When Heirs Become Major Shareholders in Asia’s Family Business Groups: Accounting Tunneling or Valuation Takeoff?

July 29, 2014 Leave a comment

“Bamboo Innovators bend, not break, even in the most terrifying storm that would snap the mighty resisting oak tree. It survives, therefore it conquers.” |

| BAMBOO LETTER UPDATE | July 28, 2014 |

Bamboo Innovator Insight (Issue 42)

|

|

Dear Friends and All,

Our presentation at the Value Unplugged event organized by John and Oliver in Naples and at the Value Investing Summit (VIS) by Ciccio in Trani went well based on the feedback of the participants. We are very honoured to be invited back to speak again at the event, including at a potential new event that is to be held and organized in Denmark by the country’s top value investor. It is really wonderful to be able to meet up with friends from around the world in person and to get to understand one another better. We look forward to sharing more insights with like-minded value investors who appreciate the value of having a knowledge-based process in the marathon of value investing and life. The Value Unplugged presentation material and video “To Catch an Asian Snake: Detecting Accounting Fraud Ahead of the Curve” will be made available for our Moat Report Asia Members.

Warm regards, The Moat Report Asia ——–

When Heirs Become Major Shareholders in Asia’s Family Business Groups: Accounting Tunneling or Valuation Takeoff?

“For investors who do not rely on professional advisers, stocks are usually more than just the abstract ‘bundles of returns’ of our economic modes. Behind each holding may be a story of family business, family quarrels, legacies received, divorce settlements, almost totally irrelevant to our theories of portfolio selection. That we abstract from all these stories in building our model is not because the stories are uninteresting but because they may be too interesting and thereby distract us from the pervasive market forces that should be our principal concern.” – Nobel laureate Merton Miller (1923-2000)

The silent but fierce battle to control one of Asia’s top family business groups with sales of over $80 billion and asset of $86 billion has intensified last week as two sons worked to become the handpicked successor of their patriarch father who turned 92 this October and who had underwent emergency surgery late last year after falling down.

Could this be a precursor to the succession and in-fighting risk that will take place in Asia’s family business groups which could override any advantages of the family model? Are there opportunities arising from capitalizing on the uncertainty surrounding the event?

The opening quote and investment insight by Merton Miller could ring true for regimes where the dominant corporate form are companies with dispersed, widely-held shareholding structure, but may be less relevant in Asia where entrepreneurial firms are typically tightly-controlled by a family. Many patriarchs in Asia built their fortunes with risky bets in the early post-war years, when Hong Kong was a desolate rock and Singapore was a swamp. They have shifted to become “rent-collectors” from property and related businesses (ports, hotels, retail) or from government concessions (electricity, telco, gas, casino licences). The simplicity of the underlying businesses may account for the ferocity of the family battles since it does not require sacrifice and knowhow for those who take over the business to continue to make money. Asian patriarchs and matriarchs add value in ways that do not appear on balance-sheets through their relationship-based deal-making capabilities. These strengths and tacit knowledge are difficult to bequeath or transfer to one’s children, and these specialized and intangible assets cannot be capitalized easily in the markets. This is why Asian empires systematically struggle to outlive their founders and succession tended to coincide with tremendous destruction of value.

Importantly, many of the crown-jewel assets in Asia are either not in the listed vehicles (these are in the private holdings of the tycoons) or that a tycoon has multiple vehicles through complicated shareholding structure for the family to exercise controlling rights with minimal capital. Thus the questions: Why is it that when heirs become major shareholders in Asia, the succession of controlling equity stake to next generation is often associated with tunneling of resources through related-party transactions to firms where the heir holds significant equity stake? What are the accounting properties around the leadership/ownership succession? We will examine these issues, which have important implications for value investors in Asia in the next decade, through the case of Korean and Hong Kong family business groups and two accounting research papers.

