In Japan, Aversion to Mergers Runs Deep

June 15, 2013 Leave a comment

June 14, 2013, 11:48 a.m. ET

In Japan, Aversion to Mergers Runs Deep

By ATSUKO FUKASE and MAYUMI NEGISHI

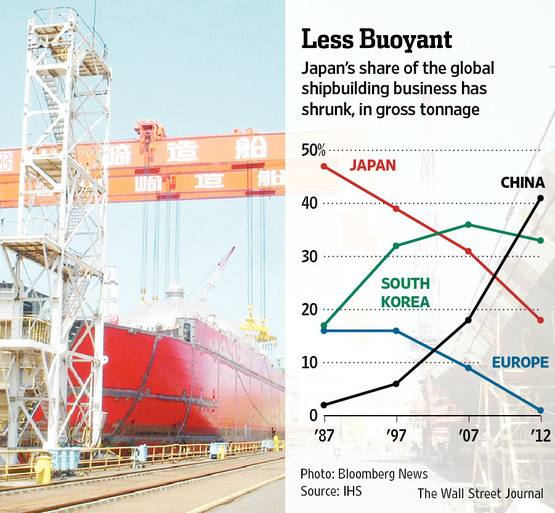

TOKYO—The Japanese government’s new “growth strategy” includes measures designed to encourage consolidation in manufacturing sectors notoriously overcrowded with inefficient companies averse to merging or combining overlapping production lines. A sign of the difficulties that lie ahead in promoting that reform came in the form of a 35-minute boardroom fight this week at Kawasaki Heavy Industries Ltd.,7012.TO +4.25% Japan’s second-largest heavy machinery maker. The battle ended with the ouster of the company’s president in order quash his plans to merge with rival Mitsui Engineering & Shipbuilding Co.7003.TO -5.52%Japan’s shipbuilding industry would seem a prime candidate for Prime Minister Shinzo Abe’s push for consolidation. Once the world’s unchallenged leaders commanding half the global market share for over four decades, the country’s 18 shipbuilders are now adjusting to a smaller pool of orders and a combined 18% market share in a world dominated by their South Korean and Chinese counterparts.

“There’s not much choice left for a shipping firm trying to survive in the domestic market,” a banker involved in the Kawasaki Heavy-Mitsui Engineering merger plan said, adding that further consolidation in the industry is inevitable in the near future.

But Kawasaki Heavy President Satoshi Hasegawa’s attempts to push a merger over internal opposition angered his board and convinced them of the necessity of a coup, executives said in a hastily called news conference on Thursday.

“We were extremely dissatisfied with the stance of the president, which proceeded from an assumption that the merger was a given, and we felt we could not trust him. We had no choice but to make this very bitter decision,” Kawasaki Heavy’s new president Shigeru Murayama said.

The deal’s demise is just the latest such example in an economy littered with carcasses of failed consolidation talks. In industries ranging from electronics to chemicals to construction, the domestic market is crowded with rivals, and companies spend so much energy to fight one another at home that they have fewer resources to win market share abroad.

Documents explaining Mr. Abe’s new strategy for reviving Japan’s moribund industrial sector argue that “too many companies in one industry” lead to “low profitability.” One chart cites examples like LCD TVs, where Japan has five makers, compared with two in South Korea, and one each in the U.S. and Europe. Japan has five main train makers, including Kawasaki Heavy, according to the documents, compared with one in South Korea.

“We will implement emergency structural reforms over the next five years to increase industrial competitiveness and promote investment in new ventures and more business consolidation,” Akira Amari, Mr. Abe’s economy minister, said at a news conference on May 29, promoting the new growth strategy.

Mr. Abe’s Industrial Competitiveness Council unveiled on Wednesday the final draft of the government’s economic growth strategy, which includes new tax breaks to encourage competing companies in saturated industries to combine.

But tax breaks are unlikely to have changed the course of past mergers that fell apart, due to difficulties combining corporate cultures, and an aversion to taking the steps that usually follow such combinations, like closing redundant operations and laying off workers.

Japan’s biggest industrial electronics conglomerate, Hitachi Ltd., 6501.TO +1.90%and the country’s biggest heavy machinery maker Mitsubishi Heavy Industries Ltd.7011.TO +0.75% in 2011 began talks to merge and create a match for General Electric Co. GE -0.68% But the two ended up joining just their thermal power businesses. In 2010, drink makers Kirin Holding Co. and Suntory Holdings Ltd., failed to complete plans to create a company whose annual revenue would rival brewerAnheuser-Busch InBev BUD +0.49% NV.

Kawasaki Heavy and Mitsui Engineering & Shipbuilding started discussing a merger a few months ago, according to the banker involved in the merger plan. The Nihon Keizai Shimbun daily reported the talks on April 22, but Kawasaki Heavy at the time denied the report. Kawasaki executives publicly confirmed the talks—as they were scuttling them—this week.

“It is extremely regrettable that Kawasaki Heavy should suddenly scrap all talks about merging,” Mitsui Engineering said in a statement on Friday.

Mr. Murayama, the new president at Kawasaki Heavy, whose products range from motorcycles to hydraulic pumps to New York City Transit subway cars and gas turbines, said his predecessor, Mr. Hasegawa, was only looking at the merger’s benefits for the company’s shipping operations and ignoring the higher costs it would have imposed on the rest of the company.

The ship-related operations account for about 10% of Kawasaki Heavy’s overall sales.

Like many other Japanese conglomerates, Kawasaki Heavy has sprawling operations, each of which often acts independently of the others. This makes infighting vicious, as even the president is seen partial to the operations in which he spent his career.

After the news of the scrapped talks, Kawasaki Heavy’s shares on Friday rose 4.2% and Mitsui Engineering’s shares dropped 5.5% while the benchmark TOPIX index rose 1.2%.

“Conglomerates are engaged in various business lines, and the issue of what to do with overlapping facilities makes it difficult for them to fully benefit from mergers,” said Takahiro Mori, an analyst at Bank of America BAC -1.06% Merrill Lynch. Mr. Mori added that the shipbuilding industry is one of the sectors in which it is difficult to cut jobs, and mergers yield only limited cost reductions.