China’s debt servicing cost and that Minsky moment; with shockingly high debt service ratio of 29.9% of GDP, no wonder that credit growth is accelerating without contributing much to real growth

June 5, 2013 Leave a comment

China’s debt servicing cost and dat Minsky moment

| Jun 04 12:48 | 32 comments | Share

Part of the CHINA’S CREDIT CONUNDRUM SERIES

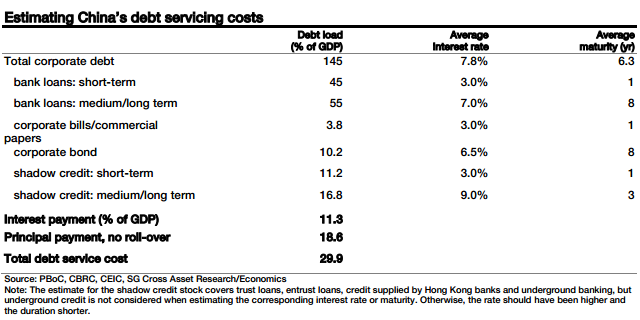

A little update on China’s growing debt-to-GDP ratio, which has caused much alarm and puzzlement this year. We’ve mentioned before a very interesting 2012 BIS paper on national debt servicing ratios, which found the following: …the DSRs’ peak levels are surprisingly similar across countries and time despite different levels of financial development. As a broad rule of thumb, the graph panels suggest that a DSR above 20–25% reliably signals the risk of a banking crisis. There are certainly exceptions to this — the authors of the BIS paper, Mathias Drehman and Mikael Juselius, point out that South Korea well exceeded this range before experiencing a financial crisis; while German and Greek crises occurred before 20 per cent was reached. What about China?Societe Generale’s Wei Yao has used the methodology from the BIS paper for calculating debt servicing ratios (DSRs) and applied it to China’s recent credit and growth data, including a broad measure of credit (ie, shadow banking). This is what she found (our emphasis):

First, taking bond, formal and shadow banking credit together, we see the debt burden of non-financial corporates and LGFVs at 145-150% of GDP as of end-2012. We consider LGFVs with other corporates because they are in pursuit of the same financing sources and increasingly face similar borrowing costs.

Second, the average interest rate and maturity are estimated at 7.8% and 6.3 years (see table below). Bear in mind that this is a fairly rough estimate, as detailed loan-level data are not easy to obtain, especially for shadow banking credit. As a general rule, we choose to adopt more lenient assumptions when information is scarcer. Therefore, maturities used in the calculation for each segment are probably longer than in reality and actual prevailing interest rates in the shadow banking system may be higher.

Third, assuming the repayment schedule of an instalment loan (i.e., a regular mortgage, for example), we then arrive at a shockingly high debt service ratio of 29.9% of GDP, of which 11.1% goes to interest payment (=7.8%×145 % of GDP) and the rest principal. At such a level, no wonder that credit growth is accelerating without contributing much to real growth!

Yao ponders whether this could be a ‘Minsky moment’, but she also points out the real debt servicing ratio is probably lower than her estimate, because the very low rates of non-performing loans recorded by Chinese banks indicates a lot of debt is being rolled over rather than repaid fully by the maturity date…

Apparently, debt roll-over is not a good thing either; and, it cannot explain the increase in the debt burden. Hence, the logical conclusion has to be that a non-negligible share of the corporate sector is not able to repay either principal or interest, which qualifies as Ponzi financing in a Minsky framework.

Finally, Yao looks at how this might all end.

This is the really challenging question for anyone with extremely bearish views on China — the country has after all bailed out its financial system before without throwing the country into chaos. We’ve looked at some of the possible ways today’s apparently-looming crisis might be resolved once again by the authorities. Yao, who’s not a particularly bearish analyst, is sceptical it will end well (her emphasis):

The mechanism that still holds the situation together is the state-backed formal banking system and its unspoken commitment to supporting local governments. We think this precarious equilibrium could last a bit longer but not much longer, particularly if the central government does nothing.

However she’s not forecasting chaos either — like other China pundits (Capital Economics for example) she’s been reassured that the central government hasn’t turned to big stimulus efforts this year and appears comfortable with slowing growth. She does believe though that rising defaults and non-performing loans are inevitable, and this will further stifle the growth rate.