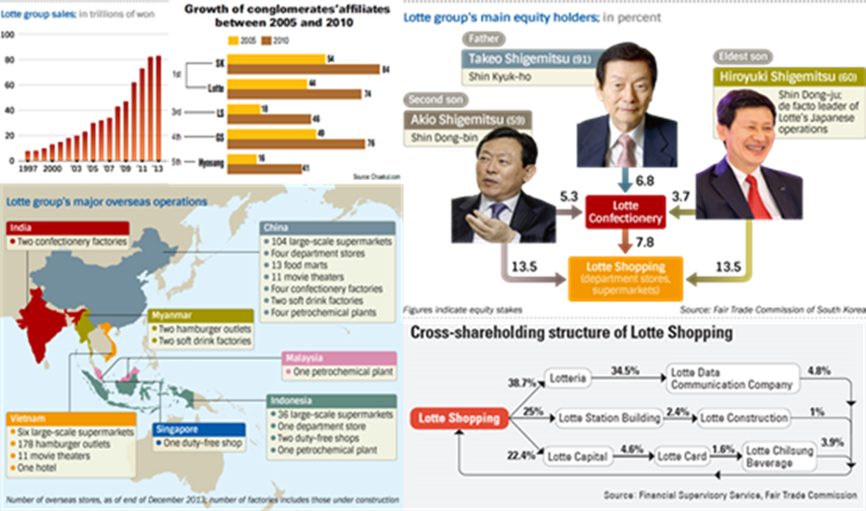

But first, back to the silent battle. Last week, more than 10 affiliates of Lotte Group exchanged part of their shares with one another to streamline the complex cross-shareholding structure ahead of the implementation of a law banning it. Early this month, the Fair Trade Commission (FTC) had rebuked Lotte Group for having cyclical shareholding structures within the group that form an intricate web for controlling its affiliates. Among the 74 affiliates, Lotte Confectionery (004990 KS, MV $2.8bn), Lotte Shopping (023530 KS, MV $9.4bn) and the unlisted Lotte Hotel, Asia’s third largest hotel chain, are the most important assets in terms of business and the governance structure. Lotte is one of the top conglomerates in Korea and Asia, thanks to its stable cash flow and unique portfolio composed of cash-rich industries. The two successors to the Lotte empire have been accumulating stakes in the key affiliate Lotte Confectionery since last year. Lotte Confectionery is up 31% this year and still trades at price-to-book of 1x. The power struggle and sibling rivalry was started decades ago when the patriarch Shin Kyuk-ho sent the elder son Shin Dong-ju to Japan and the younger Shin Dong-bin to stay in Korea. But the Korean operations have grown ten times bigger than the Jap ops in the past decades. The cooperative relationship between Japan’s and South Korea’s Lotte groups is cemented only by a marginal capital tie-up, so it could be terminated if the balance of power, underpinned by this capital alliance, tilts too far to one side.

Lotte Confectionery (Kospi: 004990 KS) – Stock Price Performance, 1983-2014

Inspired by the German author Goethe’s novel The Sorrow of Young Werther which Napoleon Bonaparte considered as one of the great works of European literature, Shin Kyuk-ho named Lotte Group after the character Charlotte in the book. Founded in 1948 as a chewing gum maker in Tokyo, Shin built Lotte with his marketing flair. Lotte later expanded to Korea with the establishment of Lotte Confectionery in Seoul in 1967, after Korea and Japan re-established diplomatic ties in 1965. Shin had gone to Japan in 1942 during the Japanese occupation period to study. Desperately wanting his career in literature, Shin overcame the disadvantage as ‘a Korean’ through his extraordinary diligence. He obtained investment from a Japanese who witnessed his diligence and built a factory that manufactured cutting oil in 1944. It was his first step as a businessman. However, he had to suffer hardships as his factory was completely destroyed by the bombs in the chaos of World War II. He was able to bounce back from the failure and now, Lotte grew to become Korea’s fifth largest chaebol in businesses ranging from snacks, beverages, department stores, to insurance, construction, amusement parks and hotels.

