumasa Yamamoto, chief operating officer at investment fund Classy Capital Management Inc.

Given a weight of 2.7% when it joined the Nikkei average in 2005, Fast Retailing’s stock has outperformed its peers in the index ever since, increasing its weighting to 9.4% as of Tuesday. That puts its influence on par with the sway IBM Corp.IBM -0.51% holds over the Dow Jones Industrial Average. About one-third of Fast Retailing’s shares are owned by Mr. Yanai and family members.

Like the Dow, the Nikkei is a price-weighted index, meaning that its 225 components are weighted in proportion to their price per share. Because Fast Retailing’s share price has risen so much, the company’s weighting is far higher than all other stocks in the index.

That gives it huge influence over the index even though Fast Retailing’s market capitalization—a measure of value calculated by multiplying the share price by the number of shares outstanding—is less than one-sixth that of Toyota Motor Corp.7203.TO -2.85% Toyota, which earned more than 13 times Fast Retailing did last fiscal year, has a 1.8% weighting.

Most other well-known indexes, including the Standard & Poor’s 500-stock index and Japan’s Topix index, are based on market capitalization.

Because Fast Retailing tends to move in line with the Nikkei, investors often buy the stock as the market rises or falls, as a proxy for the overall average. Funds pour into the stock, often making swings in Fast Retailing shares more dramatic than moves in the Nikkei.

In addition to June 5’s nearly 10% fall, the stock tumbled 6.3% on June 3, far beyond the Nikkei’s 3.7% fall. At the same time, Fast Retailing has often vastly outperformed when the Nikkei is rising. It added 5.1% on May 31, compared with a 1.4% gain for the benchmark, and 7.4% on May 22, far better than the Nikkei’s 1.6% showing.

“The company attracted a lot of attention early as a growth story, but has taken on new dimensions as its weight has made it the target of arbitrage players who trade index futures and the cash market,” said CLSA equity strategist Nicholas Smith. “The result is a stock that trades completely divorced from its fundamental merits.”

There is little about Uniqlo’s business to justify its chronic volatility. The basic story behind Uniqlo has changed little for years: aggressive growth abroad and efforts to fight stagnation at home.

One of the darlings of deflationary Japan, Uniqlo has captivated investors with its ability to make good on its grandiose plans, catapulting from a small-town suit shop to become Asia’s biggest clothes retailer. As it works to become the world’s biggest apparel maker by 2020, it has launched mammoth flagship stores in New York and Shanghai to cement the appeal of its brand.

On June 4, Fast Retailing said its same-store sales in Japan rose 10.9% in May from the same period a year earlier, reversing a 3% decline in April.

Classy Capital’s Mr. Yamamoto said he missed a chance to bet against Fast Retailing’s stock at its peak, but he was hesitant to do so now, even if most analysts believe the stock is too expensive.

“It’s too scary,” he said. “You never know when people are going to start to bet that Nikkei futures will go up.”