<Article snipped>

Is there an opportunity for value investors to accumulate Lotte Group’s key affiliates in the governance battle for control in the succession ahead?…… But first, we need to understand the accounting issues, specifically why the succession of controlling equity stake to next generation is often associated with tunneling of resources through related-party transactions to firms where the heir holds significant equity stake.

<Article snipped>

Lotte reminds us of the case of Vitasoy (345 HK, MV $1.3bn), in that most succession events are not smooth and that it takes an idea greater than oneself for different parties to work together harmoniously, especially during crisis periods.

Vitasoy was started by Dr. KS Lo with a little bean in 1940 at a factory located at Causeway Bay. KS (Kwee-seong) was the eldest son of Lo Chun-hing, a loyal employee of Eu Tong-sen, patriarch of Singapore’s Eu Yan Sang (SGX: EYSAN SP, MV $290m). In the late 1930s, KS returned to the Chinese mainland and HK to seek out opportunities and was surprised to see severe malnutrition in children caused by diseases in both places. Having got the idea that soybeans could be turned into a milk-like drink with high protein content after attending a talk entitled “Soya Bean: The Cow of China” presented by the American Julean Arnold, KS experimented in 1939 and successfully produced a cheap, nutritious, high-protein soya milk.

<Article snipped>

Both Shin and KS were inspired by the idea larger than oneself: to bring about kindness and betterment to children and people in ruined lands through food technology and quality products and services. This larger idea has galvanized the trust and support among the community of customers, business partners and suppliers throughout the years. Whenever this core value is diluted, without the accompanying culture of trust and decentralization to empower the people in the pursuit of growth, globalization, size and diversification, chinks in the mighty armour start to appear and can deteriorate quickly into major problems that would bring down the organization.

As value investors in Asia over the decade plus, we have often observed that the emperor-like and FFF (fight-for-favors) culture in companies is the #1 factor that has resulted in tremendous value destruction around the succession event and why the business does not scale further. There will be doubts about the ability, intention, motivation and fairness in rewards with people not trusting another to act in good faith; there will be envy, anger, and schadenfreude (joy at someone’s misery). How can a system be in place to eliminate doubt, envy, and schadenfreude?

<Article snipped>

Beyond the financial numbers, we like to look for this intangible idea larger than oneself to overcome and transcend beyond the vicious political fight for distributive tangible pools of money and power in Asia’s family business groups. Only then can we be more certain that accounting tunnelling is less likely to occur and valuation takeoff will take place.

To read the exclusive article in full to find out more about the accounting tunneling risks when heirs become major shareholders, as well as the inspiring stories of Korea’s Lotte Group/Shin and HK’s Vitasoy/KS, please visit:

|

| The Moat Report Asia |

|

“In business, I look for economic castles protected by unbreachable ‘moats’.” – Warren Buffett

The Moat Report Asia is a research service focused exclusively on competitively advantaged, attractively priced public companies in Asia.Together with our European partners BeyondProxy and The Manual of Ideas, the idea-oriented acclaimed monthly research publication for institutional and private investors, we scour Asia to produce The Moat Report Asia, a monthly in-depth presentation report highlighting an undervalued wide-moat business in Asia with an innovative and resilient business model to compound value in uncertain times. Our Members from North America, the Nordic, Europe, the Oceania and Asia include professional value investors with over $20 billion in asset under management in equities, secretive global hedge fund giants, and savvy private individual investors who are lifelong learners in the art of value investing.

Learn more about membership benefits here: http://www.moatreport.com/subscription/

https://www.moatreport.com/individual-subscription/?s2-ssl=yes

Our latest monthly issue for the month of July investigates an Asian-listed company who’s the global #1 and #2 maker of two types of patient monitoring devices for both clinical- and home-use. Founded in 1981 and listed in 2001, the company’s reliable manufacturing technology platform for over 30 years has enabled it to build a global durable franchise in the niche patient monitoring device market that has stable resilient growth and yet is experiencing potential disruptions led by its new innovation. A secret to its success is its in-house capabilities to combine Swiss design, high-precision electronics and sensors components with clinical healthcare to produce world-class products with cost competitiveness.The firm has competitive technology and patents especially its core competence of having an algorithm to allow fast reading/filtering of signals and outputting the accurate results in a short period of time. The company has the potential to consolidate the market further. The company is also a sticky ODM partner to reputable companies including Wal-Mart, Costco, CVS and it has a diversified customer base with none of the customers accounting for more than 10% of its sales. The company demonstrated that it has bargaining power over its powerful customers with the ability to build its own brand since 1998 (62% of overall sales). 91% of its sales are to developed markets in US and Europe. The company is trading at EV/EBIT 9.7x and EV/EBITDA 8.8x and has an attractive dividend yield at 5.6% and a strong balance sheet with net cash as percentage of market value and book equity at 23% and 47% respectively. The firm has also undertaken the unusual capital management program to reduce 10% of its shares outstanding in Sep 2012 to boost capital efficiency by utilizing the comfortable net cash position. The proactive shareholder-friendly stance backed by its strong net cash position should limit any downside in share price. The company’s terminal value and downside risk will be protected by giants such as J&J, Bayer, Abbott etc who wish to swallow it up to possess its valuable manufacturing technology platform and worldwide patents in algorithm-technology. The company’s worldwide patents in algorithm-technology has been commercialized into an innovative product series that is at the heart of its total solution service business model. This valuable intangible asset is not factored into long-term valuation. The innovative product with the algorithm measurement technology are not merely additional features; it “forces” the clinical community to adopt them as the standard, which in turn helps drive home-use penetration as patients seek a consistent and integrated healthcare experience. It transforms the product into a unique strategy that incorporates software development to create value-added services for health monitoring and collaborating with hospitals and governments on tele-healthcare projects. As a result of its wide-moat, the company has a far superior ROE at 20.9% that is nearly double that of its key giant conglomerate rival. When we compare EV/EBIT relative to ROE and ROA, the company is cheaper by as much as 120-150% when compared to its key giant conglomerate rival. The stock price of the company is down nearly 20% from its recent high in end March 2014 on profit-taking by short-term investors. Share price is back to May 2013 level, representing an attractive opportunity to take position in this long-term durable franchise. The stable long-term shareholdings and patient capital by the founder and the management team who together own around 48% of the equity has enabled the firm to adopt a very long-term approach to building its business and cultivating new growth areas. While he may sometimes be slightly over-optimistic and thinking too far ahead with his long-term opinions, this idealistic engineer-visionary-philosopher has done a fantastic job in continuously defying the odds of many skeptics by growing the company from a small startup into one of the world’s leading patient monitoring equipment company. He is the rare Asian entrepreneur who was persistent in building his own brand despite the threat of offending his ODM customers. He was also early in cultivating and coordinating a global network with high-tech component, R&D and manufacturing in his home country, manufacturing, assembly and packaging in Shenzhen, China and medical R&D and clinical testing center in Europe, including making the difficult decision to establish a direct marketing sales force in Europe and North America given the high cost. Unlike most Asian business owners whose interest and focus in the core business starts to wane due to complacency from growing personal wealth and the inability to scale the core business, the founder is genuinely passionate in the company’s ability to add value to the patients and society. The firm can effectively run without the founder with the long-term corporate culture and management system in place, yet he can inject great value as the steward in new innovations; we believe that this combination is rare for an Asian company and deserves a valuation premium.

Our past monthly issues examine:

The Moat Report Asia Members’ Forum has been getting penetrating quality dialogues from our subscribers. Questions range from:

Do find out more in how you can benefit from authentic and candid on-the-ground insights that sell-side analysts and brokers, with their inherent conflict-of-interests, inevitable focus on conventional stock coverage and different clientele priorities, are unwilling or unable to share. Think of this as pressing the Bloomberg “Help Help” button to navigate the Asian capital jungle. Institutional subscribers also get access to the Bamboo Innovator Index of 200+ companies and Watchlist of 500+ companies in Asia and the Database has eliminated companies with a higher probability of accounting frauds and misgovernance as well as the alluring value traps.

|

| Professional Development Workshops for Executives and Lifelong Learners |

|

Our 8th run of the series of workshop From the Fund Management Jungles: Value Investing Exposed and Explored – (Part 1) Moat Analysis, (Part 2) Tipping Point Analysis and (Part 3) Detecting Accounting Fraud – on 14 June 2014 has been well-received with serious value investors, professionals, and serious lifelong learners attending, with some who flew in from Jakarta and KL!..

Our 9th workshop will be on Detecting Accounting Fraud Ahead of the Curve sometime later in the year.

Thank you for your support all this while!

|

|

Thank you so much for reading as always.

Warm regards, KB Kee

Managing Editor The Moat Report Asia Singapore Mobile: +65 9695 1860

A Service of BeyondProxy LLC 1608 S. Ashland Avenue #27878 Chicago, Illinois 60608-2013 Other offices: London, Singapore, Zurich

|

|

P.S.1 Here is a little more about my background: KB Kee has been rooted in the principles of value investing for over a decade as an analyst in Asian capital markets. He was head of research and fund manager at a Singapore-based value investment firm. As a member of the investment committee, he helped the firm’s Asia-focused equity funds significantly outperform the benchmark index. He was previously the portfolio manager for Asia-Pacific equities at Korea’s largest mutual fund company.

He holds a Masters in Finance and degrees in Accountancy and Business Management, summa cum laude, from Singapore Management University (SMU) and had also published articles on governance and investing in the media, as well as published an empirical research paper Why ‘Democracy’ and ‘Drifter’ Firms Can Have Abnormal Returns: The Joint Importance of Corporate Governance and Abnormal Accruals in Separating Winners from Losers in the Special Issue of Istanbul Stock Exchange 25th Year Anniversary Best Paper Competition,Boğaziçi Journal, Review of Social, Economic and Administrative Studies, Vol. 25(1): 3-55. KB has also presented his thought leadership as a keynote speaker in global investing conferences. KB has trained CEOs, entrepreneurs, CFOs, management executives in business strategy, value investing, macroeconomic, industry trends, and detecting accounting frauds in Singapore, HK and China, and had taught accounting at the SMU where he is currently an adjunct lecturer.

P.S.2 Why do I care so much about doing The Moat Report Asia for you? My personal motivation in embarking on this lifelong journey has been driven by disappointment from observing up close and personal the hard-earned assets of many investors, including friends and their families, burnt badly by the popular mantra: “Ride the Asian Growth Story!” Iwitnessed firsthand the emotional upheavals that they go through when they invest their hard-earned money – and their family’s – in these “Ride The Asian Growth Story” stocks either by themselves or through money managers, and these stocks turned out to be the subject of some exciting “theme” but which are inherently sick and prey to economic vicissitudes. They may seem to grow faster initially but the sustainable harvest of their returns is far too uncertain to be the focus of a wise program in investment. Worse still, the companies turned out to be involved in accounting frauds. Their financial numbers were “propped up” artificially to lure in funds from investors and the studiously-assessed asset value has already been “tunnelled out” or expropriated. And western-based fraud detection tools and techniques have not been adapted to the Asian context to avoid these traps.

After a decade-plus journey in the Asian capital jungles, it has been somewhat disheartening as I observe many fraud perpetrators go away scot-free and live a life of super luxury on minority investors’ hard-earned money. And these perpetrators make tempting offers to various parties in the financial community to go along with their schemes. When investors have knowledge in their hands, we have a choice to stay away from these people and away from temptations and do the things that we think are right. With knowledge, we have a choice to invest in the hardworking Asian entrepreneurs and capital allocators who are serious in building a wide-moat business.

|

CONNECT WITH US      |

| MOAT REPORT ASIA OUR TEAM SUBSCRIBE MEMBERS CONTACT US

The Moat Report Asia Other offices: London, Singapore, Zurich |